Gold IRA fees — every line item, plainly

Application, custodian, storage, markup, buyback spread, wire fees. The full Gold IRA fee anatomy with industry-typical ranges and what to ask custodians.

The six fees that actually matter

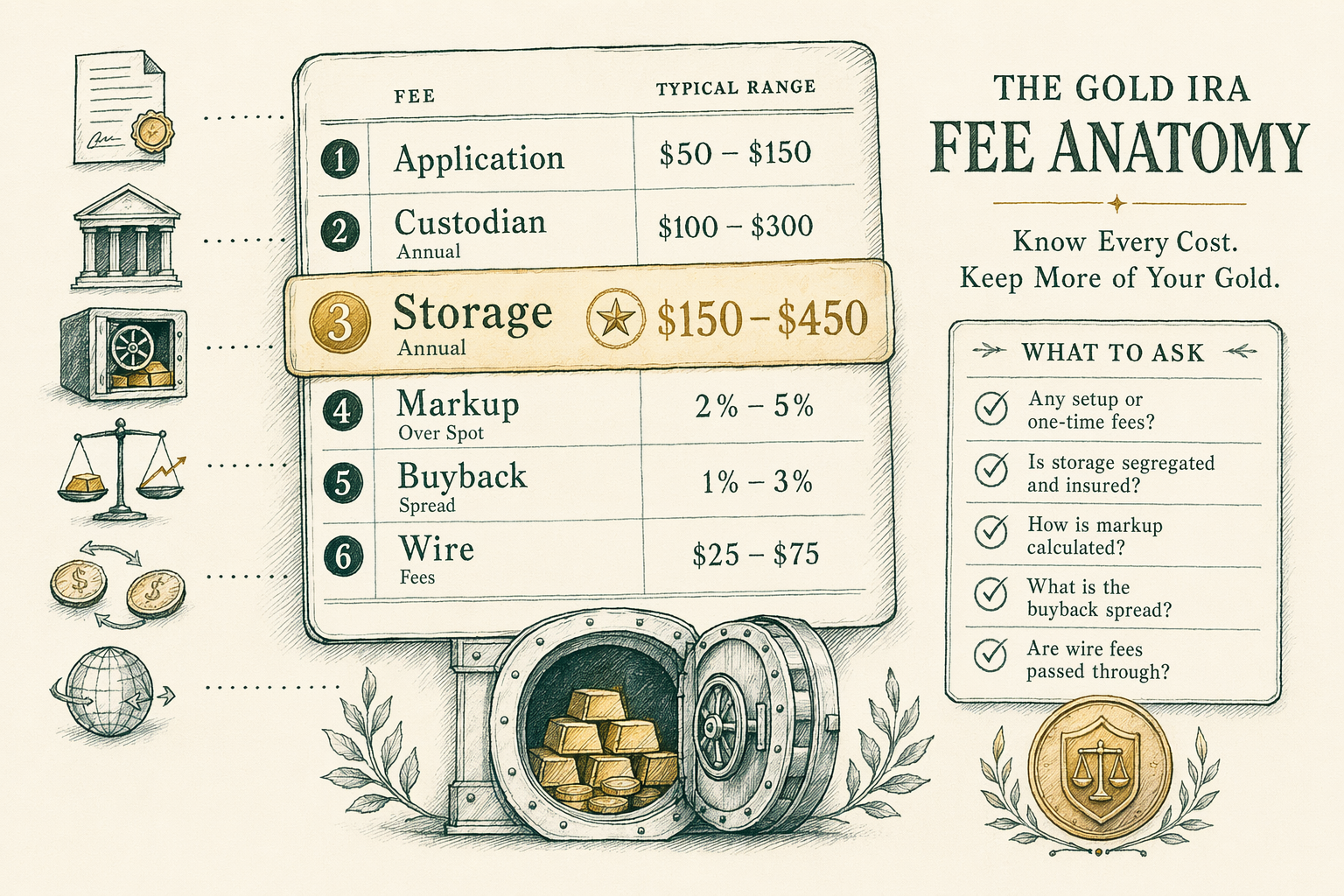

A Gold IRA carries six distinct fee categories. They compound differently, fall on different parties, and almost never appear together on the same marketing page. We list them here in the order they hit the account.

First, the application or account-setup fee. One-time. Industry-typical range $50 to $200. Often waived during a promotion or rolled into the first-year custodian charge. The cheapest fee in the stack and the one Gold IRA marketing materials lead with.

Second, the annual custodian or administration fee. Recurring. Industry-typical range $80 to $200 flat. A minority of custodians use a percentage-of-assets model that runs higher for accounts above roughly $50,000 in assets under custody.

Third, the annual storage fee at the IRS-approved depository. Recurring. Industry-typical range $100 to $300 for segregated allocated storage; $75 to $150 for commingled allocated. Charged by the depository (Delaware Depository, Brink's Global Services, International Depository Services, and a small set of others), not by the IRA marketing company.

Fourth — and this is the line item most accounts are sold to fund — the markup over spot on the initial bullion purchase. One-time at purchase, but on a $100,000 rollover this is by far the largest dollar number in the stack. Industry-typical range is 5% to 15% over the LBMA Gold Price spot reference for Gold IRA marketed coins; specialty proofs and graded numismatic issues run materially higher. Bullion-grade coins at the low end of the range are usually available on request but are rarely volunteered.

Fifth, the buyback spread when you eventually sell metal back to the company that sold it to you. Most reputable Gold IRA companies buy back at or near spot for items they originally sold; a minority quote a discount. This is the exit cost most buyers never model in.

Sixth, wire transfer and transaction fees on the IRA wrapper itself. Recurring per-transaction. Industry-typical range $25 to $40 per outgoing wire from the custodian's banking infrastructure.

We unpack each category in the sections below with the ranges, the verification step, and the question to put to a custodian in writing.

Application and account setup

The application fee covers the custodian's work to open the self-directed IRA shell at an IRS-recognized trust company, run the patriot-act-style identity verification, register the account number, and assign a relationship manager. It is one-time. Industry-typical range is $50 to $200 across the custodians most Gold IRA companies use (Equity Trust, Strata Trust Company, GoldStar Trust, Kingdom Trust, and a small set of others).

A separate transfer-in fee sometimes appears on top — $25 to $50 — covering the custodian's processing of incoming rollover or transfer paperwork from your prior plan administrator. If you are rolling over from a 401(k), that fee may be charged in addition to the application fee on the IRA shell itself.

Setup fees are the most heavily promoted-away component of the stack. A Gold IRA marketing company offering a `$50` setup-fee waiver during a quarterly promotion is reducing the smallest fee in the stack — useful but not load-bearing. The promotion should not change your evaluation of the markup and the storage commitments, which together account for `94%` to `98%` of the all-in first-year cost on a typical six-figure rollover.

The written question to put to a custodian: 'Please send the full fee schedule including application, transfer-in, custodian, storage, and any one-time fees, as it stands at today's date.' If the response is a marketing PDF without dated numbers, ask again specifically for the custodian's current published Fee Disclosure with a dated cover page.

Annual custodian and administration fees

The custodian fee covers the trust company's ongoing administration of the IRA shell: IRS reporting (Form 5498 annual contribution report, Form 1099-R on distributions), required minimum distribution calculations once you reach age 73, account statement production, and the audit trail of every transaction inside the wrapper. It is recurring annually.

Industry-typical range is `$80` to `$200` flat across the major self-directed IRA custodians. Equity Trust Company and Strata Trust Company sit in the middle of that range as of the 2026-Q2 fee schedules; GoldStar Trust and Kingdom Trust tend to sit slightly lower. The flat-rate model is the dominant pricing structure.

A minority of custodians use a percentage-of-assets-under-custody model. These typically charge 0.25% to 0.50% of assets annually. At $50,000 in assets the percentage model is roughly comparable to the flat model. Above $100,000 it becomes materially more expensive: 0.40% on $200,000 in metal is `$800/yr` versus `$150/yr` flat at most flat-rate custodians.

The percentage-fee model is sometimes packaged as 'all-inclusive' — bundling custody and storage into a single percentage. Read the disclosure to confirm whether storage is genuinely included or whether the depository will bill separately on top.

The written question to put to a custodian: 'Is the annual fee flat-rate or percentage-of-assets? If percentage, what is the rate and is storage included or billed separately? If flat-rate, does the rate change with account size, and are there minimum or maximum account thresholds?'

Annual storage fees — allocated vs commingled

Storage fees are paid to the depository, not to the Gold IRA company that sold you the metal. Major IRS-approved depositories for Gold IRA holdings include Delaware Depository Service Company, Brink's Global Services USA, International Depository Services (IDS) of Texas and Delaware, HSBC Bank USA, and JPMorgan Chase Bank. Your custodian's relationship with one or more of these depositories determines which is available on your account.

Allocated storage means specific bars or coins, identified by refiner, serial number, and weight, are registered in your name in the depository's records. There are two further sub-types. Segregated allocated storage means your specific bars sit physically separate from other clients' holdings — their own compartment or vault drawer. Commingled allocated storage means your specific bars are tracked by serial number but physically stored alongside other clients' bars in shared institutional vaulting.

Industry-typical 2026-Q2 ranges: • Segregated allocated: `$100` to `$300/yr` per account, with most depositories using a tiered schedule that climbs with metal weight stored. • Commingled allocated: `$75` to `$150/yr` per account, generally flat-rate or with a lighter weight-tier. • Delaware Depository's published 2026 schedule lists segregated at `$150/yr` for accounts up to `$200,000` in stored value, with commingled at `$100/yr` for the same band. • Brink's pricing for IRA storage sits near the upper end of the segregated range, reflecting the underwriting cost of higher-tier Lloyd's of London coverage.

Both allocated sub-types satisfy IRS Section 408(m) requirements for IRA storage. The distinction is operational and counterparty-related, not regulatory. A more thorough discussion lives at /guides/allocated-vs-unallocated/ and /guides/storage-options/.

The written question to put to a custodian and the depository: 'What is the storage fee schedule for both segregated and commingled allocated storage on this account size? Is the fee weight-tiered or flat? When does the next tier break trigger?'

Markup over spot on the initial purchase

The markup over spot is the dollar gap between the LBMA Gold Price reference and what you actually pay per ounce for the bullion that lands in the depository. It is paid to the Gold IRA marketing company (which sources the metal from a wholesaler or directly from the mint) and is by far the largest single cost in most first-year Gold IRA setups.

Industry-typical 2026-Q2 ranges, drawn from cross-referencing published Gold IRA marketing materials with the parallel retail bullion market at established direct-to-consumer dealers: • Bullion-grade 1 oz American Gold Eagle through Gold IRA channels: 5% to 8% over the LBMA spot fix. • 1 oz proof issues (Proof Gold Eagles, certified Mint State 70 graded): 15% to 30% over spot. • Specialty numismatic and limited-mintage issues sometimes marketed through Gold IRA channels: 30% to 70% over spot, occasionally higher. • Direct-to-consumer retail at established bullion dealers for the same 1 oz Gold Eagle, no IRA wrapper: 3% to 7% over spot.

On a $100,000 rollover deployed into 1 oz American Gold Eagles through a Gold IRA company at the middle of the bullion-grade range (say 7% markup), the markup component is `$7,000`. At the upper bullion-grade range (8%) it is `$8,000`. At the proof-issue range (20%) it would be `$20,000` — one-fifth of the rollover absorbed at purchase. The ratio of markup to all other annual fees combined typically exceeds 20:1 in the first year.

Bullion-grade coins at the low end of the markup range are usually available on request from any reputable Gold IRA company. They are not the default product the marketing rep will lead with, because the rep's commission structure typically scales with markup. Asking for 'IRS-approved bullion-grade coins at the lowest available markup over the LBMA spot fix' is the single highest-leverage sentence in the entire negotiation.

The written question: 'Please quote, in writing, the markup over the current LBMA Gold Price spot fix for (a) IRS-approved bullion-grade 1 oz American Gold Eagles and (b) any proof or specialty issues your firm typically recommends. Please send both quotes alongside the dated LBMA fix used as the reference price.' A company that will not produce both quotes in writing tells you something important.

Buyback spread and exit costs

When you eventually exit the position — through a distribution, a partial sale, or a complete account closure — you sell metal back. Most reputable Gold IRA companies will buy back at or near the prevailing LBMA Gold Price spot fix on bullion-grade coins they originally sold you. A minority quote a discount to spot at sale time. This discount, when present, is called the buyback spread.

A buyback spread of 1% to 3% on bullion-grade product is the rough industry-typical band when it is quoted. On proof and specialty issues, the buyback may be quoted only at spot or slightly under, which means the original markup is not recovered at exit — that markup is an absorbed cost, not a deferred one.

If you take an in-kind distribution (physical possession of the bullion rather than a cash distribution) instead of selling back, the buyback spread does not apply, but you take on the secure-shipment fee from the depository (typically `$50` to `$150`) and the income-tax event on the fair-market value at distribution.

There is no IRS rule requiring the original Gold IRA company to be the buyer. You can have the custodian sell the metal to any reputable bullion dealer at prevailing market quotes. This is a useful negotiation lever if the original company's buyback spread is wide — but the operational simplicity of selling back to the original company, where the metal is already in their familiar depository relationship, is the usual default.

Closing or distribution fees from the custodian itself typically run `$50` to `$150` on top of any wire fees. These are administrative, not market-related.

The written question: 'What is your firm's buyback policy on the specific products you would sell into this account? Please quote the historical buyback spread on those products in writing, and confirm whether the spread applies to bullion-grade and to proof issues differently.'

Wire transfer and transaction fees

The custodian's banking infrastructure carries a per-transaction fee for outgoing wires — typically `$25` to `$40` per wire — covering the routing through the trust company's bank, which is a separate entity from the depository.

Incoming transfers and rollovers usually do not carry a separate wire fee at the custodian level, though some custodians charge a `$25` 'incoming transfer processing' fee on a one-time basis at account open.

Periodic distributions (for example, scheduled required minimum distributions once you reach age 73) carry the same per-wire fee each time. On a quarterly RMD schedule that is `4` wires per year — `$100` to `$160` in annual transaction fees alone, which most fee comparisons miss entirely.

ACH instead of wire is sometimes available and is materially cheaper (often `$0` to `$10` per transaction), but availability depends on the receiving bank and the size of the transaction. Most distributions above `$50,000` will go by wire rather than ACH due to bank-side ACH ceilings.

The written question: 'What is the per-transaction fee for outgoing wires? Is ACH available, and if so, for what transaction sizes? What is the fee for an in-kind distribution that moves physical bullion out of the depository to me?'

How to ask for a written fee schedule

Every reputable Gold IRA company maintains a published, dated Fee Disclosure document and will produce it on request. If the only fee document you receive is a marketing brochure with no date or no specific dollar numbers, ask again specifically: 'Please send the current Fee Disclosure as filed with your custodian, with the cover date and the schedule of dollar amounts for each fee category.'

A complete fee schedule should answer the following ten questions on a single page, with dated dollar figures: 1. What is the application fee? 2. What is the transfer-in fee, if any? 3. What is the annual custodian fee, and is it flat or percentage-based? 4. What is the annual storage fee at each depository on offer, for segregated and commingled allocated? 5. What is the markup over the LBMA Gold Price spot fix for bullion-grade IRS-approved coins? 6. What is the markup for any proof or specialty issues your firm typically recommends? 7. What is the buyback policy and any historical buyback spread on bullion-grade products? 8. What is the closing or distribution fee? 9. What is the per-wire transaction fee? 10. As of what date is this schedule effective, and how often is it updated?

If a company returns answers to all ten in writing with dated dollar figures, you have what you need to compare across companies. If a company will only answer in person on the phone, that itself is a data point — make notes during the call, type them up, and email the notes back to the rep with a request to confirm in writing. A rep willing to confirm specific dollar figures by reply is acceptable; a rep who declines to confirm dollar figures in writing is not.

Once you have written schedules from two or three companies, the side-by-side comparison becomes straightforward arithmetic. The /tools/gold-ira-fee-comparison/ worksheet provides a structured comparison template; the /reviews/gold-ira-companies/ hub carries our editorial reviews of the named companies with snapshot-dated fee data.

How we sourced this

Fee ranges in this guide were compiled from three primary-source bands: (1) the published 2026-Q2 Fee Disclosure documents of major self-directed IRA custodians (Equity Trust Company, Strata Trust Company, GoldStar Trust Company, Kingdom Trust Company), retrieved directly from the custodians' regulatory disclosure pages; (2) the published storage-fee schedules of major IRS-approved depositories (Delaware Depository Service Company, Brink's Global Services USA, International Depository Services), retrieved from each depository's institutional-client disclosure documents; (3) the Internal Revenue Service Publication 590-B (Distributions from Individual Retirement Arrangements), and IRS Publication 590-A (Contributions to Individual Retirement Arrangements), in the 2025 edition.

Markup ranges were triangulated from a sample of Gold IRA marketing materials, BBB-filed dispute records (especially BBB complaint summaries that disclose markup-percentage detail), and the parallel retail markup in the direct-to-consumer bullion market at established dealers. Where a published markup number was not available, the range is conservative — we cite the upper bound of the BBB-filed complaint data and the lower bound of published retail bullion-dealer markups.

Snapshot date for every dollar figure in this guide: 2026-Q2. Fees and arrangements change, sometimes quarterly. Verify with the specific company and custodian before making decisions. The /editorial-standards/ page describes our quarterly review cadence.

Affiliate disclosure

BullionLens earns a commission when readers open Gold IRA accounts through links on our reviews and comparison pages. This does not change the price you pay, the markup you are quoted, or the storage fee you are charged. Editorial selection of which companies we cover is independent — see /editorial-standards/ for the methodology and the criteria we use to add or remove a company from coverage. The reviews carry a 'Last reviewed' date and are revisited quarterly minimum. Commissions are paid only on actions a reader chooses to take after reading the editorial coverage.

In plain English

In plain English: the setup fee is the smallest fee. The markup over spot on the initial bullion purchase is the biggest by 20:1 — on a `$100,000` rollover, you are probably paying `$5,000` to `$15,000` in markup the day the metal lands in the vault. Ask three companies for their written fee schedule with all ten line items including specific dollar markup. Ask specifically for bullion-grade coins at the lowest markup. Compare side-by-side. Then call a CPA before signing anything, because this is a tax-deferred account with rules the marketing page does not cover.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is the typical Gold IRA setup fee?

Industry-typical $50-$200 one-time, often waived during a promotion. Some custodians charge a separate transfer-in fee on top. -

What is the typical annual custodian fee?

Most custodians charge $80-$200 annually, flat-rate. A few use a percentage-of-assets model (rarely cheaper for accounts above $50,000). -

What is the typical annual storage fee?

Segregated allocated storage at IRS-approved depositories runs $100-$300 annually. Commingled allocated is $75-$150. Pricing varies by depository and metal weight. -

Is the markup over spot a 'fee'?

Yes, in economic terms — it is the largest single cost in most first-year Gold IRA setups. Markups of 5-15% over spot are common for Gold IRA marketed coins (proofs and specialty issues run higher). Bullion-grade coins at lower markup are usually available on request. -

What happens to fees if I close the account?

Custodians typically charge a closing/distribution fee ($50-$150). Storage is prorated to the closure date. If you take physical possession (rather than cash distribution), you pay the depository's secure-shipment fee.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.