How do RMDs work on a Gold IRA?

RMD mechanics for Traditional Gold IRAs: when they start, how to calculate, in-kind vs cash distribution, and the tax implications of taking metal.

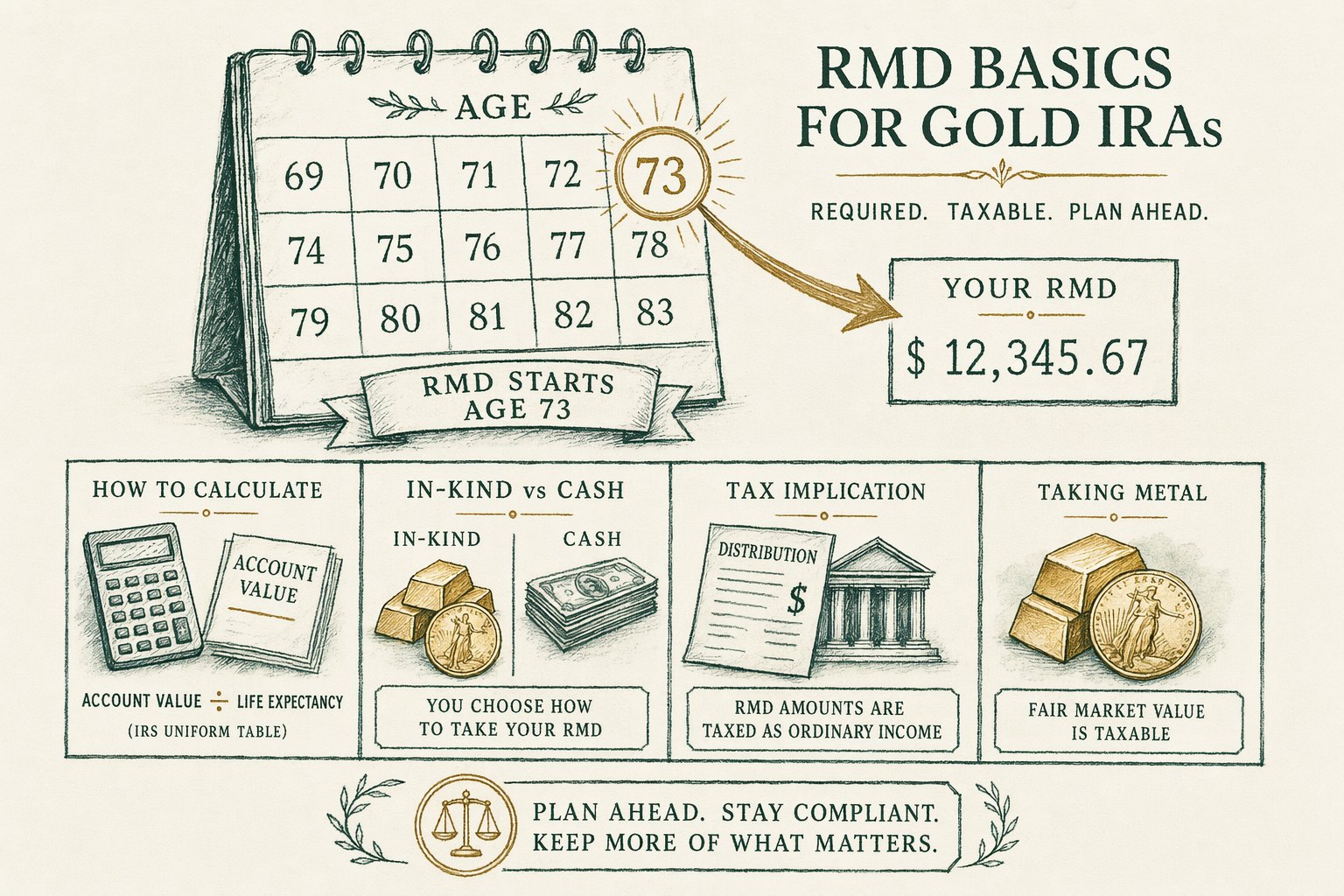

When RMDs begin under current law

Under the SECURE 2.0 Act of 2022, the age at which RMDs begin for Traditional IRAs is `73` for individuals who reach age `72` after December 31, 2022, and `75` for individuals who reach age `74` after December 31, 2032. (The earlier SECURE Act of 2019 had moved the age from `70½` to `72`; SECURE 2.0 moved it again.) The first RMD must be taken by April 1 of the year following the year in which the IRA holder reaches the applicable age. Subsequent RMDs are due by December 31 of each year.

Important distinction: Roth IRAs — including Roth Gold IRAs — generally have NO RMD requirement during the original owner's lifetime. Roth IRAs are funded with after-tax dollars and the IRS does not have a deferred-tax claim to collect. RMDs apply to Traditional IRAs (and inherited IRAs), not to Roth IRAs in the original owner's hands. Beneficiaries of inherited Roth IRAs are subject to the inherited-IRA RMD rules, which were materially changed by the SECURE Act in 2019.

Verify the applicable age and effective date against current IRS guidance — Congress amends the RMD age periodically and the rules have moved in recent years.

Calculating the RMD amount

The RMD calculation for a Traditional Gold IRA uses the same formula as for any Traditional IRA: prior-year December 31 fair market value of the IRA divided by the IRS Uniform Lifetime Table divisor for the holder's current age.

The IRA custodian (Equity Trust, STRATA, etc.) is responsible for reporting the December 31 fair market value on Form 5498 each year. For a Gold IRA, that fair market value is the depository's reported valuation of the held metal — typically based on the LBMA daily fix on December 31 of the reporting year, applied to the troy ounces held.

Example: an IRA holder is age `74` in `2026-Q4`. The Uniform Lifetime Table divisor at age `74` is `25.5`. The IRA's December 31, 2025 fair market value (per Form 5498) was `$510,000`. The 2026 RMD is `$510,000 ÷ 25.5 = $20,000`. The holder must take at least `$20,000` from the IRA by December 31, 2026. Verify the current Uniform Lifetime Table divisors against the IRS table — they update with longevity adjustments.

Cash distribution vs in-kind distribution

An RMD can be taken in two ways from a Gold IRA: cash distribution (the custodian sells metal at the depository, the proceeds are paid to the IRA holder) or in-kind distribution (the actual metal is shipped to the IRA holder, with the fair market value at the date of distribution counted as the RMD amount).

**Cash distribution**: The custodian instructs the depository to sell the required quantity of metal, the bullion is sold into the dealer/wholesale market, and the cash proceeds (less any sale-side costs) are wired to the IRA holder. This is straightforward operationally and produces a clear cash amount for tax purposes.

**In-kind distribution**: The custodian instructs the depository to release physical metal to the IRA holder, typically via insured shipment. The fair market value of the released metal at the date of distribution counts as the RMD amount for tax purposes. The holder then owns the physical metal personally (outside the IRA) and can hold or sell it independently. A secure-shipment fee applies (typically `$100-$500` depending on the value and security level of the shipment).

The in-kind option is unique to physical-asset IRAs and is one reason some retirees value Gold IRAs. The downside: once distributed in-kind, the metal is personal-property bullion subject to non-IRA tax rules — see the article on US gold taxation for the collectibles capital-gains treatment at subsequent sale.

Tax treatment

The RMD amount from a Traditional Gold IRA is taxed as ordinary income at the holder's marginal rate, just as with a cash Traditional IRA RMD. The fair market value of the metal at distribution is the taxable amount; that amount is reported on Form 1099-R by the custodian and flows through to the holder's Form 1040 for the year.

Important: an in-kind distribution does NOT itself trigger a capital gain or loss. The holder receives the metal at its current fair market value, which becomes the holder's new cost basis for any subsequent sale. If the holder later sells the bullion outside the IRA, the difference between the sale price and the in-kind distribution fair market value is the gain or loss for capital-gains tax purposes. Physical-bullion gains are taxed at the collectibles rate (currently capped at `28%` for long-term holdings under IRC § 408(m)(3)) — see our gold-taxation guide for details.

Roth Gold IRA distributions: qualified distributions from a Roth Gold IRA are tax-free under IRS rules. Distributions are qualified if the Roth account has been open at least 5 years and the holder is at least `59½`, has a disability, or qualifies under other IRC § 408A rules. No RMD applies to the original owner's Roth IRA during lifetime.

Penalty for missed RMDs

Failing to take a required RMD triggers an excise tax under IRC § 4974. SECURE 2.0 (effective 2023) reduced the penalty from the historical `50%` of the missed amount to `25%`, with a further reduction to `10%` available if the holder corrects the failure within a specified window ("the correction window") and files a corrected return.

Example: an IRA holder fails to take a `$20,000` RMD by the December 31 deadline. The base excise tax is `25% × $20,000 = $5,000`. If the holder takes the missed distribution and files Form 5329 within the correction window, the tax can be reduced to `10% × $20,000 = $2,000`. The IRS retains discretion to waive the excise tax in cases of "reasonable error and reasonable steps to remedy" — see Form 5329 instructions for the request procedure.

Practical implication: set a December calendar reminder. The math of "forgetting" the RMD is unfavorable and the correction process is paperwork-intensive. The custodian will typically send an RMD reminder; do not rely on it being received.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

When do RMDs start for a Traditional Gold IRA?

Under the SECURE 2.0 Act, RMDs generally begin at age 73 for individuals reaching that age. Roth IRAs (including Roth Gold IRAs) generally have no RMD requirement during the original owner's lifetime. -

Can I take my RMD as physical gold?

Yes — an 'in-kind' distribution ships actual metal to you. The fair market value of the metal counts as the distribution amount for tax purposes. Custodians and depositories charge a secure-shipment fee. -

What if I miss the RMD?

Under SECURE 2.0, the excise tax on a missed RMD is generally 25% (reduced from the older 50%), and can be reduced further to 10% under certain corrective conditions. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.