Spot vs futures — how gold prices are actually set

Spot, futures, the basis, contango, backwardation. How gold prices form and why your dealer quote differs from the headline number.

The 'spot' price — what it is and who sets it

'Spot' is shorthand for the price of one troy ounce of gold of London Good Delivery standard fineness (995.0 fine or better) for settlement in two business days — the standard OTC convention. The term 'spot' distinguishes it from 'forward' (settlement at an agreed future date) and 'futures' (an exchange-traded standardized contract for future delivery).

There is no single institution that sets the spot price the way a stock exchange sets a closing bell price. The spot price is the prevailing two-way market in continuous OTC trading between bullion banks — institutions like JPMorgan, HSBC, UBS, ICBC Standard Bank, Goldman Sachs, and the LBMA market-making bank membership. These institutions quote bid and ask to each other and to large institutional clients twenty-four hours a day five days a week (with a brief gap on weekends).

The retail tickers you see on Kitco, JM Bullion, APMEX, Bloomberg, and Reuters are streams derived from this OTC quote flow with vendor formatting on top. Different vendors sample at different refresh rates and from different counterparty sources, which is why two retail tickers will commonly differ by `$0.50` to `$3` per ounce at the same instant.

Volume in OTC spot gold materially exceeds volume in any single exchange-traded gold instrument. Bank of International Settlements data suggests global OTC gold trading volume averages multiple multiples of COMEX futures volume — though both numbers are large enough that the distinction matters mainly to academic-research interpretation, not to retail buyer outcomes.

The London Gold Fixing and the LBMA Gold Price

The closest thing to a 'real' published benchmark gold price is the LBMA Gold Price, established in March 2015 as the successor to the historical London Gold Fixing that ran from 1919 to 2015. The LBMA Gold Price is administered by ICE Benchmark Administration (IBA) and is set twice each business day, at 10:30 AM and 3:00 PM London time.

The mechanism is a transparent electronic auction. Participating institutions submit bids and offers; the auction algorithm finds the price at which buy and sell volumes match within a defined tolerance. The methodology is published and audited under the EU Benchmarks Regulation and the UK Benchmarks Regulation. As of 2026-Q2, fifteen accredited institutions are direct participants in the LBMA Gold Price auction, with broader market participation through them.

The LBMA Gold Price (AM and PM fix) is the benchmark cited in institutional contracts — many central bank gold transactions, many ETF rebalancing trades, and many institutional bullion contracts settle at the LBMA fix on a specified date. The price is published in US dollars per troy ounce, and the LBMA also publishes simultaneously-set fixings in euros and pounds sterling for currency-converted reference.

For a buyer or analyst who needs to cite a specific gold price on a specific date — for tax-cost-basis purposes, for a contract reference, for a research piece — the LBMA Gold Price is the appropriate institutional benchmark to cite. The intraday OTC quote stream is appropriate for execution; the LBMA fix is appropriate for citation. This site cites LBMA fixes throughout.

COMEX futures and how they relate to spot

COMEX, the Commodity Exchange division of CME Group, is the dominant exchange-traded gold-futures venue in the United States. The benchmark contract is GC (gold futures), traded in 100 troy ounce contract sizes. A single GC contract represents the obligation to deliver (or take delivery of) `100` ounces of gold of specified fineness at the contract's expiration month at a CME-approved depository.

Most COMEX gold futures contracts do not result in physical delivery. They are closed out (offsetting trades booked) before expiration, with the difference settled in cash. A small percentage of contracts are taken to physical delivery at the CME-approved depositories — and that small percentage is the link between the futures market and the physical-bullion market.

Each COMEX contract month has a distinct price quoted at the exchange. The 'front month' (the nearest-expiration contract) is the most actively traded and the one most often cited as 'the futures price.' Deferred months (subsequent expirations) trade at related but distinct prices reflecting the cost of carrying gold through that period.

COMEX futures prices and OTC spot prices are linked by arbitrage. If futures prices drift significantly above spot, an arbitrageur can buy spot gold, simultaneously sell the matching futures contract, hold the metal to delivery, and lock in the spread. This arbitrage tends to keep the futures-spot relationship anchored. When the arbitrage breaks — usually because of physical-delivery friction, settlement timing, or unusual institutional flows — interesting things happen to the basis.

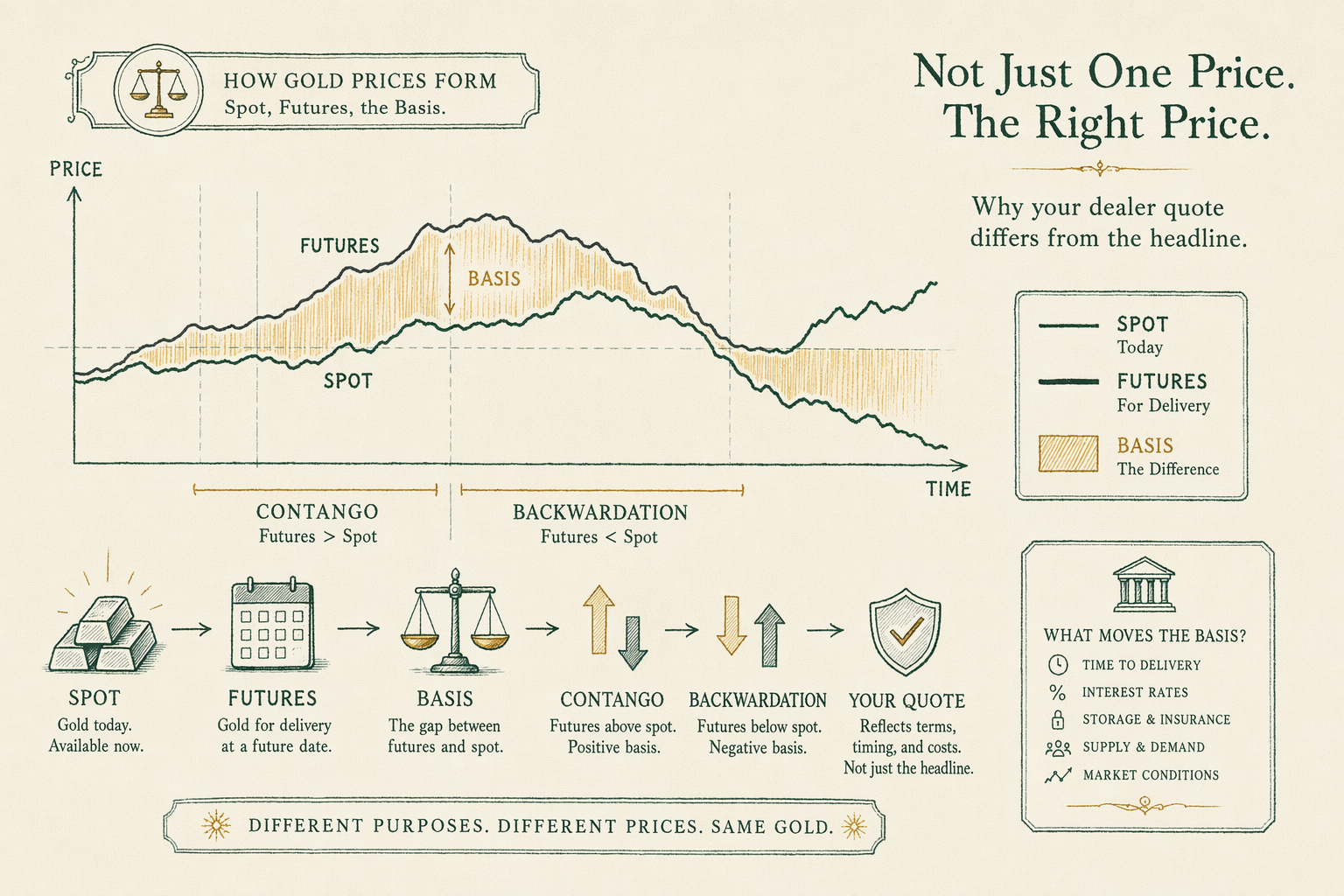

The basis — futures minus spot

The 'basis' in gold-market vocabulary is the difference between the futures price (for a specified delivery month) and the spot price, for the same metal of the same fineness, at the same instant. Expressed in dollars per ounce or as a percentage of spot.

Under normal market conditions, the gold basis is positive — futures trade slightly above spot. This positive basis reflects the cost of carrying gold from today to the futures expiration: the financing cost (you could earn interest on the cash if you did not buy the gold), the storage cost (vault fees), and the insurance cost. The aggregate of these is sometimes called the 'cost of carry.' Under positive-basis conditions (contango — see next section), the basis approximates the riskless interest rate plus storage and insurance.

The basis can also be negative, with futures trading below spot. This condition is called backwardation. In gold markets, backwardation historically signals stress in the physical metal market — concentrated demand for immediate delivery exceeding what can be sourced at the futures price. Backwardation episodes have occurred but are uncommon for sustained periods in gold; they are more common in agricultural commodities where storage is genuinely costly and physical scarcity can spike.

Academic literature distinguishes between the 'simple basis' (front-month futures price minus spot) and the 'calendar basis' or 'spread' (one futures month minus another). For retail buyer interpretation, the simple basis is the relevant metric.

Why this matters for retail buyers: the dealer-quoted price for physical bullion ultimately ties back to the spot-plus-basis structure. When the basis widens because of cost-of-carry components, retail premiums tend to widen with it. When the basis goes negative because of physical-delivery stress, retail premiums on bullion-grade coins can spike disproportionately — early 2020 (early-pandemic supply chain disruption) and late 2022 (residual supply-chain residue plus retail demand) both produced premium spikes well above their normal ranges.

Contango and backwardation in plain English

Contango is the institutional term for the normal state of a gold market: futures prices trading above spot, with progressively later expiration months trading at progressively higher prices. Plain-English translation: it costs money to store gold from today to next year, and the futures market prices that storage cost in.

Backwardation is the institutional term for the unusual state: futures prices trading below spot, with later expiration months trading at lower prices. Plain-English translation: there is so much demand for immediate-delivery physical gold that buyers are willing to pay more for delivery today than for delivery in three months — even after accounting for the cost of carrying gold for three months.

Contango is the regular state of the gold market — by a wide margin of total trading days. Backwardation episodes occur but are typically brief and tied to specific stress events. The 1999-2000 transition period (around the Washington Agreement), early 2020 (COVID-era physical-delivery friction), and late 2022 to early 2023 (residual physical-market stress) are episodes academic researchers have documented as gold-market backwardation events.

Neither contango nor backwardation is itself a trading signal. They are descriptive states of the futures-spot relationship. Some practitioners interpret backwardation as a sign of physical-market tightness; the academic literature is more cautious about reading causal direction.

The vocabulary is genuinely useful for buyers, though, in one specific way: when bullion-dealer premiums on standard 1 oz coins (American Gold Eagle, Canadian Maple Leaf) widen materially above their normal 3% to 7% retail range, checking the COMEX basis is a useful diagnostic. A premium spike during a backwardation episode is a different signal than a premium spike during a contango that has merely widened — the former suggests physical-supply stress, the latter suggests cost-of-carry pricing-in.

Why your dealer quote differs from the spot ticker

The dealer-quoted price for physical bullion is built up from spot through three additive layers. Understanding the layers is the most useful single piece of mental model for a retail buyer reading a dealer screen.

Layer one: the spot reference. The dealer references a spot price stream — either from an exchange data feed, an OTC market data vendor, or (rarely) the LBMA fix as a reference midpoint. The spot reference is updated on the dealer's cadence, typically every few seconds during active trading hours and on the prior LBMA fix during quiet periods.

Layer two: the fabrication and distribution premium. This covers the cost of converting raw refined gold into the specific product (coin or bar), the cost of distribution from the refiner/mint to the dealer's vault, and the dealer's wholesale margin on the inventory. For 1 oz American Gold Eagles, this layer typically runs 2% to 4% over spot in normal markets; for 10 oz and kilo bars it runs 1% to 2%; for proof and specialty issues it runs materially higher.

Layer three: the dealer's retail margin. The dealer's own profit margin on top of fabrication and distribution. Typically another 1% to 3% over spot for established direct-to-consumer dealers; higher for marketing-heavy Gold IRA channels.

Sum: spot plus 3% to 7% over spot for 1 oz bullion-grade coins at retail in normal markets. During stress episodes (early 2020, late 2022) the premium has widened to 10% to 15% on the same coins. The /reviews/bullion-dealers/ hub covers premiums across major dealers; the /tools/gold-silver-ratio-chart/ provides historical price data; the /guides/buying-physical-gold/ guide covers the buyer-side considerations.

The dealer's 'price lock' that engages at checkout is the dealer committing to honor the displayed price for a specified window (often 10 to 30 minutes) while you complete payment. The dealer hedges this exposure by entering its own offsetting transaction — typically buying spot gold or selling COMEX futures matching the lock. If you do not pay within the lock window, the lock typically expires and the price re-quotes.

How we sourced this

Citations draw from the LBMA Gold Price published methodology (administered by ICE Benchmark Administration, currently version 2.3 effective 2023); the CME Group COMEX gold futures contract specifications and the GC contract historical settlement data; Bank for International Settlements OTC derivatives volume reports for global gold-market sizing; and the academic literature on commodity-market basis behavior — Working (1949), Telser (1958), and more recent gold-specific studies including Aulerich, Fishe, and Harris (2014) on COMEX delivery mechanics.

Retail premium ranges were compiled by comparing published advertised premiums at major direct-to-consumer dealers (APMEX, JM Bullion, Money Metals Exchange, SD Bullion, Provident Metals) at multiple snapshot points across 2024-2026 against contemporaneous LBMA Gold Price fixings. Stress-episode data was triangulated against bullion-dealer press releases, World Gold Council market notes, and contemporary financial news coverage from the relevant periods (early 2020, late 2022).

In plain English

In plain English: 'spot' is a continuous OTC market quote, not a single set price. The LBMA fix at 10:30 AM and 3:00 PM London time is the closest thing to an official daily benchmark. Futures (COMEX GC) trade slightly above spot in normal markets — that gap is called contango, and it just means it costs money to store gold for a year. When the gap goes negative (backwardation) it usually means physical-supply stress. Your dealer's quoted price for a 1 oz coin is spot plus 3% to 7% under normal conditions, plus another 5% to 10% during supply-stress windows. The dealer's price lock at checkout commits the dealer to honor the quote for 10 to 30 minutes while you pay.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Who sets the spot price of gold?

There is no single setter. The LBMA Gold Price is a twice-daily auction-based benchmark set by participating banks. Continuous OTC trading between dealers and banks updates spot 24/5. Retail tickers reflect this stream with vendor markups. -

What is COMEX?

The Commodity Exchange division of CME Group, the largest gold and silver futures venue. COMEX gold futures (symbol GC) trade in 100 oz contracts, settling either by physical delivery or cash. -

What is the 'basis'?

Futures price minus spot price for the same delivery month. Positive basis (contango) usually reflects storage costs and interest rates. Negative basis (backwardation) historically signals supply stress in the physical market. -

Why is the dealer price higher than the spot quote?

Dealers add a premium covering fabrication, distribution, dealer margin, and shipping. For 1 oz sovereign coins at retail, 3-7% over spot is typical.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.