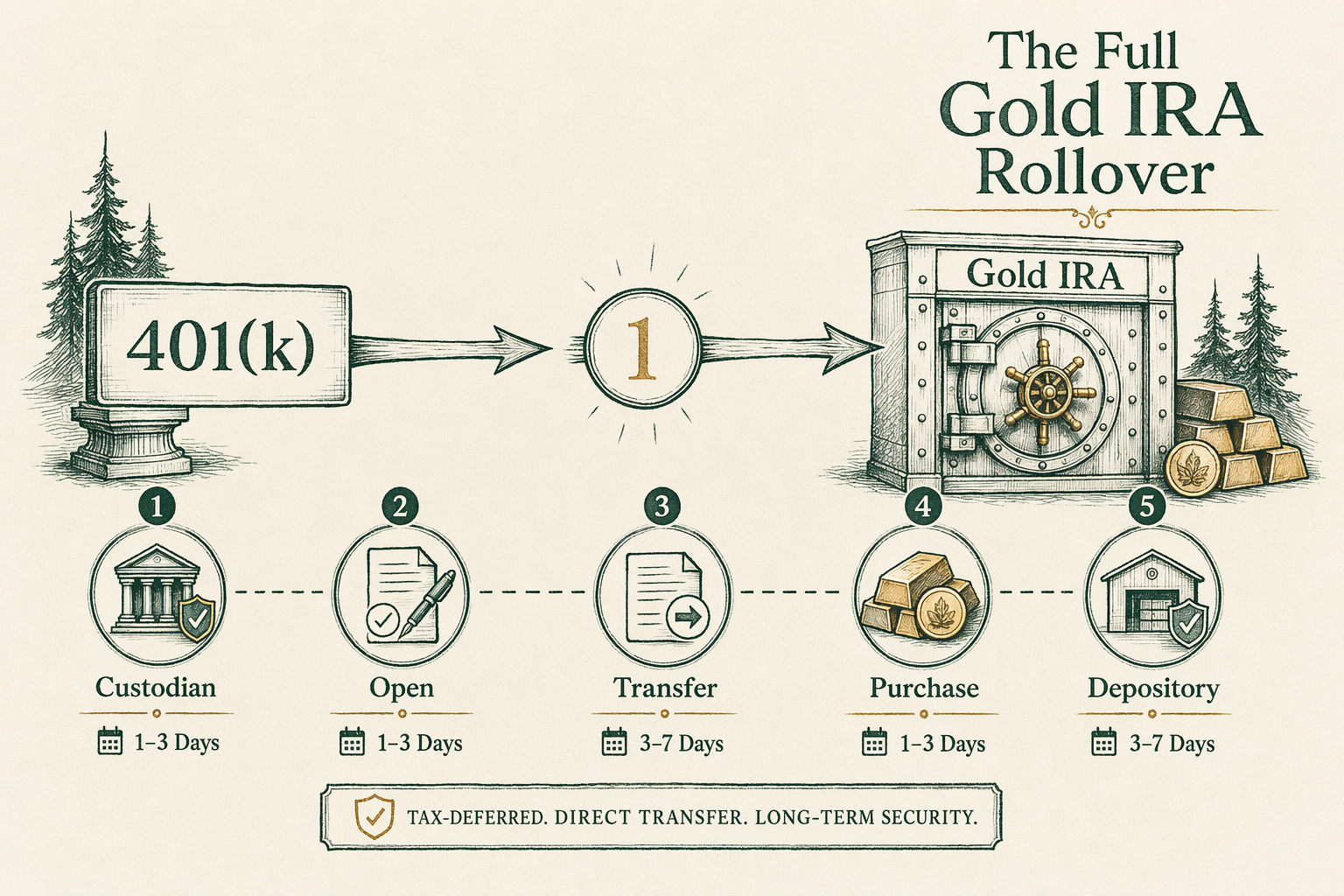

How a Gold IRA rollover works — step by step

The full Gold IRA rollover sequence: custodian selection, account opening, transfer request, metal purchase, depository delivery. Forms and timing at each step.

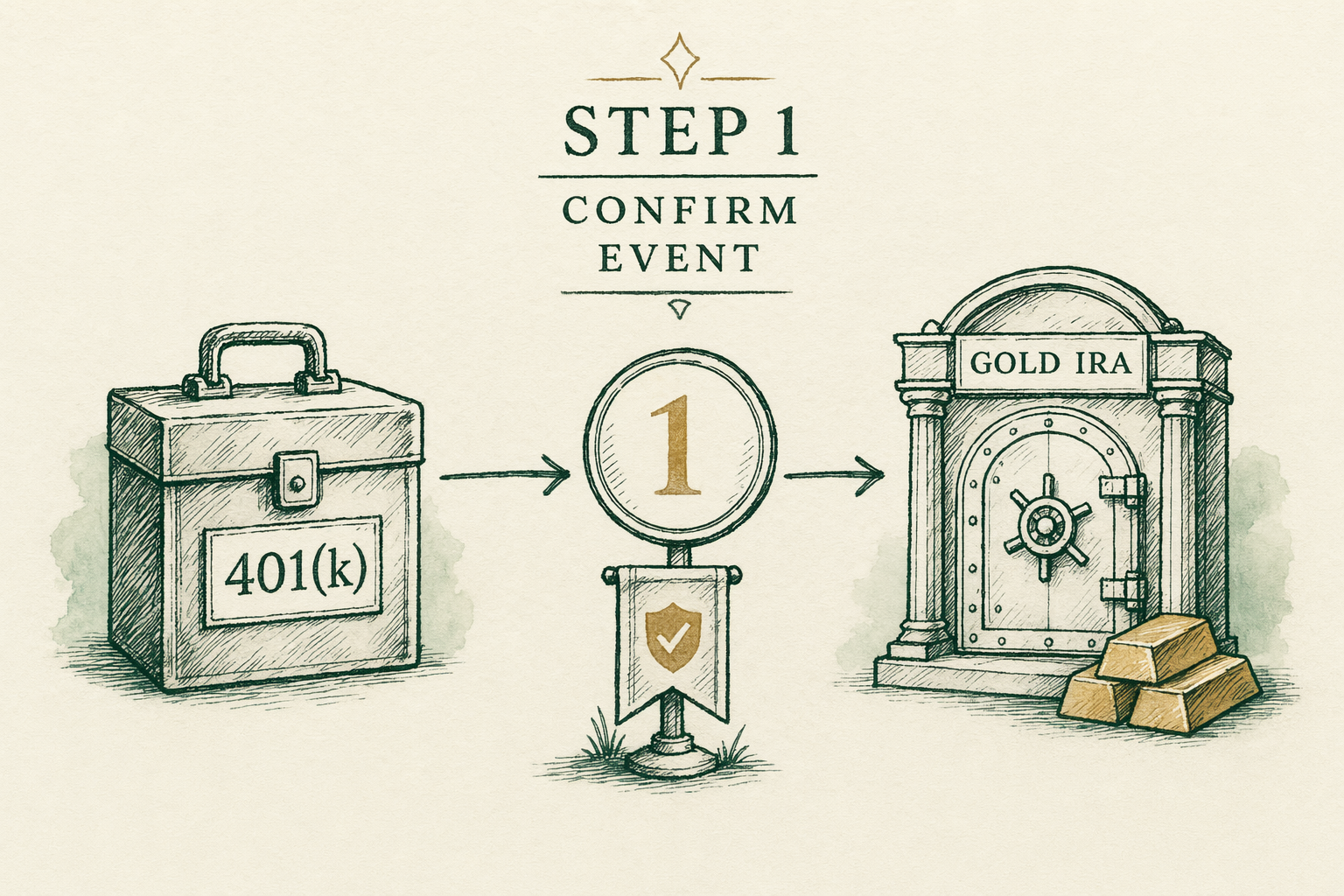

Step 1 — Confirm distributable event

Before any rollover can begin, the distributing account must be eligible to release funds. For a Traditional or Roth IRA, this is automatic — IRA-to-IRA transfers between custodians don't require a triggering event beyond your instruction. For a `401(k)`, `403(b)`, or other employer-sponsored retirement plan, you need a 'distributable event': typically separation from the employer, reaching age `59½`, the plan's normal retirement age, or specific in-service withdrawal provisions written into the plan document.

Verify with the distributing plan administrator before instructing the new custodian to issue transfer paperwork. The Summary Plan Description (SPD) is the authoritative source. Call the plan administrator (Fidelity, Vanguard, Empower, etc.) and ask specifically: 'Am I eligible to roll over to an IRA, what conditions must be met, and what is the plan's preferred process for direct trustee-to-trustee rollover?' Some plans require their proprietary distribution request form; others accept a generic letter from the receiving custodian. Knowing the answer upfront saves weeks of back-and-forth.

Step 2 — Select custodian and open the SDIRA

A self-directed IRA (SDIRA) must be opened with an IRS-recognized custodian that supports alternative assets including physical precious metals. The dominant custodians in this niche are Equity Trust Company (South Dakota), STRATA Trust Company (Texas), Kingdom Trust, IRA Financial, and a handful of others. Each has its own fee schedule, depository options, and operational style. The custodian is the IRS-recognized fiduciary holding the account — it is not the Gold IRA marketing company (Augusta, Birch, Goldco). The marketing company helps you select metals and depository, but the custodian holds the account.

Opening the SDIRA typically involves a packet of forms: account application, IRS Form `W-9`, signature pages, beneficiary designations, and a depository selection. Most custodians can process the application within `2-5` business days once the packet is complete. Some Gold IRA marketing companies (Augusta, Birch, Goldco) coordinate the custodian onboarding for you — they help fill out the paperwork, but the contractual relationship is between you and the custodian, not between you and the marketing company. Confirm in writing which entity has custody of the account.

Step 3 — Initiate transfer from existing plan

Once the SDIRA is open, the new custodian generates a Transfer Request Form (or 'rollover request' for `401(k)` situations) listing the distributing account number, plan name, and the requested transfer amount. This form goes to the existing plan administrator, who processes the request and issues the funds. For IRA-to-IRA transfers, the funds typically move via ACH or wire from the old custodian directly to the new custodian, never touching your personal bank account. This is the cleanest path because trustee-to-trustee transfers are not reportable distributions under IRS rules.

For `401(k)` rollovers, the process is similar but often slower. The distributing plan typically sends funds via check made payable to '`<New Custodian>` FBO `<your name>`, IRA Account `<account#>`' — which the receiving custodian deposits to your IRA. This 'FBO' check is a direct rollover and remains non-taxable. Avoid the option where the plan makes the check payable directly to you personally; that triggers mandatory `20%` federal withholding, the `60`-day deposit rule, and a one-rollover-per-12-months counter. Direct trustee-to-trustee is cleaner, faster, and reduces the chances of accidentally creating a taxable distribution.

Step 4 — Fund settlement and metal purchase

When the transferred funds settle at the new custodian, they sit in a cash position inside the SDIRA. The custodian doesn't actively invest these funds — you (or the Gold IRA marketing company acting on your written direction) initiate the metal purchase. You select the specific bullion products from the dealer's IRA-eligible inventory (`1 oz` Gold Eagles, `1 oz` Maple Leafs, `1 oz` Gold Buffalos, IRS-approved silver, platinum, or palladium per the custodian's list), agree on price (including dealer markup), and authorize the purchase in writing.

The custodian wires the agreed purchase amount to the bullion dealer. The dealer arranges shipment of the physical metal directly to your IRS-approved depository — never to you personally. Direct-to-depository shipment is what preserves IRA tax treatment; metal that touches your personal possession en route can trigger IRS treatment of the entire transaction as a distribution. The dealer's shipment includes a serial-numbered manifest matching each bar or coin to your custodian's records. The depository acknowledges receipt to the custodian, who updates your account statement showing the new positions.

Step 5 — Depository delivery and confirmation

Once the depository (Delaware Depository Service Company, Brink's Global Services, International Depository Services of Texas/Delaware, or another IRS-approved facility) receives the shipment, the receiving clerk inventories each bar and coin against the dealer's manifest. Bars are confirmed by serial number, weight, and refiner stamp; coins are counted by quantity and type. The depository issues a Certificate of Receipt (or equivalent confirmation document) to the custodian, listing the specific items now held under the depository's bailment for your IRA account.

Request a copy of the Certificate of Receipt or holdings statement for your records. Many depositories issue monthly account statements listing bar serial numbers and total holdings; some make this available via online portal. Confirm the storage type — segregated (your specific bars stored in their own compartment) versus commingled-allocated (your specific bars tracked individually but stored together with other clients' bars). Segregated typically costs more annually but provides clearer ownership documentation. Once delivery and confirmation are complete, the rollover is operationally finished. Total elapsed time from Step `1` to Step `5` is typically `3-6 weeks` for a `401(k)` rollover, faster for IRA-to-IRA transfers.

Step 6 — Annual reporting

After the rollover completes, two IRS forms reconcile the transaction. The distributing plan issues Form `1099-R` reporting the gross distribution with distribution code `G` (direct rollover, non-taxable). The receiving custodian issues Form `5498` reporting the rollover contribution. Both forms appear on your tax return; the `1099-R` is reported on the IRA distribution line and netted against the rollover code to show zero taxable amount. If you used an indirect (`60`-day) rollover instead of trustee-to-trustee, the reporting is more complex and the risk of accidental taxable treatment is higher.

Annually thereafter, the custodian issues Form `5498` if you make new contributions and a Form `1099-R` only when distributions are taken. The depository continues to bill annual storage fees (typically `$100-$300/yr` depending on storage type and metal weight); the custodian bills annual maintenance fees (typically `$80-$200/yr`). Required Minimum Distributions (RMDs) begin at age `73` under current rules; Gold IRA RMDs can be satisfied in cash (after a partial liquidation of metals) or in-kind (taking physical possession of bars/coins, which then becomes a taxable distribution event). Plan the RMD strategy with a CPA who knows your situation.

Real-world example — a $150,000 IRA rollover timeline

Consider a `62-year-old` with a `$150,000` Traditional IRA at Fidelity, rolling over to a Gold IRA via Augusta Precious Metals with Equity Trust as custodian and Delaware Depository as storage. Week `1`: initial conversation with Augusta, paperwork sent for Equity Trust SDIRA. Week `2`: SDIRA opens, Equity Trust generates IRA-to-IRA transfer request, sent to Fidelity. Week `3`: Fidelity processes transfer, wires `$150,000` to Equity Trust. Week `3.5`: Funds settle at Equity Trust SDIRA. Week `4`: Augusta proposes specific bullion (e.g., `60 × 1 oz American Gold Eagle` at illustrative spot + 5% markup), client authorizes purchase. Week `4.5`: dealer ships to Delaware Depository.

Week `5`: Delaware Depository receives shipment, inventories, issues Certificate of Receipt to Equity Trust. Equity Trust updates account statement showing `60` Eagles held. Week `5-6`: client receives confirmation and first monthly statement. Total elapsed time: roughly `5-6 weeks` from initial conversation to confirmed positions. Tax forms (`1099-R` from Fidelity, `5498` from Equity Trust) arrive the following January. Year `2` recurring costs: `$80` Equity Trust + `$150` segregated storage = `$230/yr`. No new markup unless additional bullion is added.

Common misconceptions about the rollover process

**'I can take the cash and deposit it myself within 60 days.'** Technically yes via indirect rollover, but the distributing plan applies mandatory `20%` federal withholding, you have only `60` days to deposit, and you're limited to one such rollover per `12` months across all IRAs. Direct trustee-to-trustee transfer avoids all three constraints.

**'The whole process takes one afternoon.'** No. End-to-end timing is typically `3-6 weeks` for a `401(k)` rollover, `1-3 weeks` for an IRA-to-IRA transfer. Delays usually originate at the distributing plan administrator.

**'My personal bank account is involved.'** No, and it shouldn't be. Funds move from the old plan trustee directly to the new IRA custodian. Metal ships from the dealer directly to the depository. Any path where you personally handle funds or metal during the rollover risks triggering IRS distribution treatment.

What this means for you

A Gold IRA rollover is a `3-6 week` administrative process with well-defined steps. The keys to a clean rollover: confirm a distributable event before starting, use direct trustee-to-trustee transfers (never indirect `60`-day rollovers when avoidable), keep all metal flowing directly from dealer to depository, and confirm receipt documentation matches the dealer manifest. Choose a custodian carefully — it's the entity holding the account long-term. Choose a depository carefully — segregated versus commingled-allocated has documentation implications. As always, BullionLens does not provide personalized advice on whether or how to execute a rollover; consult a licensed adviser and a CPA who know your specific tax and retirement situation.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

How long does a Gold IRA rollover take?

Typical end-to-end timing is 2-6 weeks. Custodian-to-custodian transfers are faster (1-3 weeks) than 401(k) rollovers (3-6 weeks). Delays usually originate at the distributing plan administrator. -

What forms does the receiving custodian send?

Account application, transfer request form (referencing your existing custodian/plan), depository selection form, IRS Form W-9, and a metal purchase authorization. Some custodians consolidate these into a single packet. -

Who actually ships the metal?

The dealer fulfilling the purchase ships directly to your IRS-approved depository — never to you personally. Direct-to-depository delivery preserves the IRA tax treatment. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.