Bullion dealers — the editorial cut

Editorial reviews of online bullion dealers: spreads over spot, shipping policies, return windows, payment methods, and buyback spreads.

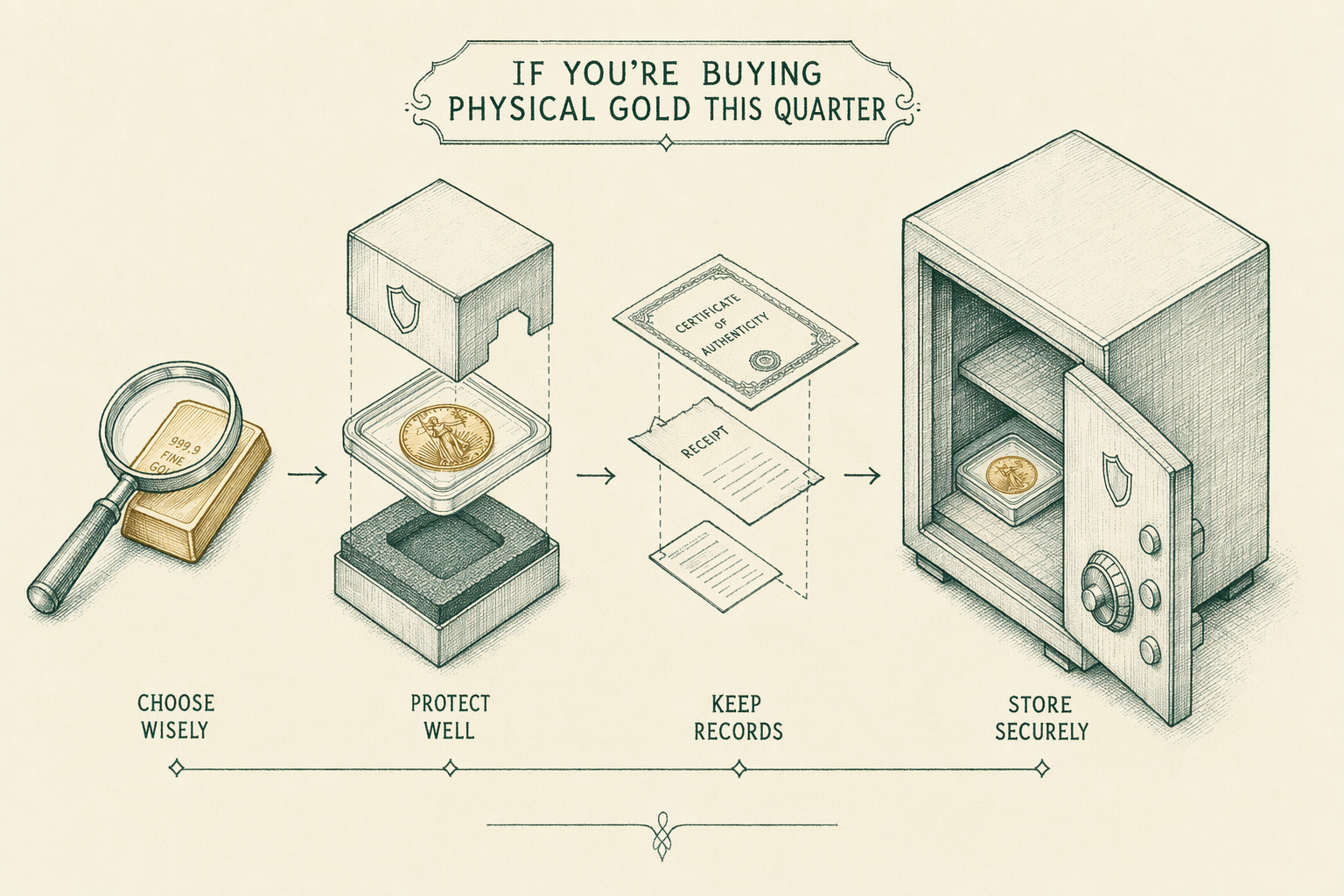

If you're buying physical gold this quarter

If you are buying physical gold this quarter — coins, bars, fractional rounds, sovereign mint or private mint — you have a choice between online bullion dealers, local coin shops, and direct-from-refinery channels (the latter typically gated by minimum order size and KYC). For most retail buyers the online dealer channel is where the volume happens, and the differences between dealers are real: spreads on the same `1 oz` American Gold Eagle can vary `2%`-`3%` between dealers on the same day, payment-method surcharges range from zero (bank wire) to `4%` (credit card), and buyback policies vary from at-spot to spot-minus-`5%` for the same item.

This editorial hub exists to give you the structural picture before you start filling carts. We cover seven major online dealers (APMEX, JM Bullion, Money Metals Exchange, SD Bullion, Provident Metals, BGASC, and Kitco), each with a standalone review under `/learn/` listing the published fee schedule, payment-method surcharges, shipping policy, return window, and buyback terms. Every page that names a dealer carries an affiliate disclosure callout. We earn commission when a reader opens an account through a link on this site; we do not earn commission on the purchase itself or on its dollar amount.

What we evaluate

Five criteria. The first is the spread on common reference items — `1 oz` American Gold Eagle, `1 oz` Canadian Maple Leaf, `1 oz` Krugerrand, `10 oz` LBMA-listed bar, and `1 kg` LBMA-listed bar. Spreads are tracked on a single reference date each quarter; we publish the date with the comparison. The second is payment-method surcharges, particularly the credit-card surcharge that materially affects the all-in cost.

The third criterion is shipping policy: declared-value insurance, signature required, carrier rotation, and the dealer's handling of lost or damaged shipments. USPS Registered Mail and UPS / FedEx with declared-value insurance are the standard; we read the dealer's published policy and note exceptions. The fourth is the buyback policy — under-discussed in the channel and the single most important lever for a buyer planning to hold for a few years and then exit. The fifth is the BBB record and complaint history, alongside any state regulatory matters on file.

Two criteria we do not score on: testimonial collections (self-selected) and the customer-service experience on a phone call (varies by representative). The desk's position is that subjective comparisons collapse the audience's ability to evaluate the page; objective criteria preserve it. Where a dealer has a documented pattern of customer-service issues in the BBB complaint record — a different kind of evidence than testimonials — we note the pattern with the complaint count and category.

The spread mechanics every buyer should understand

A bullion dealer's spread is the gap between the bid price (what the dealer would pay if you sold to them) and the ask price (what they charge if you buy from them). The mid-point sits at or near the LBMA spot fix; the bid sits below it, the ask sits above. For common `1 oz` gold coins at retail, the all-in spread typically runs `2%`-`5%` (`1%`-`3%` on the bid side, `1%`-`3%` on the ask side). For larger formats the spread compresses: a `10 oz` LBMA-listed bar ships at `1%`-`3%` over spot in normal markets, and a `1 kg` (`32.15 oz`) bar can land near `1%` over spot for established customers buying from dealers with active wholesale relationships.

Spread widens in two specific conditions. The first is supply stress: in early `2020` (COVID-era refinery shutdowns) and again in late `2022` (silver market dislocation), retail spreads on common items widened materially, with premiums on American Gold Eagles briefly hitting `10%`-`15%` over spot. The second is illiquid or specialty items: limited-mintage proofs, fractional `1/10 oz` and `1/4 oz` coins, and modern numismatic releases routinely carry spreads above `15%`. The lower the per-ounce dollar amount, the higher the fabrication and distribution cost as a percentage.

Sovereign coin spreads run tighter than private-mint round spreads because sovereign coins carry global resale recognition. An American Gold Eagle, a Canadian Maple Leaf, a Krugerrand, and a Britannia are accepted by every coin shop in the country. A private-mint round (priced as bullion, not as a coin — they are not legal tender) is recognized regionally; the resale market is thinner.

Payment methods and their cost

Bank wire and ACH are the cheapest payment methods at most dealers. A typical wire fee runs `$30`-`$45` per outgoing transfer (paid to your bank, not to the dealer), with no per-transaction surcharge from the dealer side. Some dealers offer a small percentage discount (`1%`-`2%`) for bank wire payment as an inducement, particularly on orders above `$25,000`.

Credit card payment carries a surcharge at almost every major dealer, typically `2%`-`4%`. The surcharge covers the dealer's card-processing cost (roughly `1.5%`-`3%` of the transaction depending on card type) and the chargeback exposure that comes with a high-value reversible product. Treat the credit-card surcharge as a real cost, not a fee that can be negotiated away. A `4%` credit-card surcharge on a `$10,000` order is `$400`, which dwarfs the dealer-spread difference between the cheapest and most expensive dealers in the comparison.

Cryptocurrency payment is offered by some dealers (notably JM Bullion, SD Bullion, and BGASC at various times); pricing varies. PayPal and other consumer-payment platforms are rare at the major dealers because of chargeback risk. Money order, certified check, and cashier's check are accepted by most dealers without a surcharge — slower than wire, no fee. Cash transactions over `$10,000` in aggregate trigger IRS Form 8300 reporting by the dealer.

Shipping, insurance, and signature-required delivery

Standard practice in the channel is USPS Registered Mail or UPS / FedEx with declared-value insurance and signature required on delivery. The shipment package does not disclose the carrier or the dealer (often blank or plain-labeled) and does not declare the contents on the outside; the insurance is arranged underneath. Most dealers ship free on orders above a stated threshold (typically `$199` or `$299` minimum). Below the threshold, shipping runs `$10`-`$25` depending on order size and weight.

If a shipment is lost or damaged, the dealer's published policy controls the recourse. Reputable dealers (the seven covered on this hub) all carry shipping insurance and absorb verified losses without passing them to the buyer; the published policy typically requires signature on delivery and prompt notification (within `24`-`72` hours) of any visible damage to the package. Read the published shipping policy before ordering; we link it on each dealer's standalone review.

Free shipping is a real economic line. A `$10` shipping fee on a `$300` `1/10 oz` gold coin order is `3.3%`, comparable to the spread itself. For small orders, choosing a dealer with a low free-shipping threshold (`$199` rather than `$299`) materially affects the all-in cost. For large orders the shipping fee is rounding error against the spread.

Buyback policies — the under-discussed lever

Buyback policy is the single most under-discussed lever in the channel and the one we spend the most editorial effort on. The published policy controls what happens when you exit: how much under spot the dealer pays, what items the dealer will buy back, how the transaction settles (mailed check, wire, or store credit), and how quickly. Differences here can be larger than the spread differences on the buy side.

Three patterns to look for. The first is at-or-near-spot buyback on items the dealer originally sold you — a documented policy that materially favors the buyer. APMEX, JM Bullion, and Money Metals have all published variants of this policy at various times; we re-confirm the current terms each quarter. The second pattern is fixed-discount buyback (typically spot-minus-`2%` to spot-minus-`5%` depending on the item) — predictable but less favorable. The third pattern is no-published-buyback — the dealer takes case-by-case offers, with the buyer carrying full price-discovery risk at exit. We flag dealers in the third category.

Read the buyback policy before opening the account, not after. The policy that exists on the day you sell is the policy that controls the transaction. Dealers update policies; the snapshot dates on the reviews tell you when we last confirmed the published terms.

Dealers we currently cover

APMEX — Shortlisted. Largest online bullion dealer in the US by volume, broadest product catalog, competitive spreads on sovereign coins, published buyback policy. Standalone review at `/learn/apmex-review/` walks the fee schedule. JM Bullion — Shortlisted. Comparable scale to APMEX, often slightly tighter spreads on specific items in our quarterly checks, similar payment-method structure. Standalone review at `/learn/jm-bullion-review/`. Money Metals Exchange — Shortlisted. Strong published buyback policy, competitive spreads at the small-to-mid order size, retail-friendly interface. Standalone review at `/learn/money-metals-exchange-review/`.

SD Bullion — Editorially Neutral. Aggressive promotional pricing on rotating items; ongoing-day spreads competitive but not consistently the lowest on every product line. Standalone review at `/learn/sd-bullion-review/`. Provident Metals — Editorially Neutral. Mid-scale operator with a stable product mix and standard published policies; competitive on common items, less competitive on specialty. Review at `/learn/provident-metals-review/`. BGASC — Editorially Neutral. Solid mid-tier operator with regional New England presence and a published policy structure that matches peers. Review at `/learn/bgasc-review/`.

Kitco — Editorially Neutral on the dealer side, distinct on the price-data side. Kitco is best known as a published price-data and editorial source; the dealer arm runs alongside. Spreads are competitive on bullion bars, less competitive on coins. Standalone review at `/learn/kitco-review/`.

How we score

The same four editorial tags as the Gold IRA hub: Shortlisted, Editorially Neutral, Mid-tier, Deprioritized. Definitions at `/editorial-standards/`. Shortlisted on the bullion-dealer side means competitive spreads on common reference items in the quarterly check, a published buyback policy on the favorable end of the channel, a clean BBB record, and a payment-method structure with no surprises. Editorially Neutral means parity on the criteria without the additional strengths that elevate a Shortlisted designation.

The tags do not collapse into a numerical score because the criteria do not weight the same for every buyer. A buyer focused on bar formats above `10 oz` will weight spread differently than a buyer focused on `1/10 oz` fractional sovereigns. The tags give you the desk's editorial judgment; the criteria let you do your own weighting. Read the full methodology at `/editorial-standards/`.

Affiliate disclosure for this hub

BullionLens earns a commission when a reader opens an account or makes a qualifying purchase through links on this hub or any linked individual dealer review. The commission is paid by the dealer, not by the reader. It does not change the price the reader pays. The disclosure appears in a persistent callout component on every page that names an affiliate partner, with a link to the methodology at `/editorial-standards/`.

Editorial selection is independent of affiliate paperwork. The seven dealers on this hub were selected based on market footprint, reader demand, and the published fee structure; the affiliate program (where the dealer has one) was signed up separately. Three dealers on the list are Shortlisted; four are Editorially Neutral. The asymmetry — affiliate participation does not buy a Shortlisted tag — is the point of the disclosure model.

Reviewed `2026-Q2`. Dealers will be re-confirmed in `2026-Q3` per the quarterly editorial calendar. Educational content, not personalized investment advice. Consult a licensed adviser before making allocation decisions.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is a bullion dealer's 'spread'?

The gap between the dealer's buy price (what they pay if you sell to them) and ask price (what they charge if you buy). For common 1 oz gold coins this typically runs 2-5% on retail and tighter for institutional volume. -

Are credit card purchases more expensive?

Almost always. Most dealers add 2-4% surcharge for credit card payment versus bank wire or ACH. The surcharge covers the dealer's processing cost and chargeback exposure on a high-value reversible product. -

Is my shipment insured?

Reputable dealers ship via USPS Registered Mail or UPS/FedEx with declared-value insurance, signature required, no insurance carrier disclosed on the package. Read the dealer's published shipping policy before ordering. -

What is a buyback spread?

The discount the dealer applies to their buy price when you sell back. Many dealers will buy at or near spot for items they originally sold you; others quote a discount. Check the dealer's published buyback policy. -

Do bullion dealers issue 1099 reports to the IRS?

On certain transactions yes. IRS Form 1099-B is triggered on dealer purchases of specific quantities of specific products (e.g., 25+ oz of gold bars of certain finenesses). The dealer reports the transaction, not the buyer.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.