Gold taxation in the US — the editorial primer

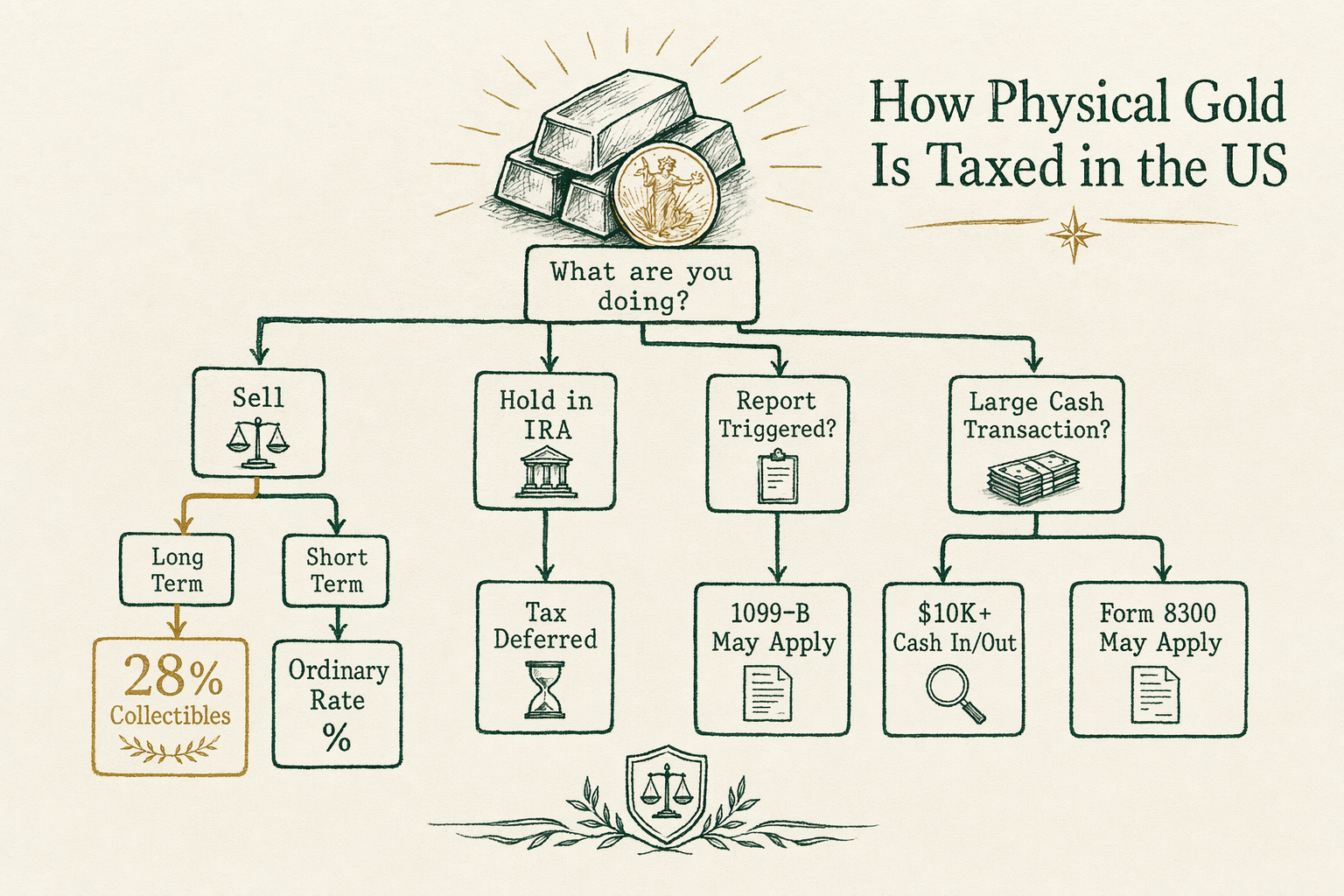

How physical gold is taxed in the US: 28% collectibles rate on long-term gains, IRA tax-deferred treatment, 1099-B reporting triggers, and Form 8300 thresholds.

Physical gold as 'collectibles' under IRS code

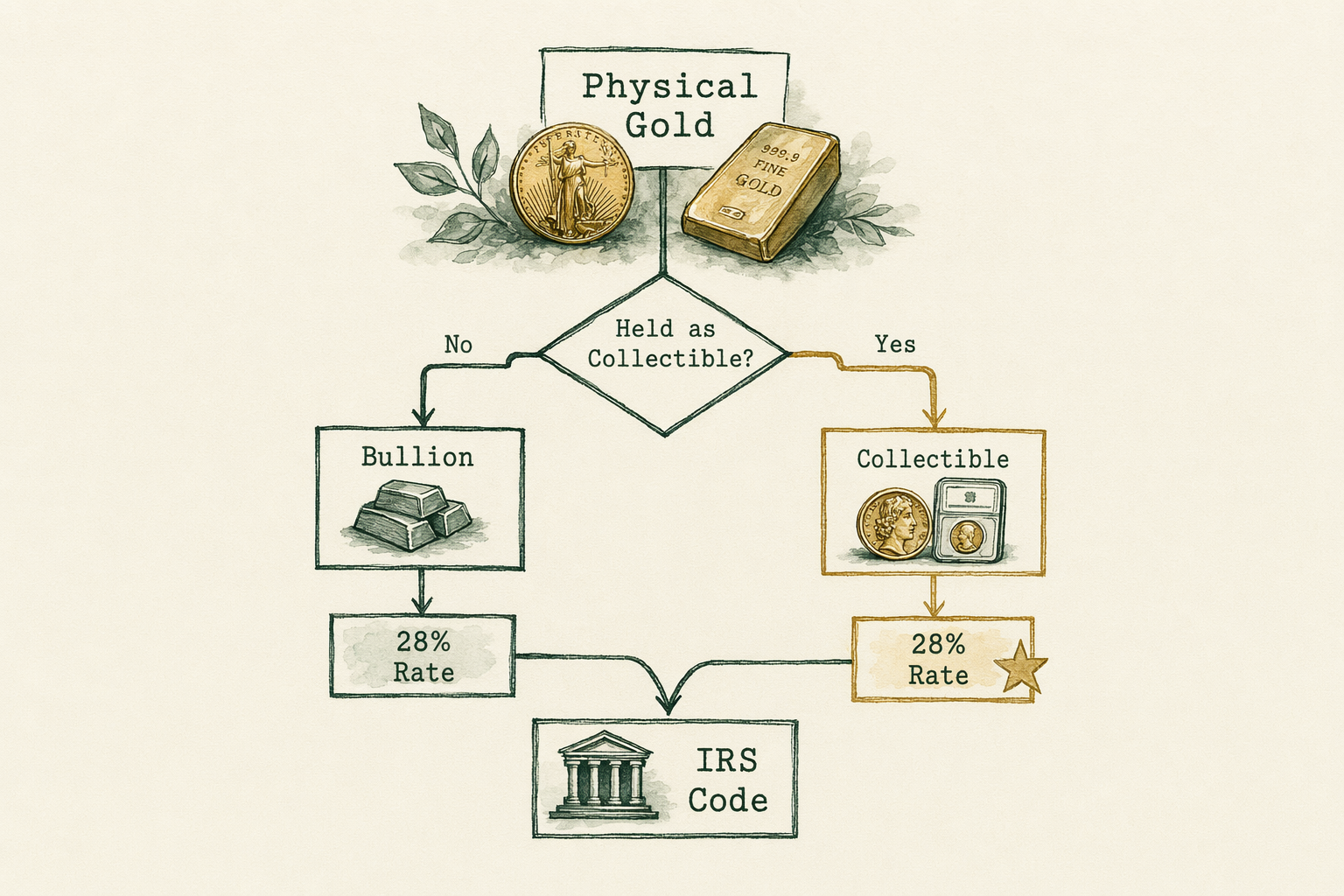

The Internal Revenue Code categorizes physical gold and most bullion coins as 'collectibles' under IRC Section 408(m). The statutory definition of collectibles for this purpose includes 'any metal or gem' subject to limited exceptions specified in the same section.

The collectibles classification has two distinct downstream consequences. First, it determines the long-term capital-gains tax rate on after-tax holdings (next section). Second, it determines what bullion is and is not eligible to be held inside an IRA wrapper. Section 408(m) prohibits IRAs from holding collectibles — and then carves out specific exceptions for certain coins meeting fineness requirements and bars from approved refiners. The carve-out is what makes Gold IRAs legally possible at all.

The carve-out for IRA-eligible bullion: any coin meeting specified fineness requirements (`.995` or higher for gold) plus the specific list of named exceptions including the American Gold Eagle (which is `.9167` fine and would otherwise be excluded by fineness — Congress made an explicit statutory exception in 1986). Bars must be from a refiner meeting the LBMA Good Delivery, COMEX, NYMEX, or NYSE-LIFFE specifications. Privately-minted rounds, Krugerrands, and most non-Eagle sovereign coins below `.995` fine are excluded from IRA eligibility.

The /guides/coins-vs-bars/ guide covers the IRA-eligibility implications for product selection in more detail. The /reviews/gold-ira-companies/ hub covers the named-company landscape.

The 28% maximum long-term gains rate

Long-term capital gains on collectibles, including physical gold held outside an IRA, are taxed at a maximum federal rate of `28%`. The rate compares to the maximum `20%` rate that applies to most non-collectibles long-term gains (and `0%` or `15%` rates for lower-income brackets).

Mechanical detail: the `28%` rate is the maximum. Lower-income taxpayers may pay a lower effective rate. The applicable rate is the lesser of `28%` and the taxpayer's ordinary-income marginal rate. For taxpayers in the top federal brackets the collectibles rate of `28%` is materially higher than the `20%` rate on other long-term gains; for taxpayers in lower brackets the difference may be smaller or zero.

Long-term, for this purpose, means a holding period of more than one year measured from the day after acquisition to the day of sale. Holding for exactly one year is short-term; more than one year is long-term.

Net Investment Income Tax (NIIT): higher-income taxpayers may be subject to an additional `3.8%` NIIT on net investment income, which can include collectibles gains. The combined maximum federal tax burden on long-term gold gains for a high-income taxpayer could therefore reach `28% + 3.8% = 31.8%`. State income taxes apply on top — see the state-sales-tax section below for the separate sales-tax question.

The cost basis for gold gains is the acquisition cost plus the dealer markup, the shipping and insurance paid at purchase, and (where applicable) the assay or grading fee. The proceeds are the net amount received at sale after dealer buyback spread and any commission. Document each step with the dealer's purchase confirmation, the dated LBMA reference price used, the markup, the all-in price paid, and the sale-side confirmation. The /tools/gold-ira-tax-decision-tree-pdf/ provides a structured walk-through; CPAs typically request cleanly-documented cost-basis records on first contact.

Short-term gains — ordinary income

Gold held for one year or less and sold at a gain is taxed at the holder's ordinary-income tax rate, not the long-term-gains rate. For a top-bracket federal taxpayer the ordinary-income marginal rate is currently `37%` — meaningfully higher than the `28%` collectibles long-term rate.

The short-term-vs-long-term distinction matters more for gold than for many other asset categories, because the holding-period difference between `12` months and `13` months can shift the applicable tax rate by roughly `9` percentage points for a top-bracket taxpayer.

Operational implication: where the buyer has flexibility on sale timing, holding past the one-year mark to qualify for long-term treatment is meaningful. Where the buyer does not have flexibility (need for liquidity, scheduled distribution), the short-term rate applies regardless. A CPA-level consult before a near-the-line sale is the appropriate diligence step.

Gold IRAs — tax-deferred (Traditional) or tax-free distributions (Roth)

Gains realized inside a Gold IRA wrapper are not subject to the `28%` collectibles long-term-gains rate. The collectibles rate applies to after-tax holdings outside the IRA wrapper. Inside the wrapper, the tax treatment is determined by whether the IRA is Traditional or Roth.

Traditional Gold IRA: contributions may be deductible in the year contributed (subject to income limits and active-401(k) rules). Gains compound inside the wrapper without annual tax. Distributions are taxed as ordinary income at the holder's marginal rate at distribution. Required minimum distributions (RMDs) begin at age `73`. Distributions before age `59½` may be subject to a `10%` early-withdrawal penalty in addition to ordinary income tax. The tax bill is deferred from contribution to distribution; the rate at distribution is the holder's marginal ordinary-income rate at that time.

Roth Gold IRA: contributions are not deductible. Gains compound inside the wrapper without annual tax. Qualified distributions (after age `59½` and a 5-year holding period) are tax-free. There is no RMD requirement on the original Roth IRA owner under current rules (SECURE Act 2.0 changes affected inherited IRAs but not the original Roth owner). Roth conversion (Traditional-to-Roth) is itself a taxable event in the conversion year — covered in /guides/gold-ira-rollover/ in more detail.

Inside either wrapper, the IRS still requires storage at an IRS-approved depository in identifiable (allocated) form. Home-storage Gold IRAs and unallocated arrangements are not compliant. The /reviews/storage-vaults/ hub covers the approved depository landscape.

The distinction-language to avoid: 'tax-free' is the right term for qualified Roth distributions; 'tax-deferred' is the right term for Traditional. 'Tax-free Gold IRA' as a generic marketing phrase is wrong for Traditional accounts (which are tax-deferred not tax-free) and is the wrong default characterization. The /editorial-standards/ page documents BullionLens' editorial-language policy on this distinction.

Dealer 1099-B triggers

IRS rules require bullion dealers to file Form 1099-B reporting certain customer-side bullion sales to the dealer. The reporting is triggered by specific product-and-quantity combinations rather than by a simple dollar threshold. The IRS rules cite specific bullion-coin and bar specifications that fall within the reporting regime; other products fall outside.

Examples within the 1099-B reporting regime, per the IRS published guidance and dealer-association compliance materials (subject to verification with a CPA for any specific transaction): • Sale of `25` or more 1 oz Krugerrands, Maple Leafs, or Mexican Onzas to a dealer in a single transaction. • Sale of `25` or more 1 oz Austrian Philharmonics to a dealer. • Sale of one or more gold bars meeting certain weight thresholds (the IRS guidance cites specific kilogram and 100-oz-bar thresholds). • Sale of one or more 100-oz silver bars.

Examples explicitly outside the 1099-B reporting regime per current IRS guidance: • Sale of American Gold Eagles, regardless of quantity. (The Eagle was specifically excluded from 1099-B reporting in 1984 IRS guidance.) • Sale of American Gold Buffalos. • Sale of fractional-ounce coins below the listed thresholds.

Important distinction: the 1099-B reporting is on customer-to-dealer sales (the customer sells back to the dealer). The dealer files the form on the customer-side gain. Buyer-to-dealer purchases (the customer buys from the dealer) are not subject to 1099-B reporting — those would, in larger cash-transaction cases, be subject to Form 8300 reporting instead (next section).

The 1099-B filing is informational and reflects the dealer's reporting obligation. It does not change the underlying tax treatment of the sale (which is still governed by collectibles long-term-gains rules for the seller). The seller should expect to receive a copy of the 1099-B and to incorporate it into the tax return for the year of sale.

Form 8300 and cash transactions

Form 8300 is the IRS reporting form a business must file when it receives more than `$10,000` in cash (or in related transactions summing to that amount within a 24-hour window or other related transactions) from one customer. The form was originally established under the Bank Secrecy Act to support anti-money-laundering enforcement.

Bullion dealers fall within the Form 8300 reporting regime for buyer-to-dealer purchases. A customer paying more than `$10,000` cash for bullion at a dealer triggers the dealer's obligation to file Form 8300 reporting the customer's identity, the transaction amount, and the transaction details. The IRS guidance defines 'cash' for this purpose broadly — including US currency, foreign currency, cashier's checks, money orders, traveler's checks, and certain other monetary instruments in some circumstances.

Important exclusion: wire transfers and personal/business checks (drawn on the customer's bank account in the customer's name) are NOT 'cash' for Form 8300 purposes. The threshold for Form 8300 reporting applies to the specific instruments listed in the IRS guidance, not to any payment exceeding `$10,000`. Most large bullion purchases at retail are conducted by bank wire — which falls outside the Form 8300 reporting regime.

Structuring (intentionally splitting transactions to fall under the `$10,000` threshold) is a separate offense under the Bank Secrecy Act, subject to severe penalties independent of the Form 8300 reporting itself. Dealers will not assist customers in transaction structuring, and many dealer terms-of-service explicitly disallow it.

Practical implication for retail buyers: a `$50,000` bullion purchase paid by bank wire is reported neither by Form 1099-B (that's a sell-side form) nor by Form 8300 (wire is not 'cash' for that purpose). A `$15,000` purchase paid in physical cash at a coin shop triggers Form 8300 reporting on the buyer. Document the payment method on the dealer's purchase confirmation.

State sales tax treatment

State sales tax on bullion varies materially across US states. The dominant pattern is to exempt investment-grade bullion above a specified threshold (commonly `$500` or `$1,000` per transaction or per piece), with a minority of states either taxing all bullion or maintaining no relevant exemption.

Indicative 2026-Q2 state treatment (verify with the specific state's department-of-revenue for current rules — this varies over time): • Broad bullion-exemption states: Texas, Florida, Arizona, Washington, Pennsylvania, Ohio, Tennessee, and a number of others have broad exemptions covering investment-grade bullion above their stated thresholds. • Limited-exemption states: California exempts bullion sales above a relatively high threshold (`$2,000` per transaction in most recent guidance); New York exempts bullion sales above `$1,000` per transaction. Both have specific definitional language worth checking with a CPA familiar with the state's rules. • Tax-bullion states (small minority): a small number of states tax bullion fully at the state sales-tax rate. Hawaii, Maine, Massachusetts (with some exemptions), and Vermont have at times fallen in this category, though the rules change.

Many states publish a specific bullion-exemption checklist on the department-of-revenue website. Reputable bullion dealers track these and apply state-specific tax calculation at checkout based on the buyer's shipping address. For purchases shipped to a state with sales-tax exemption above a threshold, the dealer's checkout will apply zero sales tax above the threshold automatically.

Sales tax is paid at purchase and is not a recoverable input cost at sale. For tax-cost-basis purposes (relevant when computing the capital-gains-tax-due-on-sale calculation later), state sales tax paid at purchase increases the cost basis of the bullion and reduces the eventual taxable gain at sale.

Online purchases shipped across state lines follow the destination-state's bullion tax rules (under the Wayfair-era nexus rules for online sales tax). The dealer's checkout will calculate based on the shipping address, not the buyer's billing address or the dealer's state-of-incorporation.

How we sourced this

Citations draw from IRS Publication 550 (2025 edition, Investment Income and Expenses), IRS Publication 590-A and 590-B (2025 editions, Individual Retirement Arrangements), Internal Revenue Code Section 408(m) (the collectibles statute), Internal Revenue Code Section 1(h) (capital gains rate structure including the collectibles rate carve-out), the IRS guidance on Form 1099-B reporting thresholds for precious-metals dealers (IRS Publication 1212 references and related guidance), the Bank Secrecy Act and IRS Form 8300 instructions, and the state-specific department-of-revenue published guidance for each state cited.

The 2026-Q2 state-tax-exemption summary was compiled by cross-referencing each state's department-of-revenue published bullion-tax guidance with the National Retail Sales Tax compendium and contemporary bullion-dealer compliance materials. State rules change; verify before transacting.

We are not a tax adviser. CPA-level review of your specific situation is the appropriate next step before any meaningful transaction. The /tools/gold-ira-tax-decision-tree-pdf/ provides a structured walk-through suitable for use in a CPA conversation.

In plain English

In plain English: gold held in your own name and sold at a gain after a year is taxed at up to 28% federal — higher than the 20% rate on stocks. Held inside a Traditional Gold IRA, gains compound untaxed until distribution, then taxed as ordinary income. Held inside a Roth Gold IRA, qualified distributions are tax-free. Sales of certain coins (Krugerrand, Maple Leaf at 25+ oz) and bars trigger a dealer 1099-B report; American Gold Eagles do not. Cash purchases above $10,000 trigger Form 8300 — but wires are not 'cash' for that purpose. Most states exempt bullion above a threshold, but a few do not. Talk to a CPA before transacting; tax outcomes vary by individual situation.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is the maximum long-term capital gains rate on physical gold?

Under current US tax law, physical gold and most bullion coins are 'collectibles' under IRC Section 408(m). Long-term capital gains on collectibles are taxed at a maximum 28% rate (versus 20% for most other long-term gains). Consult a CPA for your specific situation. -

Are Gold IRAs taxed differently?

Inside a Traditional Gold IRA, gains compound tax-deferred until distribution. Distributions are taxed as ordinary income. Inside a Roth Gold IRA, qualified distributions are tax-free, but contributions are not deductible. -

What triggers a dealer 1099-B report?

IRS rules require dealers to report certain bullion transactions. Examples include sales (by the customer to the dealer) of 25 or more 1 oz gold Krugerrands, Maple Leafs, or Mexican Onzas, and certain bar quantities. Sales of American Gold Eagles are not subject to the same 1099-B reporting. -

What is Form 8300?

Form 8300 is the IRS report a business must file when it receives more than $10,000 in cash (or related transactions summing to that amount) from one customer. Coin and bullion dealers must file Form 8300 on qualifying cash transactions. -

Do all states charge sales tax on bullion?

No. Most states exempt investment-grade bullion above a threshold (Texas, Florida, Arizona, and others have broad exemptions). A minority of states tax bullion fully. Check your state's department-of-revenue published rules.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.