Gold IRA rollover — the editorial mechanics

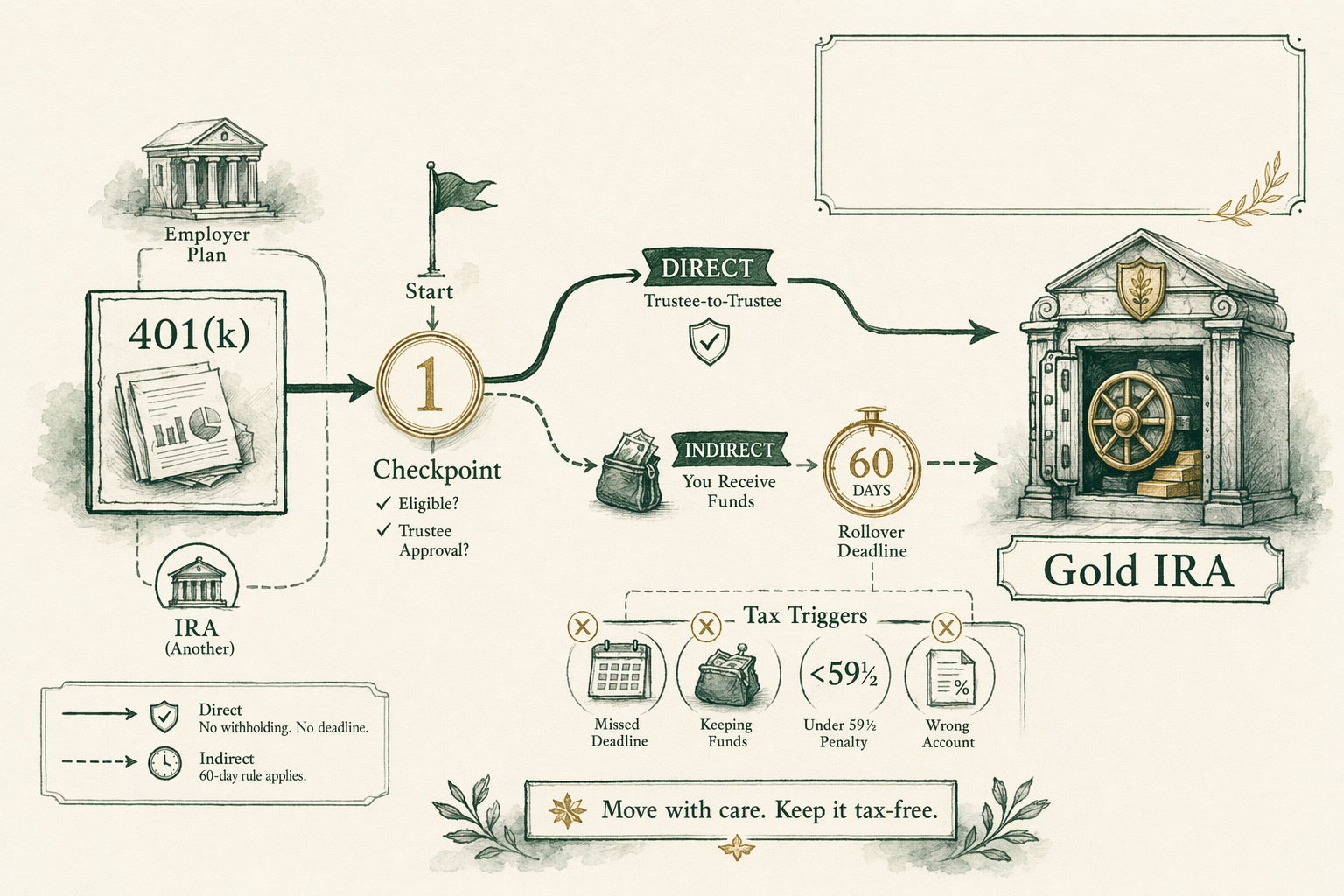

How a Gold IRA rollover works in practice: direct vs indirect, 60-day rule, employer plan vs IRA-to-IRA, and the mistakes that trigger tax events.

Rollover vs transfer — the IRS distinction

Per IRS terminology, a 'transfer' is a trustee-to-trustee movement of funds between two IRAs of the same type — say, a Traditional IRA at one custodian to a Traditional IRA at another. The money never lands in your personal name. The distributing custodian sends the assets directly to the receiving custodian. There is no Form 1099-R, no Form 5498-related reporting friction, and no 60-day rule to worry about. The IRS does not even classify a clean trustee-to-trustee transfer as a 'rollover' in the technical sense.

A 'rollover,' in the strict IRS sense, involves either (a) movement across plan types — for example, a 401(k) to an IRA, an IRA to a 401(k), or a 403(b) to an IRA — or (b) any movement of IRA funds that does land in your personal name first, with the intention that you re-deposit it into another IRA within 60 days.

Why the distinction matters: rollovers are reported on IRS Form 1099-R (by the distributing plan) and IRS Form 5498 (by the receiving custodian). Both forms must reconcile on your tax return for the IRS to treat the rollover as a non-taxable event. The IRS also limits IRA-to-IRA rollovers to one per twelve-month period across all your IRAs combined — a rule the IRS clarified after the 2014 Bobrow Tax Court decision.

Most well-run Gold IRA setups, despite the 'rollover' marketing terminology, are actually executed as trustee-to-trustee transfers when moving from a prior IRA to a new self-directed Gold IRA. The 'rollover' language is imprecise but ubiquitous in the Gold IRA marketing vocabulary. If your prior account is already an IRA, ask the receiving custodian to structure the move as a trustee-to-trustee transfer; the paperwork is materially simpler and you avoid the one-rollover-per-twelve-months rule.

Direct rollover from an employer 401(k)

If your retirement assets currently sit in an employer-sponsored 401(k) or 403(b), the path into a Gold IRA crosses plan types. This is a true rollover, not a transfer, regardless of how cleanly it is executed.

The first question is whether your current 401(k) plan permits the rollover at all. The IRS rules permit it only on a 'distributable event' — typically separation from the sponsoring employer, reaching age 59½, the death or disability of the participant, or specific in-service withdrawal provisions if your plan's Summary Plan Description allows them. An active employee under age 59½ at the sponsoring employer usually cannot roll over the active 401(k) balance unless the plan permits an in-service withdrawal. Read the Summary Plan Description before initiating any rollover paperwork on the Gold IRA side.

Assuming the distributable event applies, the cleanest path is the direct rollover, sometimes called the 'plan-to-plan' rollover. Your 401(k) administrator sends the distribution check made payable to the new Gold IRA custodian 'For the Benefit of [your name],' typically by check mailed to the new custodian or by wire to the new custodian's banking instructions. The funds never land in your personal name.

On a direct rollover, the 401(k) administrator reports the gross distribution on Form 1099-R with distribution code 'G' (direct rollover, non-taxable). The receiving Gold IRA custodian reports the contribution on Form 5498 as a rollover contribution. Your tax return shows the gross distribution on Form 1040 line 5a but $0 as taxable on line 5b, with 'Rollover' written next to it per the IRS instructions.

Direct rollovers are not subject to the 20% mandatory federal withholding that applies to certain indirect rollovers (see next section). This is the operational reason direct rollovers are strongly preferred over indirect rollovers for any meaningful balance.

Indirect rollover and the 60-day rule

An indirect rollover occurs when the distributing plan or IRA cuts a check payable to you personally rather than to the receiving custodian. You then have 60 calendar days from receipt to deposit the funds into the receiving Gold IRA. Miss the window and the amount becomes a taxable distribution with possible 10% early-withdrawal penalty if you are under 59½.

Indirect rollovers from an employer 401(k) carry an additional operational hazard: 20% mandatory federal income tax withholding. If your 401(k) cuts a $100,000 check to you personally, the plan administrator is required by IRS rules to withhold $20,000 against potential income tax liability, so the check you receive is $80,000. To complete the rollover and avoid a taxable distribution, you must re-deposit the full original $100,000 into the receiving Gold IRA within 60 days — meaning you have to come up with $20,000 from other funds to make the receiving custodian whole. The $20,000 withheld eventually comes back as a refund when you file your tax return, but in the interim you have a 60-day cash gap.

Indirect rollovers from an IRA to an IRA do not carry the 20% withholding rule but are still subject to the 60-day deadline and the IRS one-rollover-per-twelve-months limit. The Bobrow Tax Court decision (2014) clarified that the twelve-month limit applies across all IRAs an individual holds, not separately per IRA — a constraint many Gold IRA marketing pages still misrepresent.

The 60-day window starts on the date you receive the funds, not the date the distributing plan sent the check. Mail transit time is counted against the deadline. There is a narrow IRS hardship waiver process for missed-deadline rollovers under Revenue Procedure 2016-47, but reliance on the waiver is operationally risky.

The practical guidance is to avoid indirect rollovers wherever the distributing plan offers a direct-rollover option. Most 401(k) plans and all reputable IRA custodians offer direct rollover. The indirect rollover is for the edge case where the distributing plan does not.

IRA-to-IRA trustee-to-trustee transfer

When the source account is already a Traditional IRA, Roth IRA, SEP-IRA, or SIMPLE IRA, the cleanest path into a self-directed Gold IRA is a trustee-to-trustee transfer rather than a rollover. The receiving Gold IRA custodian initiates the request by sending the prior custodian a transfer request form signed by you authorizing the movement.

The prior custodian liquidates the relevant assets (if held in securities) or wires cash directly to the receiving custodian. The cash never lands in your personal name. There is no Form 1099-R, no 60-day rule, no withholding, and no one-rollover-per-twelve-months limit. The IRS does not classify the movement as a reportable distribution.

Trustee-to-trustee transfer paperwork typically takes 5 to 15 business days from form submission to funds arriving at the receiving custodian, depending on how the prior custodian processes the request. Some legacy custodians still process by mailed paper check; others have moved to direct wire. The receiving Gold IRA custodian should be able to give you a realistic expected window when they initiate the request.

If the source IRA is held in mutual funds, ETFs, or individual securities, the prior custodian will liquidate the holdings as part of the transfer (selling them on the market and wiring cash) unless you specifically request an in-kind transfer of identical securities, which is not relevant for a Gold IRA destination because the receiving Gold IRA custodian cannot hold securities. Plan for the liquidation timing and the brief market exposure between sale at the prior custodian and metal purchase at the receiving Gold IRA company.

If the source is a Roth IRA, the destination Gold IRA must also be set up as a Roth Gold IRA. A Traditional-to-Roth conversion is a separate, taxable event and should not be combined with the transfer unless that is the explicit intent — and only after consultation with a CPA on the tax implications of the conversion.

Required paperwork and timing

On the source-account side: the distribution request form from your prior plan administrator or IRA custodian, signed and notarized if the plan requires it. Most 401(k) plans require a signature; spousal consent may be required if the plan is subject to the Retirement Equity Act of 1984. A small subset of plans require a Letter of Acceptance from the receiving custodian — a one-page document the receiving Gold IRA custodian will produce on request.

On the receiving-account side: the self-directed IRA application with the new custodian, completed and submitted with identity verification documents. Most custodians have moved this to a fully online process; a minority still require wet-signature on a printed application. After account approval, the rollover or transfer request form is the next document.

On the bullion-purchase side: a purchase confirmation from the Gold IRA marketing company specifying the bullion-grade product, the dated LBMA Gold Price spot reference used, the markup, the all-in per-coin price, the quantity, and the destination depository. Read this confirmation carefully before authorizing the wire from the custodian to the marketing company. The /guides/gold-ira-fees-explained/ guide covers the markup question in detail.

On the depository side: the storage agreement, which carries the depository's insurance disclosure, the segregated vs commingled designation, and the access procedures. Read this before signing — depositories typically require an explicit segregated-vs-commingled election at account open, and changing it later is operationally cumbersome.

Realistic timing from initial Gold IRA application to settled metal-in-the-depository: 3 to 6 weeks for a clean rollover or transfer from a cooperative prior custodian, 6 to 10 weeks if the prior plan administrator processes by paper check or requires a Letter of Acceptance. Build calendar buffer; the IRS deadlines on indirect rollovers do not flex for processing delays.

The mistakes that trigger tax events

Five mistakes consistently turn what should be a non-taxable rollover into a taxable distribution event. We list them here because each one is documented in IRS hardship-waiver applications under Revenue Procedure 2016-47, meaning real people have made them.

First, missing the 60-day window on an indirect rollover. The most common cause is mail-transit delay on either the distribution check from the source plan or the deposit check to the receiving custodian. Use direct rollover or trustee-to-trustee transfer wherever possible to eliminate the 60-day risk entirely.

Second, using indirect rollover when the source is a 401(k) and not coming up with the 20% withheld portion from other funds within 60 days. If the 401(k) withholds $20,000 from a $100,000 distribution and you only deposit the $80,000 you received, the missing $20,000 is treated by the IRS as a taxable distribution. The 20% withholding rule on 401(k) indirect rollovers is the single highest-frequency source of unintended tax events in this category.

Third, exceeding the one-rollover-per-twelve-months limit on IRA-to-IRA rollovers. Per the Bobrow Tax Court decision, the limit applies across all IRAs the taxpayer holds. Trustee-to-trustee transfers do not count against the limit and are the operationally cleaner path.

Fourth, attempting an in-service rollover from an active 401(k) without confirming the plan's Summary Plan Description permits it. Many active 401(k) plans do not allow in-service withdrawals for participants under 59½. Confirm with the plan administrator before initiating any paperwork on the Gold IRA side.

Fifth, accidentally converting a Traditional IRA to a Roth Gold IRA in the rollover paperwork rather than maintaining the same tax type. A Traditional-to-Roth conversion is a taxable event triggering income tax on the converted amount. If the intent is to maintain tax-deferred status, the destination account must be a Traditional Gold IRA. Read the receiving custodian's account-type confirmation before authorizing the funds movement.

All five mistakes share a single mitigation: ask the receiving custodian to document, in writing, the IRS code applicable to the specific movement (rollover vs transfer, plan type, distribution code that will appear on Form 1099-R) before you sign any paperwork. A custodian who will not produce this documentation in writing is not the right custodian for the move.

How we sourced this

Citations in this guide draw from IRS Publication 590-B (2025 edition, Distributions from Individual Retirement Arrangements), IRS Publication 575 (Pension and Annuity Income), Revenue Procedure 2016-47 (the hardship-waiver framework for missed 60-day deadlines), and the 2014 Tax Court decision Bobrow v. Commissioner (T.C. Memo. 2014-21) which clarified the one-rollover-per-twelve-months limit. The 20% mandatory withholding rule cites IRC Section 3405(c).

Operational details on processing timing, paperwork friction, and Letter of Acceptance requirements were compiled from a sample of major self-directed IRA custodians' published procedures as of 2026-Q2. Procedural details vary between custodians and change over time; verify the current procedures with the specific custodians involved in your move.

Affiliate disclosure

BullionLens earns a commission when readers open Gold IRA accounts through links on our reviews and comparison pages. Commission does not change the rollover procedures or the fees you are quoted. Editorial selection is independent — see /editorial-standards/. The reviews carry a 'Last reviewed' date and are revisited quarterly.

In plain English

In plain English: most Gold IRA 'rollovers' are technically trustee-to-trustee transfers, which are simpler and safer. Use a direct rollover (or transfer) wherever the source plan offers it. Avoid getting the money in your personal name. If you absolutely cannot avoid an indirect rollover, mark the 60-day deadline on a calendar and account for the 20% withholding if the source is a 401(k). Ask the receiving custodian to put the IRS distribution code in writing before you sign. Talk to a CPA before doing any of this — the cost of the consult is negligible against the tax cost of getting the procedure wrong.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is the difference between a rollover and a transfer?

Per IRS terminology, a 'transfer' is trustee-to-trustee movement between IRAs of the same type and is not reported as a distribution. A 'rollover' specifically involves distributing funds (or moving funds across plan types, e.g., 401(k) to IRA) and has reporting requirements. -

What is the 60-day rule?

If you receive a distribution from a retirement account and intend to roll it into another, you have 60 calendar days from receipt to deposit it in the receiving account. Miss the window and the amount becomes a taxable distribution with possible 10% early-withdrawal penalty if you are under 59½. -

Can I roll over my current 401(k)?

Only if you have a 'distributable event' — typically separation from the employer, reaching age 59½, or specific in-service withdrawal provisions if your plan allows them. Active 401(k)s with current employers usually cannot be rolled. -

What forms are involved?

Form 1099-R from the distributing plan reports the gross distribution. Form 5498 from the receiving custodian reports the rollover contribution. Both must reconcile on your tax return.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.