Gold for retirees

Editorial guide to gold and Gold IRAs for retirees: RMD mechanics on physical-gold IRAs, spending-account strategies, and estate planning considerations.

If you are 65+ and holding (or considering) a Gold IRA

If you are over `65` and either holding a Gold IRA already or considering one as part of a late-stage portfolio adjustment, the operational questions are different than they are for a `45`-year-old in accumulation. The RMD age (currently `73` under SECURE 2.0) is closer than it is for younger holders. The spending question — how to actually use the IRA for living expenses — is closer or already here. Estate planning matters. Beneficiary mechanics matter. The headline 'is gold a good investment' question is genuinely less urgent at this stage than the mechanics of holding, distributing, and inheriting it.

This guide walks the four practical issues that come up most often in reader questions from this audience: how RMDs work on a physical-gold IRA, the in-kind distribution rules that determine whether the metal ships to your door or is sold for cash, the cash-flow planning options for using the IRA in retirement, and the estate planning considerations including step-up-in-basis treatment and beneficiary mechanics under current tax law. The desk does not deliver personalized recommendations; the material below points at the questions worth bringing to your CPA and licensed adviser.

What this guide covers

Four sections, in the order most readers encounter the issues. First, the `73`+ RMD mechanics on a Gold IRA: how the RMD is calculated against a physical-metal holding, how the depository's published bar values translate into IRS-acceptable RMD math, and what your custodian needs from you to process the distribution. Second, the choice between in-kind metal distribution (the metal ships to you or to an addressable depository) and cash distribution (the depository sells the metal at depository-quoted prices and the custodian wires the cash).

Third, spending-account strategies: pairing the Gold IRA distribution stream with the rest of your retirement income (Social Security, pension, Roth, taxable brokerage), and the sequencing decisions that affect lifetime tax burden. Fourth, inheritance: what happens to a Gold IRA at death, how beneficiary IRAs work under the SECURE 2.0 amendments, the step-up-in-basis rules for after-tax precious-metals holdings, and the documentation that makes the inheritance transition smooth rather than messy.

Each section ends with a 'questions to ask your CPA / adviser' shortlist. The desk publishes educational material; the licensed professionals you hire deliver the personalized answer.

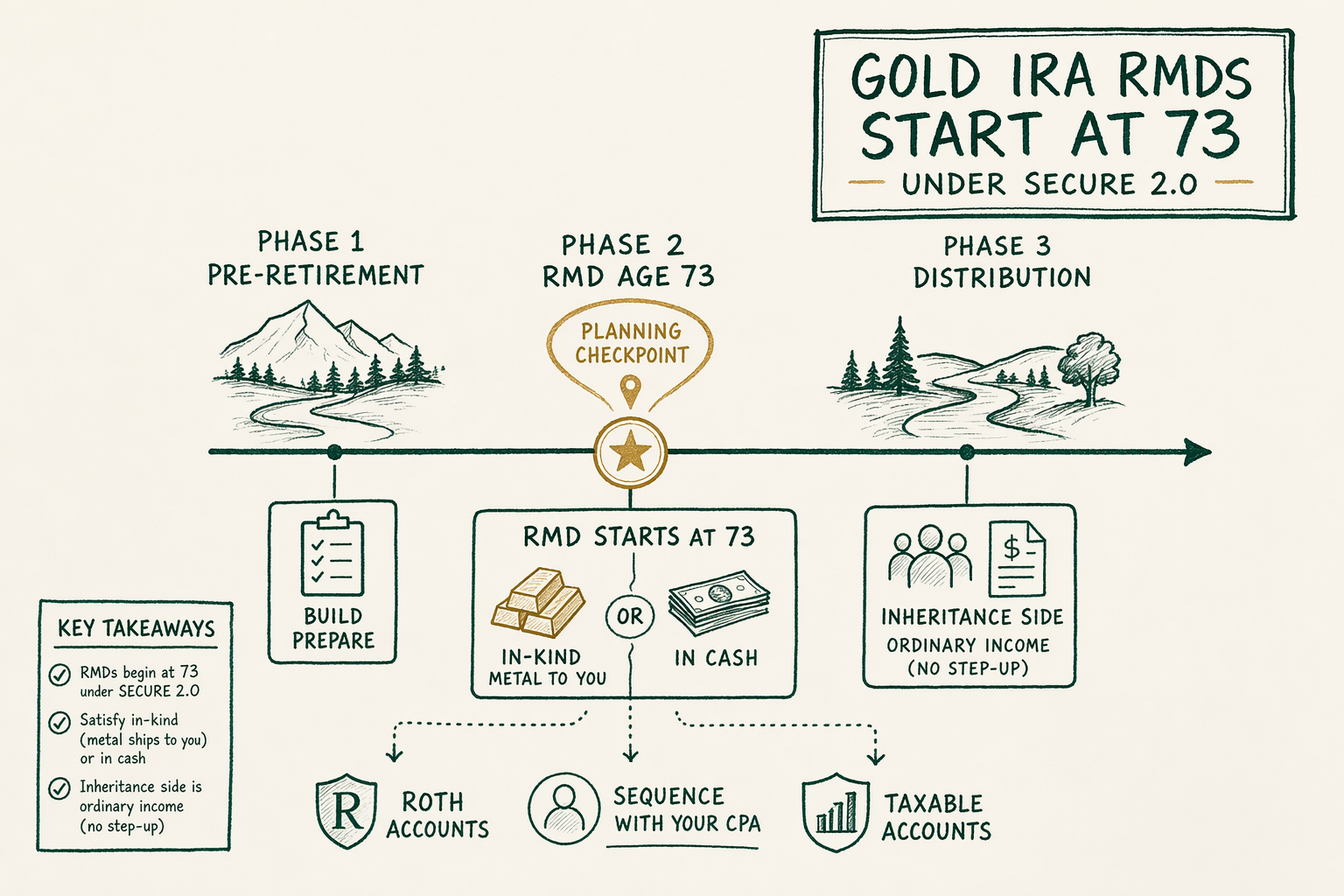

The 73+ RMD reality

Required Minimum Distributions on a Traditional Gold IRA begin at age `73` under current SECURE 2.0 rules (this was raised from age `72`, and is set to rise again to age `75` in `2033`). The RMD is calculated against the prior-year-end account value, divided by an IRS-published life-expectancy factor from the Uniform Lifetime Table. For most retirees the first-year RMD lands at roughly `3.65%`-`4.0%` of the prior-year-end balance, rising slowly each subsequent year.

On a physical-gold IRA the calculation works the same way, with one operational wrinkle. The prior-year-end account value is the depository's published valuation of the metal as of `December 31` of the prior year — typically the depository's bid price for the specific items held, or the spot reference applied to the relevant tonnage. Your custodian publishes the year-end statement and the RMD calculation on it. Read the statement when it arrives; if the valuation looks off relative to public reference prices, query the custodian before relying on the number.

The RMD is satisfied by withdrawing the required amount from the account during the calendar year. On a Gold IRA the withdrawal can take two forms (covered in the next section): in-kind metal distribution, where the underlying bars or coins ship to you or to an addressable destination, or cash distribution, where the depository sells the metal and the cash is wired to you. Either form satisfies the RMD; the choice affects the operational mechanics and the tax-reporting mechanics.

In-kind metal distribution mechanics

In-kind distribution means the depository ships the actual metal to you (or to another addressable destination, including a private vault outside the IRA wrapper). The metal leaves the IRA wrapper at fair market value on the distribution date, and the distribution is reported on Form `1099-R` at that value. From the IRS perspective the transaction is a normal IRA distribution; the difference from a stock-IRA distribution is that the asset arriving in your hands is physical metal rather than a stock-account brokerage entry.

Operationally, in-kind distribution requires the depository to release the specific bars or coins (in a segregated-allocated arrangement) or the equivalent weight in pooled-allocated arrangements. Shipping is via the depository's secure-logistics partner (typically Brink's or a comparable carrier) with declared-value insurance and signature required. Shipping fees for the distribution are typically `$50`-`$200` depending on the weight and distance; the depository publishes the fee schedule with the storage agreement.

Cash distribution is the alternative. The depository sells the metal at depository-quoted prices on the sale date (typically at or near the LBMA spot reference minus the depository's quoted bid-side spread). The proceeds are wired to the custodian, who then distributes the cash to you. Form `1099-R` reports the cash amount. Cash distribution is operationally simpler; in-kind distribution preserves the physical asset and gives you the option to store it outside the IRA wrapper afterward. The choice depends on whether you want the metal or the cash for the underlying spending need.

Spending-account strategies

Most retirees holding a Gold IRA also hold other retirement-asset categories: Social Security, a pension or annuity stream, a Roth IRA or Roth `401(k)`, a taxable brokerage account, and sometimes after-tax precious-metals holdings outside the IRA wrapper. The sequencing decision — which account to draw from first — affects the lifetime tax burden, the size of the eventual estate, and the flexibility of late-stage adjustments.

The general framing in the tax-planning literature (the desk emphasizes 'general framing' because the personalized answer depends on your fact pattern) suggests drawing from taxable accounts first, Traditional IRAs in the middle as RMDs require, and Roth assets last to preserve tax-free compounding. On a Gold IRA specifically, the additional consideration is whether to liquidate the metal or distribute it in-kind. For a retiree with a strong preference to retain the physical asset, in-kind distribution into an after-tax allocated-storage arrangement preserves the holding at the cost of the depository's transfer fees.

Pairing decisions are personalized. The questions worth asking a CPA: what is the effective marginal tax bracket in the year of distribution, does pulling the Gold IRA RMD trigger Social Security taxation or Medicare IRMAA brackets, and what is the right Roth-conversion strategy alongside the RMD draw. The answers depend on income, filing status, and state residency. The desk does not deliver them.

Inheritance and step-up basis

Beneficiary IRA rules apply at death of the IRA holder. Under current law (SECURE 2.0), non-spouse beneficiaries typically must distribute the inherited IRA within `10` years of the original holder's death (with limited exceptions for eligible designated beneficiaries — minor children of the decedent, disabled or chronically ill individuals, and individuals less than `10` years younger than the decedent). Spouse beneficiaries retain the option to treat the inherited IRA as their own. Inside a Gold IRA wrapper the beneficiary mechanics are the same as any other IRA; the inheritance asset is still subject to ordinary-income taxation on distribution.

Step-up in basis applies to assets held outside an IRA at death. For after-tax precious-metals holdings (coins or bars stored at home, in a bank safe-deposit box, or in a private non-IRA vault), the cost basis at death typically steps up to fair market value at the date of death for capital-gains purposes — so the heir's eventual sale is taxed only on appreciation after the inheritance, not the original holder's appreciation. Gold IRA assets do NOT get step-up treatment; the IRA wrapper means the asset is distributed as ordinary income to the beneficiary.

The tax-planning implication, where it matters: some retirees deliberately liquidate a portion of the Gold IRA and re-purchase equivalent metal in a taxable after-tax arrangement before death, accepting the current-year tax cost in exchange for the eventual step-up at death. Whether this is the right strategy depends on the holder's expected longevity, the estate's overall composition, and the heirs' specific tax positions. Talk to a CPA who handles estate planning — this is exactly the type of decision where personalized advice pays for itself.

Estate planning with allocated storage

Allocated storage (specific bars or coins registered to you by serial number) simplifies the estate-administration mechanics versus unallocated arrangements. In an allocated arrangement the executor inherits a documented inventory: bar serial numbers, weights, refiners, and the depository's registration records. The estate's metal holdings can be valued precisely at the date-of-death price reference, transferred to heirs in kind, sold for cash, or split as the will directs.

Documentation matters more here than most retirees expect. The depository's records, the custodian's account records, the IRA beneficiary designation (which controls inheritance separately from the will for IRA-wrapped holdings), and any state-specific estate-administration considerations all need to align. Mismatch between the IRA beneficiary designation and the will is a common source of post-death disputes; the beneficiary designation typically controls for IRA assets, and that fact often surprises heirs. Confirm the beneficiary designation matches your current intentions periodically.

For larger estates, additional considerations include estate tax (federal threshold currently above `$13M` per individual and indexed annually), state-level estate or inheritance taxes (which vary widely), and the practical questions of whether to use trusts, family limited partnerships, or other vehicles for the after-tax precious-metals portion of the estate. These are estate-planning-attorney decisions; the desk's role is to point at the questions, not to answer them.

Recommended next steps

Three pointers. For the RMD and rollover mechanics — both the inflow side (rollover from a `401(k)` if you have not yet) and the outflow side (RMDs from the IRA) — start with `/guides/gold-ira-rollover/` for the IRS rule mechanics. For the company-side question of which Gold IRA custodian or marketing company to use, the editorial coverage is at `/reviews/gold-ira-companies/`; minimum investment, custodian relationships, and storage partners are detailed in the standalone reviews.

For the storage-side question of segregated vs commingled allocated storage at IRS-approved depositories, see `/reviews/storage-vaults/` — the depository on your specific account is set by the custodian, and the comparison detail there walks Delaware Depository, Brink's, IDS, HSBC, and JPMorgan. Comparison pages under `/compare/` walk pairwise comparisons between specific companies and specific depositories.

For the personalized tax-and-estate side, find a CPA and an estate-planning attorney with experience in retirement-asset and precious-metals planning. The licensed professionals deliver the personalized answer; the desk gives you the editorial framing to ask better questions when you sit down with them.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Do I have to liquidate gold to satisfy RMDs?

No. In-kind distribution of metal counts toward the RMD at fair market value. You can take physical possession of the metal or have it sold for cash, your choice. -

What happens to a Gold IRA at death?

Beneficiary IRA rules apply per current tax law. Inherited Gold IRAs follow the same beneficiary mechanics as any IRA, with distribution timing rules updated under SECURE 2.0. Estate planning with a tax adviser is essential. -

Where do I go next?

Start with the linked topic hub for a deeper foundation, then the comparison page that matches your selection criteria. Every claim about a company carries a snapshot date — confirm current arrangements before committing. -

Is this personalized advice?

No. BullionLens publishes editorial coverage, not personalized investment advice. Use this material to understand the landscape, then consult a licensed adviser for your specific situation.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.