Gold for high-net-worth investors

Editorial guide to gold allocations for high-net-worth investors: institutional depository options, allocated-segregated storage, and trust-and-estate considerations.

If you are managing a 7-or-8-figure portfolio

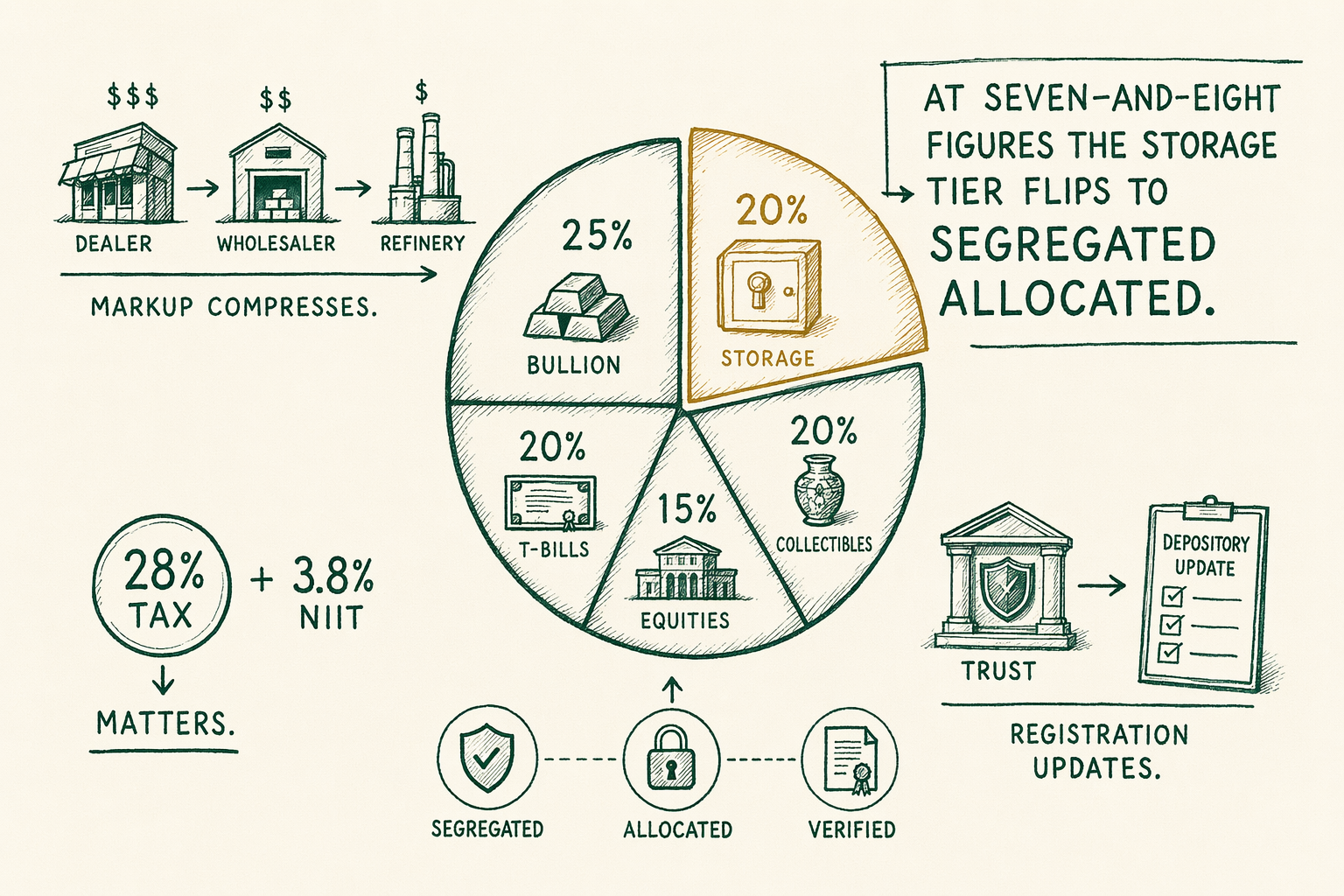

If you are managing a portfolio in the `$1M`-`$50M+` range and considering gold as a portfolio-insurance sleeve or a generational store of value, the editorial mechanics that apply to a `$50,000` retail Gold IRA do not scale linearly. At seven and eight figures the storage tier shifts (segregated allocated becomes a default rather than a premium), the dealer channel widens (direct refinery and wholesaler relationships open up below the retail dealer markup), the trust and estate planning becomes load-bearing, and the tax mechanics — particularly around the IRS `28%` collectibles rate on long-term gains — start to matter materially.

This guide walks the five issues most often raised in reader questions from this audience: storage tier choice at scale, the institutional-vs-retail depository decision, direct refinery purchase logistics, trust-and-estate structuring, and the tax treatment that becomes material once realized gains cross meaningful dollar amounts. The desk does not deliver personalized recommendations; the material below points at the questions worth bringing to a wealth manager, an estate-planning attorney, and a CPA experienced with high-net-worth precious-metals planning.

What this guide covers

Five sections. First, the storage-at-scale question: why segregated allocated typically becomes the default at meaningful weight, and how the per-ounce storage economics shift in favor of segregation as the position grows. Second, the institutional-versus-retail depository decision: HSBC and JPMorgan operate institutional-tier vaulting that opens up at certain account sizes, alongside the retail-channel depositories (Delaware, Brink's, IDS). Each has tradeoffs.

Third, direct refinery and wholesaler purchase considerations: at multi-kilo and `400 oz` London Good Delivery quantities, the dealer markup collapses but minimums, KYC, and settlement mechanics tighten. Fourth, trust and estate planning specific to precious-metals holdings: revocable living trusts, irrevocable trusts for specific asset-protection or estate-tax reasons, family limited partnerships, and the documentation that makes the inheritance transition clean. Fifth, tax treatment at scale: the IRS `28%` long-term capital gains rate on collectibles (which includes most physical gold), state-level treatment, and the strategic decisions around realization timing.

Each section ends with the relevant licensed-professional pointer. The desk publishes editorial framing; the personalized answer comes from the wealth manager, the estate-planning attorney, the CPA, and (for the largest estates) the family-office team you assemble.

Storage at scale — allocated segregated as default

At retail Gold IRA scale (`$25,000`-`$250,000`), the storage choice is typically commingled allocated (your specific bars tracked by serial number but stored physically together with other clients' same-format bars) because the segregation premium is a meaningful percentage of the account. Segregated allocated runs `$100`-`$300/yr` at IRS-approved depositories; commingled allocated runs `$75`-`$150/yr`. On a `$50,000` account the segregation premium is `$25`-`$200/yr`, a non-trivial percentage of the asset.

At high-net-worth scale (`$1M`+), the economics flip. Segregated allocated storage at a major depository typically scales with metal weight or asset value, with effective rates that compress as the position grows. A `$2M` precious-metals position in segregated allocated storage at Delaware Depository or Brink's might run `$1,800`-`$3,500/yr`, depending on the specific arrangement — roughly the same `$/oz` rate as the retail-account commingled tier. The marginal cost of segregation is small at scale, and the benefits (serial-number-level identification of specific bars, clear chain-of-custody documentation for trust or estate purposes, the right to physically inspect specific items rather than equivalent-weight items) compound.

Segregated allocated at scale is the editorial default for the audience this guide addresses. The exceptions are large institutional holdings where the unit of trade is the `400 oz` London Good Delivery bar, in which case segregation is less load-bearing because each bar is independently serialized and traceable, and the operational efficiency of commingled storage compounds favorably across the institutional portfolio.

Institutional vs retail depository options

Delaware Depository, Brink's Global Services, and IDS of Texas / Delaware are the retail-channel depositories that dominate the Gold IRA marketing channel. They are also fully appropriate for high-net-worth holdings outside the IRA wrapper, with institutional-tier insurance and audit arrangements. The desk's review of these depositories at `/reviews/storage-vaults/` covers the structural differences; for high-net-worth holdings the same comparison applies, with the additional question of whether to consolidate at a single depository (operational simplicity) or split across two (counterparty diversification).

HSBC and JPMorgan operate institutional-tier vaulting that opens up at certain account sizes (the specific thresholds vary by bank and by the client relationship — both banks gate access through their private banking and wealth-management channels). The institutional-tier services include LBMA Good Delivery bar custody, multi-jurisdiction storage (London, Zurich, Singapore, New York), and deeper bullion-banking services (lending, hedging) that are not available through the retail-channel depositories. For the largest precious-metals positions these services are differentiated.

The desk's editorial position is that for most high-net-worth investors holding gold as a portfolio-insurance sleeve rather than as part of an active trading book, the retail-channel depositories (Delaware, Brink's, IDS) at segregated allocated are entirely appropriate. Institutional-tier vaulting via HSBC or JPMorgan is relevant when the bullion holding is part of a broader private-banking relationship, when multi-jurisdiction storage is a strategic consideration, or when the position exceeds roughly `1,000 oz` (`~$2.5M-$3M` at current prices).

Direct refinery purchase considerations

At multi-kilo quantities and above, the dealer markup compresses materially. A `1 kg` (`32.15 oz`) LBMA-listed bar typically runs `1%`-`2.5%` over spot at retail dealers; at direct-refinery purchase through a relationship account, the same bar can land at `0.5%`-`1%` over spot, with the savings approximately doubling to a fraction of a percent at the `400 oz` London Good Delivery bar level. For a `$5M` precious-metals purchase, a `1.5%` margin compression saves `$75,000` — large enough to justify the KYC and operational overhead of opening a direct-refinery or wholesaler relationship.

The practical gate is the minimum order size and the KYC requirements. Direct refinery purchase typically requires a documented business or trust relationship, KYC documentation that exceeds retail-dealer standards, and order minimums in the multi-kilo range (some refiners gate at `5 kg`; institutional accounts start at the `400 oz` London Good Delivery single-bar minimum, currently `~$1M`+ at spot). Settlement is via wire to the refiner's nominated bank; the metal is typically held in the refiner's affiliated vault until the buyer instructs onward delivery to the buyer's depository.

The wholesaler channel is the middle path. Wholesalers (some of the same entities operate retail dealer and wholesaler arms) accept business or trust accounts with substantial minimum activity (`$250,000`+ initial position is common), apply institutional KYC, and offer pricing between the direct-refinery tier and the retail dealer tier. For most high-net-worth buyers a wholesale-tier relationship is the practical choice. Sourcing the relationship is typically through a private bank, a family-office service provider, or a precious-metals-specialist advisor.

Trust and estate planning

Precious-metals holdings of meaningful size require explicit estate-planning treatment. The default — bullion held personally, registered to the individual, in a personal allocated-storage arrangement — works at any scale but loses optionality. The estate-planning structures common at high-net-worth scale include revocable living trusts (the typical default, providing probate avoidance and continuity of management at incapacity), irrevocable trusts (for specific asset-protection or estate-tax reasons), and family limited partnerships (for multi-generational holdings with consolidated management).

Holding bullion inside a revocable living trust requires updating the depository's registration to reflect the trust as the legal owner, with the individual (as trustee) maintaining management control. The mechanics are straightforward and most retail-channel depositories handle the documentation routinely. Irrevocable structures (asset-protection trusts, generation-skipping trusts, charitable remainder trusts) carry more complex documentation requirements; the depository's documentation team typically requires the relevant trust agreement, the trustee's letter of authority, and standard KYC on the trustee. Allow `2`-`4` weeks for the registration update.

The state-jurisdiction question matters at scale. Some states (notably South Dakota, Nevada, Delaware, Alaska) offer trust law that is materially more favorable for long-duration trusts; the choice of trust situs is an estate-planning-attorney decision rather than a precious-metals-storage decision. The depository's location is a separate question from the trust's situs; both can be optimized.

Tax treatment at large scale

Physical gold is classified as a 'collectible' under IRC Section `408(m)`, and long-term capital gains on collectibles are taxed at a maximum `28%` rate at the federal level — higher than the `20%` maximum that applies to most other long-term gains. The difference is meaningful at scale. A `$5M` precious-metals holding realized after a long-term hold with a `$2M` basis would face roughly `$840,000` in federal capital-gains tax at the `28%` collectibles rate, versus `$600,000` at the `20%` standard long-term rate. State-level treatment varies; some states tax capital gains as ordinary income.

Net investment income tax (NIIT) adds another `3.8%` to investment income (including capital gains) for high-income filers above the relevant threshold (`$200,000` single, `$250,000` joint, modified AGI). On the same `$5M` example with `$2M` basis, NIIT adds roughly `$114,000` to the federal bill. Total federal liability on a long-term sale of physical gold can reach `31.8%` before state tax. Plan the realization timing with a CPA who handles both the collectibles rate and the NIIT mechanics.

Gold IRA holdings sidestep the collectibles rate question because they are distributed at ordinary-income rates rather than capital-gains rates. The tradeoff is the ordinary-income rate (potentially as high as `37%` at the top federal bracket, plus state) versus the `28%` collectibles rate plus NIIT. For high-bracket filers the after-tax math can favor after-tax holdings; for moderate-bracket retirees the IRA-distribution path may be more efficient. This is exactly the type of decision where a CPA's personalized analysis pays for itself.

Recommended next steps

Three pointers. For the depository-side comparison see `/reviews/storage-vaults/` (Delaware, Brink's, IDS, HSBC, JPMorgan all covered). For the allocated-vs-unallocated and segregated-vs-commingled distinctions see `/guides/allocated-vs-unallocated/`. For the buying-physical-gold mechanics (which apply at any scale, with the dealer channel widening as the position grows) see `/guides/buying-physical-gold/`.

For the wealth-management-and-tax side, the team at this scale typically includes a private-banking relationship for cash management, a wealth manager for portfolio construction, an estate-planning attorney for trust structuring, a CPA experienced with collectibles taxation and NIIT, and (for the largest estates) a family-office service provider for consolidated reporting. The desk's role is to point at the questions worth asking; the licensed professionals deliver the personalized answer.

For the editorial standards and disclosure policies, see `/editorial-standards/`. Reviews carry quarterly snapshot dates; confirm current arrangements before committing at any scale.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Do high-net-worth investors hold gold differently?

Often yes — larger positions justify segregated allocated storage at institutional depositories, more granular contract terms, and direct refinery relationships. The economics of segregated storage become more favorable at higher metal weights. -

Is direct refinery purchase practical?

For large positions (multi-kilo or 400-oz London bars), direct refinery or wholesaler purchase can compress spreads versus retail dealers. Practical minimums and KYC requirements apply. -

Where do I go next?

Start with the linked topic hub for a deeper foundation, then the comparison page that matches your selection criteria. Every claim about a company carries a snapshot date — confirm current arrangements before committing. -

Is this personalized advice?

No. BullionLens publishes editorial coverage, not personalized investment advice. Use this material to understand the landscape, then consult a licensed adviser for your specific situation.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.