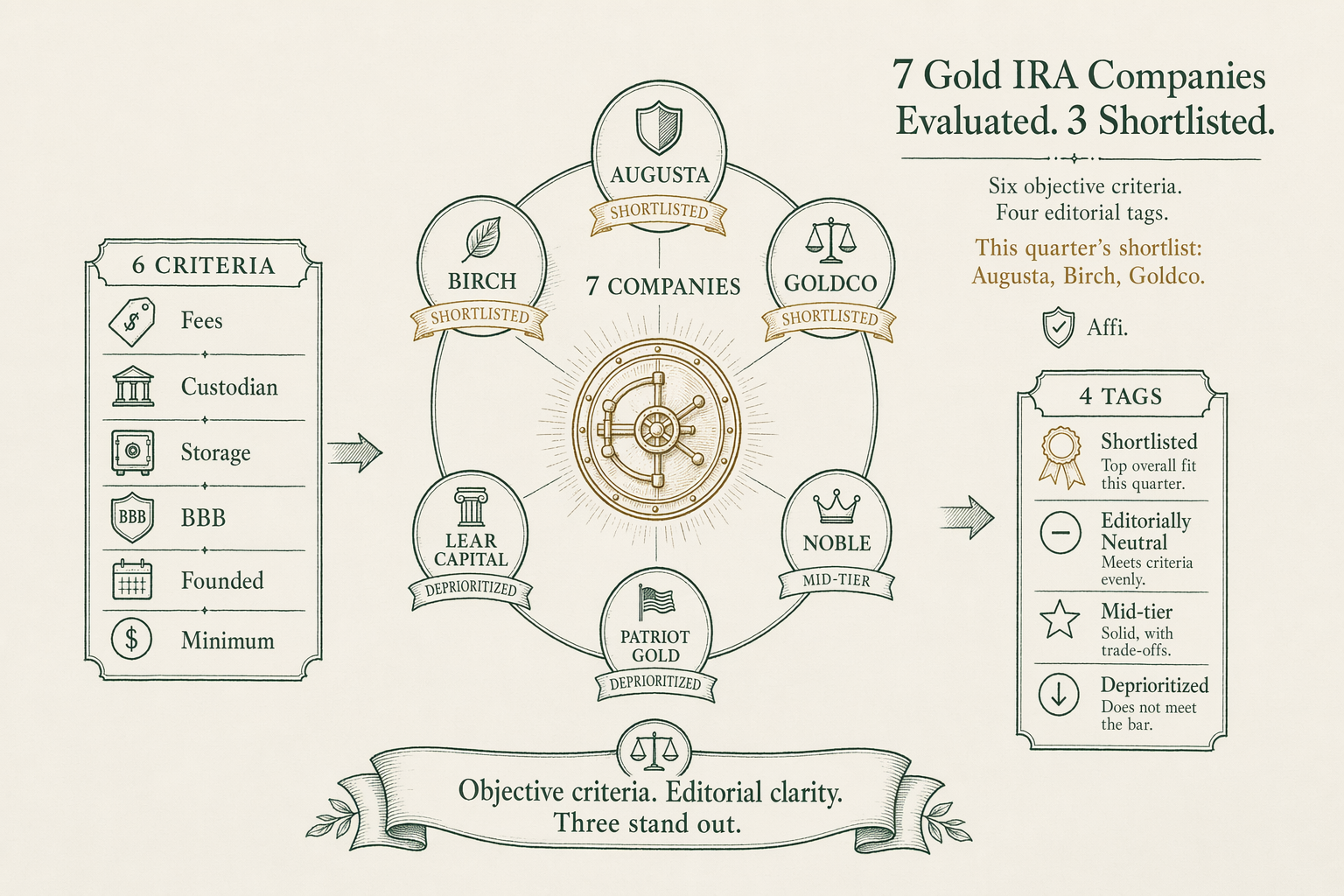

Gold IRA companies — the editorial cut

Independent editorial coverage of Gold IRA companies: fee structures, custodian relationships, storage partners, BBB records, and founded-year context.

If you're rolling over retirement assets, start here

If you are rolling over a `401(k)` or considering a `$50,000`-and-up move into a precious-metals IRA, the marketing channel you are about to walk into is structured around commissioned phone sales. Each company has its talking points. Each rep has a target. The fee schedule, the custodian relationship, the storage partner, the buyback policy — these are knowable, documented facts. The sales pitch is not where you learn them.

This editorial hub exists to give the reader the documented facts before the sales call. We compare Gold IRA companies on six objective criteria: published fees, custodian relationship, storage partner, BBB grade and complaint count, founding year, and minimum investment. We do not score on marketing material, sales-call experience (varies by representative), or testimonial collections (self-selected). Every fee in every review is followed by a snapshot date and a source link. Every page that names a company carries an affiliate disclosure callout, because we earn commission when a reader opens an account through a link on this site.

What we evaluate

Six criteria, weighted in the order of dollar impact on the first-year account economics. The first and largest is the published fee schedule, particularly the markup over spot on the initial coin or bar purchase. A `$50,000` rollover into a `12%`-over-spot specialty proof coin allocation pays roughly `$6,000` to the dealer before the account has done anything else; the same `$50,000` into a `5%`-over-spot bullion-grade allocation pays `$2,500`. The markup line is where most of the first-year cost actually lives, and it is the line most commonly under-disclosed in marketing materials.

The second criterion is the custodian relationship. The Gold IRA marketing company is rarely the custodian. The custodian is the IRS-recognized trust company that administers the account, files the annual `Form 5498` reporting, and handles the in-kind distribution mechanics. Equity Trust, STRATA Trust, Kingdom Trust, GoldStar Trust, and IRA Financial are the most common custodians in the channel. Custodian quality determines reporting accuracy and account portability. A company that refuses to name its custodian is a flag.

The third criterion is the storage partner. The depository is the IRS-approved vault that physically holds the metal. Delaware Depository, Brink's Global Services, International Depository Services of Texas or Delaware, HSBC, and JPMorgan are the largest. The depository's insurance arrangements, audit cadence, and segregation policy all matter; we read the published storage agreement before publishing a company review.

The fourth criterion is the BBB record, including the grade, the complaint count by category for the trailing three years, and any consent orders or pending matters. The fifth is the founding year — a company with a `20-year` operating record has a longer documented track record than a company founded in `2019`. The sixth is the minimum investment, because the minimum drives who the company is actually marketed to: minimums above `$50,000` indicate a different go-to-market than minimums at `$10,000`.

Companies we currently cover

The current coverage list, alphabetical: Augusta Precious Metals, American Hartford Gold, Birch Gold Group, Goldco, Lear Capital, Noble Gold Investments, and Preserve Gold. Each company has a standalone review under `/learn/` with the full fee snapshot, custodian list, storage partners, BBB record, founding year, and editorial verdict. The comparison pages under `/compare/` walk pairwise comparisons against the same criteria.

Snapshot dates for the most recent quarterly review cycle: `2026-Q2`. Companies will be re-confirmed in `2026-Q3` per the editorial calendar at `/editorial-standards/`. Fee schedules and storage partners change; the numbers on the page are accurate as of the snapshot date, not the publication date. Where a company has changed its fee schedule between snapshots, the change is annotated inline with the date of the change and a link to the source.

Augusta Precious Metals charges a `$50` application fee, an `$80/yr` IRA custodian fee through Equity Trust, and an additional `$100/yr` storage fee with Delaware Depository for segregated allocated storage. Birch Gold Group lists a `$50` application fee, an `$80/yr` custodian fee through Equity Trust or STRATA Trust depending on plan, and `$100/yr` storage with Delaware Depository or Brink's. Goldco's published structure runs `$50` application, `$100/yr` custodian, and `$100/yr` storage with similar partners. American Hartford Gold publishes a flat `$180/yr` combined custodian-plus-storage on accounts above a stated threshold, with the underlying custodian relationship through Equity Trust. Each of those figures is dated to the company's published fee schedule as of `2026-Q2`; we relink the source on each company's full review.

Editorial verdicts in two sentences each

Augusta Precious Metals — Shortlisted. Strongest published-fee transparency in the coverage list, with a stable Equity Trust custodian relationship and a consistent Delaware Depository storage partnership; minimum investment of `$50,000` excludes smaller rollovers. The Augusta review at `/learn/augusta-precious-metals-review/` walks the fee schedule line by line.

Birch Gold Group — Shortlisted. Long operating history (founded `2003`), multi-custodian flexibility (Equity Trust and STRATA Trust depending on plan), and a competitive published fee schedule. The Birch review at `/learn/birch-gold-group-review/` walks the custodian-choice mechanics.

Goldco — Shortlisted. The most aggressive promotional structure in the channel (storage-fee waivers on qualifying first-year accounts), tempered by a fee schedule that becomes standard at year two; minimum investment `$25,000`. The Goldco review at `/learn/goldco-review/` covers the promotional-vs-ongoing economics.

American Hartford Gold — Editorially neutral. Lower minimum investment than the shortlisted companies (`$10,000` for cash purchase, higher for IRA), a flat custodian-and-storage fee structure that is straightforward to read, and a shorter operating record than Augusta or Birch. The AHG review at `/learn/american-hartford-gold-review/` walks the fee transparency and the structural shorter-track-record point.

Noble Gold Investments — Editorially neutral. Storage flexibility (Texas IDS in addition to Delaware Depository) and a moderate minimum, with a smaller scale than the shortlisted companies. The Noble review at `/learn/noble-gold-investments-review/` covers the Texas storage option in depth.

Lear Capital — Mid-tier. Documented historical regulatory matters that the desk treats as material; we link to the consent order and complaint records in the full review at `/learn/lear-capital-review/`. Buyers should read those records before opening an account. The fee schedule itself is unremarkable; the regulatory record is the editorial point.

Preserve Gold — Mid-tier. Newer entrant (founded `2022`) with a thinner public record than the longer-operating companies on the list; the desk re-evaluates each quarter as the BBB record matures.

How we score

The four editorial tags — Shortlisted, Editorially Neutral, Mid-tier, Deprioritized — carry definitions on the editorial standards page. Shortlisted means the company meets all six objective criteria at the median or better, with a clean regulatory record and a fully published fee schedule. Editorially Neutral means the company meets the criteria at parity with peers, without the additional strengths that elevate a Shortlisted designation. Mid-tier means the company has at least one documented criterion (operating record, fee transparency, regulatory record) materially weaker than the Shortlisted peers, with the specific weakness linked in the review.

The tags do not collapse into a numerical score because the desk's position is that subjective scoring obscures the criteria rather than clarifying them. A reader who cares about fee structure above all else will read the comparison differently than a reader who cares about operating record above all else. The tags let the reader see the desk's editorial judgment without erasing the underlying criteria.

Where two companies are roughly equivalent on the objective criteria, the verdict says so. "On the fee schedule and custodian footprint, Augusta and Birch are within `5%` of each other; reader preference will turn on minimum-investment fit and on the specific Delaware Depository segregation tier each company offers" is a defensible verdict and we use it when it is true. Read the full methodology at `/editorial-standards/`.

Affiliate disclosure for this hub

BullionLens earns a commission when a reader opens an account with Augusta Precious Metals, Birch Gold Group, Goldco, American Hartford Gold, Noble Gold Investments, Lear Capital, or Preserve Gold through links on this hub or any linked individual review. The commission is paid by the company, not by the reader. It does not change the price the reader pays or the fees the company quotes. The disclosure appears in a persistent callout component on every page that names an affiliate partner, with a link to the methodology page at `/editorial-standards/`.

Editorial selection is independent of affiliate paperwork. The seven companies on this hub were selected based on market footprint, reader demand, regulatory record, and the published fee schedule; the affiliate program (where the company has one) was signed up separately. The editorial side of the desk does not see the commission rate when evaluating a company. Two of the companies on the coverage list (Preserve Gold and Lear Capital) have weaker editorial verdicts than the other five despite affiliate program availability — that asymmetry is the point of the disclosure model.

Reviewed `2026-Q2`. Companies will be re-confirmed in `2026-Q3` per the quarterly editorial calendar. Educational content, not personalized investment advice. BullionLens is not a registered investment adviser; consult a licensed adviser before making rollover or allocation decisions.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is a Gold IRA?

A self-directed Individual Retirement Account that holds IRS-approved physical gold (and silver, platinum, palladium) instead of paper securities. It must be administered by a qualified custodian and stored at an IRS-approved depository. -

Is a Gold IRA tax-free?

No. A Traditional Gold IRA is tax-deferred — gains compound without annual tax, but distributions are taxed as income. A Roth Gold IRA's qualified distributions are tax-free, but contributions are not deductible. -

What fees should I compare?

Application/setup fee, annual custodian fee, annual storage fee (segregated vs commingled), markup over spot on the initial purchase, buyback spread, and wire transfer fees. -

Who is the custodian and why does it matter?

The custodian is the IRS-recognized trust company holding the account. The Gold IRA marketing company is often separate from the custodian. Custodian quality determines reporting accuracy and account portability. -

Can I store Gold IRA gold at home?

Not without significant IRS risk. The IRS has taken the position that home-storage Gold IRAs do not satisfy Section 408(m) requirements. Use an IRS-approved depository. -

How often are reviews updated?

Quarterly minimum. Each review carries a 'Last reviewed' date and snapshot fees as of that date.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.