Buying physical gold — the editorial guide

How to buy physical gold without getting burned: spot price mechanics, coin vs bar tradeoffs, dealer selection, shipping, and the resale market.

If you are buying gold for the first time

If you are buying physical gold for the first time — perhaps as part of a `5%`-`15%` portfolio insurance sleeve, perhaps as a generational store of value, perhaps simply because you want to hold an asset that does not require a screen — the channel you are about to walk into is structured around dealers selling commoditized inventory at small margins. The product itself is interchangeable across dealers (a `1 oz` American Gold Eagle from APMEX is the same coin as a `1 oz` American Gold Eagle from JM Bullion). The differences live in spread, payment method, shipping, and the buyback policy that controls your eventual exit.

This guide walks the structural mechanics: how the spot price actually forms, the tradeoff between coins and bars, the difference between sovereign mints and private mints, how to choose a dealer, what to do with the gold when it arrives, and how the resale market actually works. The desk does not recommend a specific dollar amount, a specific allocation percentage, or a specific entry point. Those decisions belong with a licensed adviser who knows your circumstances. What we can do is point at the right questions.

What we evaluate (the buyer's checklist)

Six items, in the order of dollar impact. The first is the spread over spot on the specific product you are buying — typically `2%`-`5%` for common `1 oz` sovereign coins, `1%`-`3%` for `10 oz` bars and larger, and meaningfully higher for fractional coins (`1/10 oz`, `1/4 oz`) and specialty proofs. The second is the payment-method surcharge, particularly the `2%`-`4%` credit-card surcharge that dwarfs most dealer-to-dealer spread differences.

The third is the dealer's published shipping policy — declared-value insurance, signature required, no contents disclosed on the package, prompt-notification window on visible damage. The fourth is the buyback policy, which controls your exit economics years from now and varies more than the spread does on the entry side. The fifth is the dealer's BBB record and any state regulatory matters. The sixth is the storage plan: where the metal goes when it arrives, who insures it, and what happens if a fire or theft occurs.

Three items we do not list: which 'expert' said what about gold this week, what the headline price chart did over the past `30` days, and whether some major economy is about to do something dramatic. The first is signal-free noise. The second is a poor reason to buy or not buy. The third is a forecast and we do not act on forecasts.

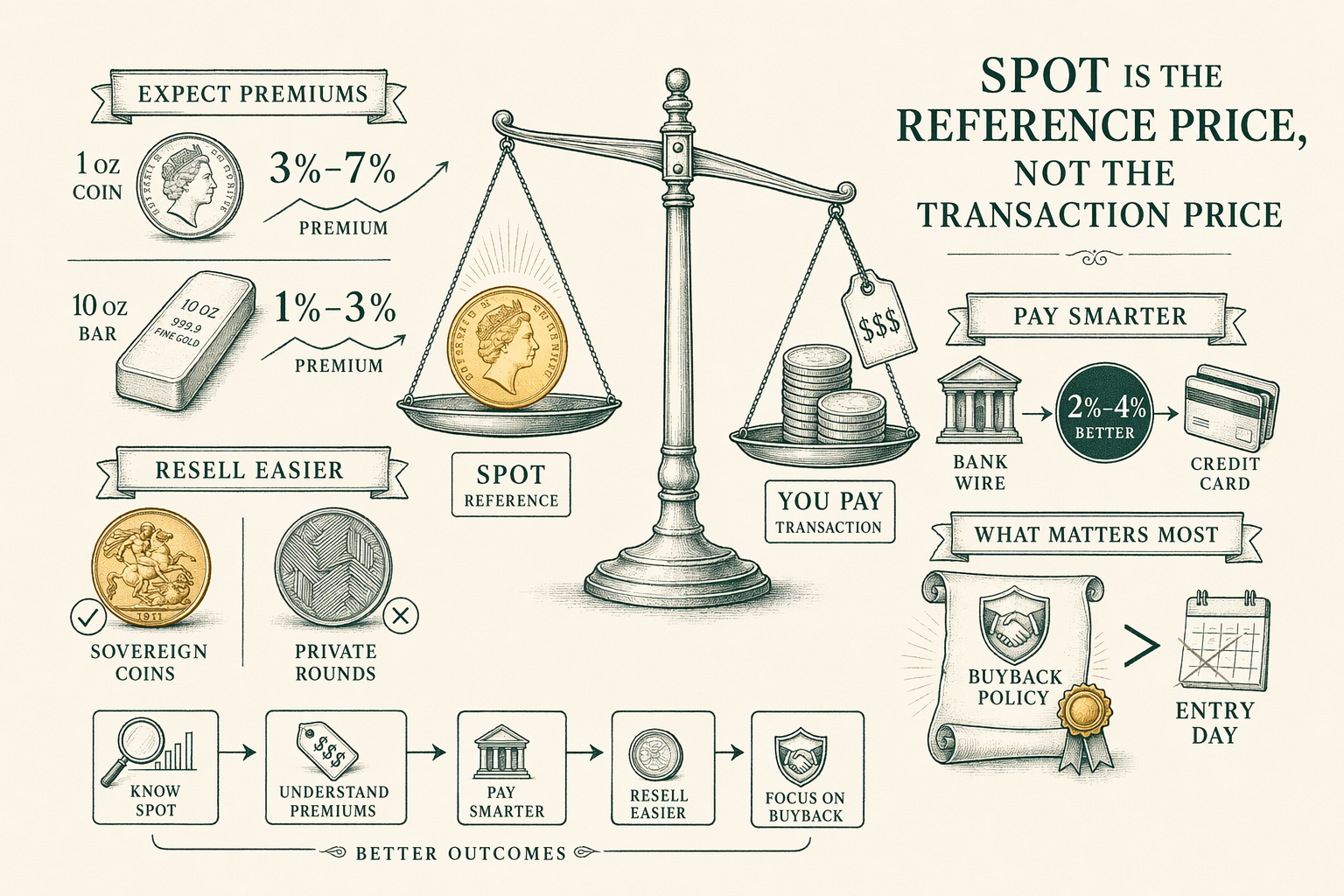

What 'spot price' actually means

The spot price of gold is the reference price for immediate delivery of one troy ounce of gold of specified fineness, set by global OTC trading. There is no single price-setter. The LBMA Gold Price is a twice-daily auction-based benchmark set by participating banks (the morning fix at `10:30 GMT`, the afternoon fix at `15:00 GMT`); the LBMA fixings are the most widely cited benchmarks for documentation and contracts. Continuous OTC trading between dealers and banks updates spot `24/5`; retail tickers (Kitco, JM Bullion, BullionVault) reflect this stream with vendor-specific formatting.

What you see on a retail ticker is not what your dealer will charge you. The dealer's quote includes a premium over spot covering fabrication, distribution, dealer margin, and shipping. For `1 oz` sovereign coins at retail, the all-in dealer price typically runs `3%`-`7%` over the published spot reference. For `10 oz` and `1 kg` bars, the premium compresses to `1%`-`3%`. The premium is the dealer's product; spot is the reference point, not the transaction price.

Spot dispersion of `$0.50`-`$3` between different retail sources on the same day is normal. The LBMA fix is the documented benchmark for contracts; the streaming retail tickers are indicative-only references with vendor markups and refresh-rate differences. For the most up-to-date documentation see the LBMA's published methodology.

Coins vs bars — when each makes sense

Coins carry higher premiums over spot than bars; bars compress to lower premiums as the format gets larger. A `1 oz` sovereign coin (Eagle, Maple Leaf, Krugerrand, Britannia) at retail runs `3%`-`7%` over spot. A `10 oz` LBMA-listed bar runs `1.5%`-`3%`. A `1 kg` (`32.15 oz`) bar runs `1%`-`2.5%`. A `400 oz` London Good Delivery bar — the institutional benchmark format — sits near `0.5%`-`1%` above the wholesale price, but the minimum order size (a single bar at ~`$1M` at current prices) excludes most retail buyers.

The case for coins despite the premium is liquidity and recognition. Sovereign coins are accepted by every coin shop in the country on resale. They carry global legal-tender status. They divide naturally into small denominations the seller can move in pieces. The case for bars is cost per ounce. For buyers planning to hold a single position for years and unwind through a single dealer-buyback transaction, the per-ounce savings on a `10 oz` or `1 kg` bar materially outweigh the resale-flexibility cost.

Most retail buyers end up with a mixed allocation: a stack of `1 oz` sovereign coins for resale flexibility, plus a `10 oz` or `1 kg` bar for the bulk of the position. The split is not formulaic. A buyer planning to gift portions of the holding over time will want more `1 oz` coins. A buyer planning to hold the position intact for a multi-decade horizon can rationalize a larger bar with a smaller sovereign-coin tail.

Sovereign mint vs private mint

A sovereign coin is produced by a government mint (the US Mint, the Royal Canadian Mint, the Perth Mint, the South African Mint, the Royal Mint). Sovereign coins enjoy legal-tender status in their home jurisdiction, global resale recognition, and tighter retail spreads. The American Gold Eagle, the Canadian Maple Leaf, the Krugerrand, the Britannia, and the Australian Kangaroo are the five most-traded sovereign gold coins in the channel.

A private-mint round is produced by a private refiner or mint and priced as bullion. They are not coins (no legal-tender status) and they do not carry numismatic premium. Common producers include PAMP Suisse, Credit Suisse (now part of UBS), Sunshine Minting, and Republic Metals. The spread on private-mint rounds runs lower than sovereign coins of the same weight — typically `1%`-`3%` over spot on `1 oz` rounds versus `3%`-`7%` on `1 oz` sovereigns — at the cost of thinner resale market depth and weaker global recognition.

The choice is a tradeoff between entry cost and exit liquidity. For most retail buyers planning to hold for multiple years, the sovereign-coin premium pays for itself at exit when the resale market is `100%` recognition and the coin shop offers spot-minus-`1%` or better. For institutional-scale buyers running through wholesale dealer relationships, the private-mint round saves real dollars on the entry side. Both formats are appropriate; the framing of one as 'better' than the other collapses the decision.

Choosing a dealer

Online dealers compete on spread, payment-method structure, shipping policy, and buyback terms. The seven dealers covered at `/reviews/bullion-dealers/` (APMEX, JM Bullion, Money Metals Exchange, SD Bullion, Provident Metals, BGASC, Kitco) are the major channel and the desk's coverage list. Spreads on the same `1 oz` American Gold Eagle vary `2%`-`3%` across these dealers on any given day; the cheapest dealer on Monday may not be the cheapest on Wednesday.

Three structural items matter more than the spot-day spread comparison. The first is the buyback policy: dealers with at-or-near-spot buyback on items they originally sold materially favor the buyer at exit, sometimes by `2%`-`5%` of the total holding value. The second is the payment-method structure: if you plan to pay by bank wire, the credit-card surcharge differential is irrelevant; if you plan to pay by credit card, it is the largest line item after the spread itself. The third is the BBB record: dealers with documented complaint patterns in 'shipping' or 'refund' categories deserve weight on those specific issues.

Local coin shops are a separate channel with different economics. A well-established local shop (`5`+ years operating record, BBB profile, physical address) can be a good resource for sovereign coins, partial-stack acquisition, and the occasional in-person transaction below the IRS Form 8300 threshold. The spread on retail coin-shop transactions is typically a few percentage points wider than the cheapest online dealer; the tradeoff is in-person verification and immediate possession. Test small before scaling.

Payment, shipping, and storage on arrival

Bank wire is the cheapest payment method at most dealers. The wire fee is paid to your bank (`$30`-`$45` per outgoing wire typically), the dealer rarely charges a per-transaction surcharge, and some dealers offer small percentage discounts (`1%`-`2%`) for bank wire as an inducement on larger orders. Credit card payment carries a `2%`-`4%` surcharge at almost every major dealer; the surcharge covers card-processing cost and chargeback exposure on a high-value reversible product.

Shipping is USPS Registered Mail or UPS / FedEx with declared-value insurance and signature required. Standard practice is no carrier or contents disclosed on the outside of the package; the insurance is arranged underneath. Most dealers ship free above a stated threshold (`$199` or `$299` typically); below the threshold, shipping is `$10`-`$25` depending on order size and weight. If you are buying for the first time, plan to be present for signature on delivery day or have a trusted recipient present.

On arrival, inspect the package before signing. Verify the contents against the order, weigh the items on a digital scale (`±0.01g` accuracy), and check the serial numbers on assay-card products. Storage decisions are downstream: home safe with appropriate fire rating and bolt-down, bank safe-deposit box with separate scheduled-valuables coverage, or private vault depending on the dollar value of the holding. The storage decisions are the same whether you bought from a sovereign mint or a private mint; the physical item is what matters, not its origin label.

Resale mechanics

There are three resale channels for retail-held gold. The first is the online dealer where you bought it (or another major online dealer); reputable dealers buy back at or near spot for items they originally sold and at spot-minus-`2%` to spot-minus-`5%` for items they did not. The second is the local coin shop; typical prices run slightly under online dealer buyback, with the tradeoff being immediate settlement and no shipping risk. The third is the refinery channel for institutional quantities; refineries pay highest for sufficient volume but minimums are typically multi-kilo.

Never accept the first offer. Spread between buyback offers from different reputable dealers can run `2%`-`4%` on the same item; the few minutes of price discovery routinely save more than the original purchase-spread differential. If selling more than a few items, consider splitting the lot across two dealers to maintain price discovery on a second transaction.

IRS reporting on dealer purchases (you selling to the dealer) is triggered on specific quantities of specific products. `25` or more `1 oz` gold Krugerrands, Maple Leafs, or Mexican Onzas trip the dealer's `1099-B` reporting obligation. American Gold Eagles do not trip the same reporting due to a long-standing carve-out. The buyer's own capital-gains reporting on Schedule D is a separate obligation that applies regardless of the dealer's `1099-B`.

Common pitfalls and how to avoid them

First pitfall: buying numismatic or 'rare' coins from a dealer that pushes them harder than bullion-grade. Numismatic premium varies; numismatic coins are valued for collectability, not weight. A `1 oz` numismatic coin at `$2,800` may be worth `$2,800` to a numismatic collector — or `$2,100` to a coin shop the next day if the numismatic premium evaporates. For buyers focused on the metal-content thesis, bullion-grade is the appropriate format. The numismatic market is a different market.

Second pitfall: paying for storage you did not need. Some Gold IRA marketing companies package private 'depository' arrangements outside the IRA channel at storage fees materially above the IRS-approved depository tier. For after-tax holdings, a home safe or a bank safe-deposit box with a scheduled valuables rider is often the appropriate solution at a fraction of the cost of marketed-storage services. Match the storage tier to the holding value.

Third pitfall: ignoring the buyback policy until you want to sell. The policy that exists on the day of sale is the policy that controls. If the dealer's policy at purchase was at-spot buyback and the dealer has since changed it to spot-minus-`5%`, that change applies. Re-read the dealer's published buyback policy annually as part of a portfolio-review cadence; switch dealers if the policy has materially deteriorated.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Should I buy coins or bars?

Coins (American Gold Eagle, Canadian Maple Leaf, Krugerrand) carry a higher premium over spot but are more liquid in retail markets. Bars (1 oz, 10 oz, kilobar) carry lower premiums but resale options are narrower. Mix is common. -

What is a 'sovereign mint' coin?

A coin produced by a government mint (US Mint, Royal Canadian Mint, Perth Mint). Sovereign coins enjoy legal-tender status and global recognition, supporting tighter resale spreads. -

How much premium over spot is reasonable?

For 1 oz sovereign gold coins, 3-7% over spot at retail is typical. For 10 oz and kilo bars, 1-3%. Premiums spike during supply stress (early 2020, late 2022) — buyers paid 10-15% over spot on Eagles. -

Is buying gold from a local coin shop safe?

It can be, if the shop is established (5+ years, BBB record, physical address). Test small first. Cash transactions over $10,000 trigger IRS Form 8300 reporting by the dealer. -

How do I sell gold I already own?

Major online dealers buy back what they originally sold at or near spot. Local coin shops pay slightly under spot. Refineries pay highest for institutional quantities. Never accept the first offer.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.