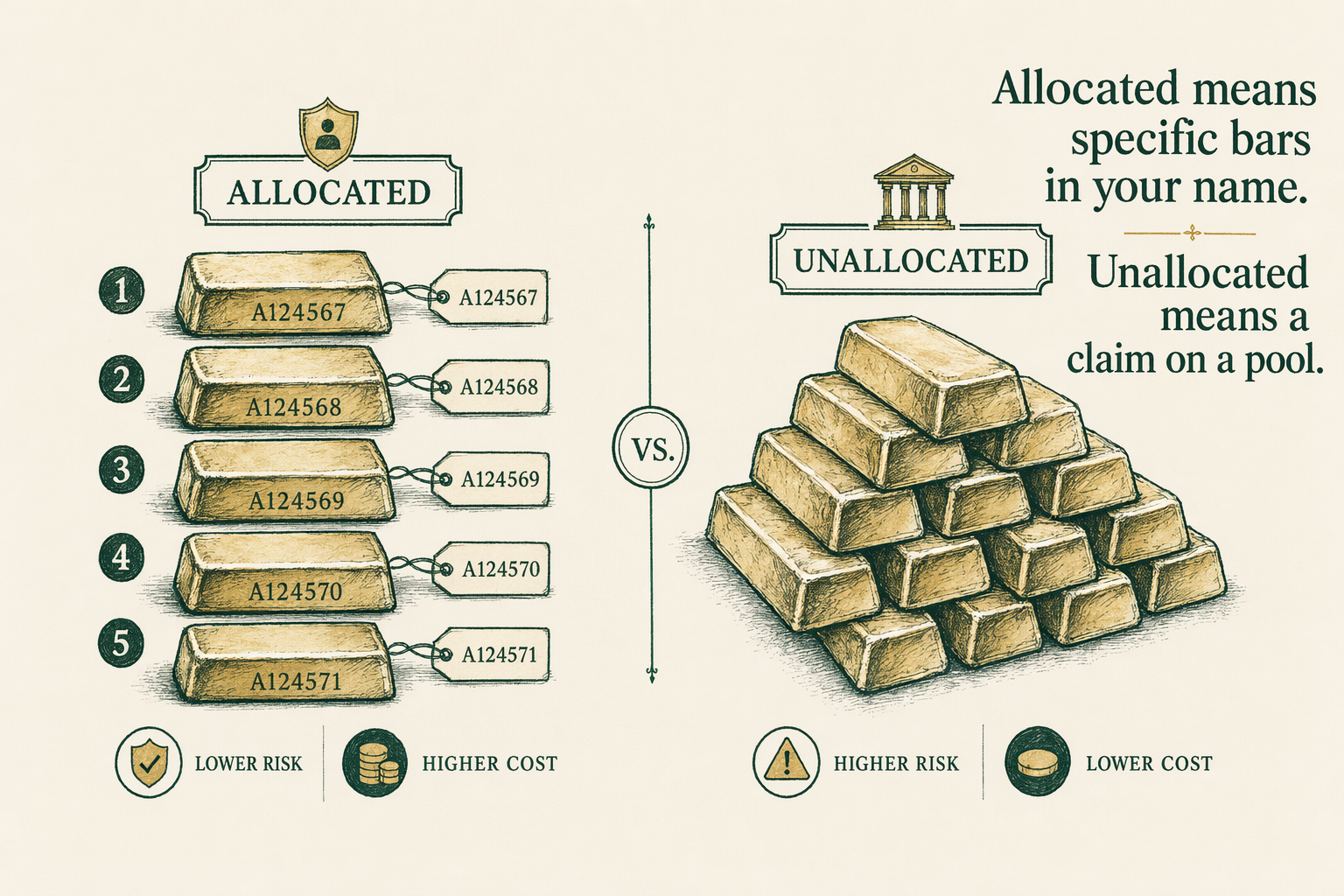

Allocated vs unallocated storage

Allocated storage means specific bars in your name. Unallocated means a claim on a pool. The cost and counterparty implications, explained.

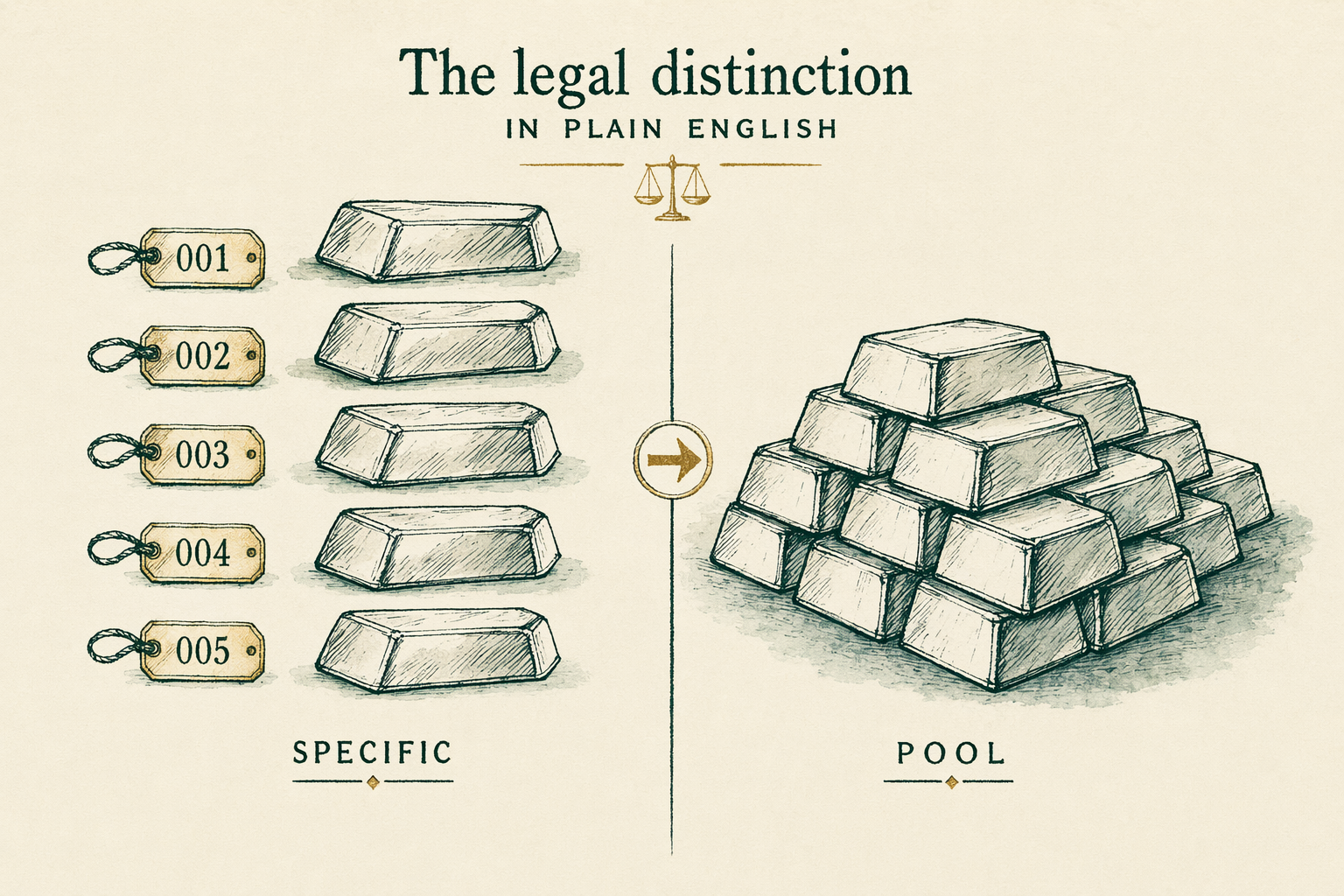

The legal distinction in plain English

An allocated storage arrangement is, in common-law jurisdictions, structured as a bailment. The vault operator (the bailee) holds your specific metal (the bailed property) in safekeeping for you (the bailor). The metal is your property, with the vault providing custody services. The vault's records identify the specific bars or coins associated with your account: refiner, serial number, weight, fineness, account number. In a properly drafted allocated agreement, the vault has no right to lease, lend, pledge, or otherwise dispose of your metal.

An unallocated arrangement is, in common-law jurisdictions, structured as a debtor-creditor relationship. The vault operator owns the pooled metal on its balance sheet. You own a claim — an obligation of the vault operator to deliver a stated weight of gold of stated fineness on your demand (subject to the agreement's terms). The vault operator can lease, lend, or use the pooled metal for its own account, subject to maintaining sufficient pool inventory to cover client claims. Your relationship to the metal is an unsecured creditor relationship to the operator.

The vocabulary varies by jurisdiction and by the specific contractual language, but the underlying property-law distinction is consistent across jurisdictions where bullion vaulting is a meaningful industry. In civil-law jurisdictions the same distinction appears under different legal terminology but with similar economic effect.

The single most important practical implication: in the operator's bankruptcy, allocated metal (if the documentation is clean and the allocation was real) is your property and should not enter the bankruptcy estate. Unallocated metal is part of the operator's assets, and your claim is one of many against the same pool.

Allocated — specific bars registered to you

In a fully allocated arrangement, the depository's holdings records show your account number associated with specific bars: refiner mark, bar serial number, weight (to the gram or finer), fineness (purity to .999 or .9999 fine), and date of receipt into the depository.

Allocated storage further subdivides into two sub-types in modern depository practice. Segregated allocated means your specific bars sit in their own physical compartment, drawer, or vault — physically separated from other clients' bars. Commingled allocated means your specific bars are tracked by serial number in the depository's records but stored in shared institutional vaulting alongside other clients' bars. Both satisfy IRS Section 408(m) requirements for Gold IRA storage. Both are 'allocated' under the property-law definition. Segregated allocated costs more — the depository is providing physical-space-level custody on your behalf.

Documentation you should receive in an allocated arrangement: a holdings statement listing the specific bars in your account by serial number and weight, dated at least quarterly and ideally monthly; an annual audit confirmation from the depository's independent auditor confirming the holdings reconciliation; the storage agreement language explicitly stating that the metal is held as bailment property and that the operator has no right to lease, lend, or pledge.

Modern depositories publish allocated-holdings statements monthly to many clients. Delaware Depository, Brink's Global Services, and International Depository Services all maintain procedures for client-requested holdings statements; institutional clients receive these on regular schedules. Retail clients can typically request a statement on demand at no charge or for a nominal handling fee.

If you ever cannot get a serial-number-level holdings statement from an arrangement that is marketed to you as 'allocated,' that arrangement is not allocated in the strict property-law sense regardless of marketing terminology. Verify in writing before signing.

Unallocated — a claim against a pool

Unallocated storage is structured as a pool-claim arrangement. The vault operator pools metal from many clients (and often the operator's own inventory) into shared institutional vaulting. Your account record shows a weight balance, not specific bars. The operator owes you the agreed weight of gold on demand, subject to the agreement's notice periods and delivery terms.

Unallocated arrangements are common in two specific institutional contexts: London Good Delivery (LGD) bullion banking, where the LBMA market-making banks maintain unallocated accounts with each other and with their institutional clients as part of OTC market plumbing; and certain ETF and pooled investment products that hold metal in unallocated form on the back end while issuing share-level claims to retail investors.

The retail-investor unallocated proposition is typically marketed as cheaper, simpler, and more liquid — and on healthy-market days it is all three. The arrangement does carry meaningful counterparty risk that is often understated in retail marketing. The operator's solvency, the quality of the operator's audit and inventory-management procedures, and the strength of the operator's segregation between client-pool metal and operator-proprietary metal are all material to your risk exposure.

Some unallocated arrangements include a contractual right to 'allocate' specific bars on demand — sometimes for a fee, sometimes free of charge — which converts the pool claim into specific-bar registration. If you are signing an unallocated arrangement, check whether this conversion right exists and what the fee and process look like.

IRS-approved Gold IRA storage does not use unallocated arrangements. The IRS's Section 408(m) approved-depository framework requires the depository to hold IRA metal in identifiable form — practical implication: only allocated arrangements (segregated or commingled) qualify.

Cost differences

Allocated arrangements typically cost 50% to 150% more than unallocated for the same metal weight at the same depository, because the depository is providing item-level custody and reporting rather than pooled bookkeeping.

Indicative 2026-Q2 pricing at major IRS-approved depositories: • Segregated allocated, retail client: `$150` to `$300/yr` per account, with tiered escalation by metal weight above a base threshold. • Commingled allocated, retail client: `$75` to `$150/yr` per account, generally flat-rate or with a lighter weight-tier. • Unallocated (where retail-available): `$0` to `$60/yr` per account, sometimes embedded into spread or ETF expense ratio rather than itemized as a storage fee.

ETF holders pay the equivalent of unallocated storage cost embedded in the expense ratio rather than as a line-item storage fee. The two largest physical-gold-backed ETFs in the US market — GLD and IAU — charge expense ratios that incorporate storage and operating costs in single-digit basis points to roughly 40 basis points annually, with the metal held in allocated form on the ETF's behalf at HSBC's London vault. The retail share holder owns ETF shares, which are themselves a pool claim against the trust's metal — a different layer of pooling than direct retail unallocated.

The cost premium for allocated is the price of property-law certainty under operator stress. In normal markets the cost premium feels like overhead; in stress events it can be the difference between recovering your metal and standing in a creditor line. Whether that premium is worth paying depends on the size of the position and the buyer's view of operator-stress probability.

Counterparty risk implications

In a healthy market, both allocated and unallocated arrangements deliver what they promise. The distinction matters at the tail — under operator stress.

Allocated under operator bankruptcy: your bars are your property. The vault is a bailee, not the owner. Properly executed allocated metal does not enter the operator's bankruptcy estate and should be available for client claim against the bankruptcy trustee. The /case-studies/allocated-storage-after-mf-global/ case study walks the MF Global bankruptcy in detail, where most allocated bullion clients ultimately recovered full claims through the SIPA liquidation process — though recovery was not immediate and stressed clients' liquidity in the interim.

Unallocated under operator bankruptcy: you are a general unsecured creditor of the operator for the metal weight owed. Your claim ranks with all other unsecured creditors. Recovery depends on the bankruptcy estate's assets after secured creditors and senior claims are satisfied. Historical recoveries on bullion-related unallocated claims have ranged broadly; the specific factual record of each insolvency determines outcomes.

Even in allocated, real-world documentation can have gaps. The MF Global case demonstrated that 'allocated on paper' did not always mean 'allocated in practice' when third-party broker arrangements intervened. The post-MF-Global industry response has been greater emphasis on third-party audits, more granular client-documentation requirements, and increased client demand for direct depository custody rather than broker-intermediated allocated arrangements.

Practical risk-mitigation for an allocated client: (a) request the storage agreement before signing, read the bailment language, confirm the operator has no lease/lend/pledge right; (b) request monthly holdings statements and verify they reconcile bar-by-bar; (c) confirm the depository's audit framework — Lloyd's of London underwriting requires an independent audit cadence at major depositories; (d) confirm the depository's solvency standing through publicly available financial information and rating-agency data where available; (e) consider whether the documentation chain runs through any intermediary (broker, IRA marketing company) and what that intermediary's solvency exposure adds to the chain.

When unallocated makes sense (and when it does not)

Unallocated can be a reasonable arrangement for a meaningful subset of bullion holders. The cost savings (50% to 150% per year) compound over time. Liquidity is often better in unallocated — large weights can typically be drawn down or transferred more quickly than allocated holdings, which sometimes require physical-shipment lead time. Some sophisticated institutional uses of bullion specifically require unallocated form for accounting or hedging purposes.

Unallocated arrangements at LGD (London Good Delivery) bullion banks are the institutional plumbing of the global gold market. ETF backings (with allocated metal at the trust level but pool claims at the share level) provide low-friction retail access to gold-price exposure at very low expense ratios. These are reasonable structures with well-understood mechanics for the buyers who use them.

Unallocated does not make sense where the buyer needs property-law certainty against operator stress — typically large positions, retirement assets, family-trust assets, or any holding the buyer would not want exposed to general-unsecured-creditor risk against the vault operator. For these uses, allocated is the appropriate structure, and the annual cost premium is the price of that certainty.

Unallocated is also generally inappropriate inside a Gold IRA wrapper — both because the IRS approved-depository framework requires identifiable holdings, and because the additional layer of intermediation (IRA custodian, between you and the depository) makes property-law certainty harder to maintain.

The decision is a tradeoff with no universally correct answer. Position size, time horizon, the buyer's view of operator-stress probability, and the structural use case (long-term hold vs trading vehicle vs institutional plumbing) all matter. The /reviews/storage-vaults/ hub covers the major IRS-approved depositories and their allocated-storage practices in detail.

How we sourced this

Citations draw from LBMA-published guidance on allocated vs unallocated bullion accounting; the Bank for International Settlements documentation on bullion-bank balance-sheet treatment of unallocated client liabilities; SEC filings and bankruptcy court records from the MF Global SIPA liquidation (case 11-2790 in the US Bankruptcy Court for the Southern District of New York); and the published storage-fee schedules and storage-agreement language of major IRS-approved depositories including Delaware Depository, Brink's Global Services USA, and International Depository Services (Texas and Delaware).

Property-law characterization draws from standard common-law bailment doctrine as discussed in Goode and McKendrick's Commercial Law and analogous treatises. Specific applications to bullion storage and the MF Global case have been examined in commentaries from the LBMA's working group on customer-asset protection (2012-2015).

In plain English

In plain English: allocated means specific bars with your name on them sit in the vault. Unallocated means the vault owes you a weight of gold from a shared pool. Allocated costs about double. Allocated metal is yours if the vault goes bankrupt; unallocated metal puts you in line with other creditors. ETFs use a hybrid (allocated at the trust level, pooled at the share level) and are reasonable for low-cost market exposure. For Gold IRAs the IRS requires allocated. For after-tax holdings at meaningful size, allocated is the conservative choice — ask for monthly serial-number-level statements and verify the agreement explicitly bans lease/lend/pledge.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is allocated storage?

Specific bars or coins, identified by serial number and weight, are registered in your name in the vault operator's records. You have legal title to specific physical metal. -

What is unallocated storage?

You have a claim against a pool of metal held by the vault operator. The operator owes you the agreed weight of metal; you do not own specific bars. Cheaper than allocated. -

Why does the distinction matter in a bankruptcy?

In an allocated arrangement, your bars are not the operator's property and (subject to clean documentation) should not enter the bankruptcy estate. In an unallocated arrangement, you are a general creditor of the operator for the metal balance. -

Which do Gold IRAs use?

IRS-approved depositories for Gold IRAs offer allocated storage, typically segregated or commingled-allocated. Unallocated storage is generally not used inside a Gold IRA wrapper.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.