Gold IRA vs physical gold — which makes sense?

Comparing a Gold IRA to direct physical gold ownership: tax treatment, custody costs, access, and the situations in which each makes sense.

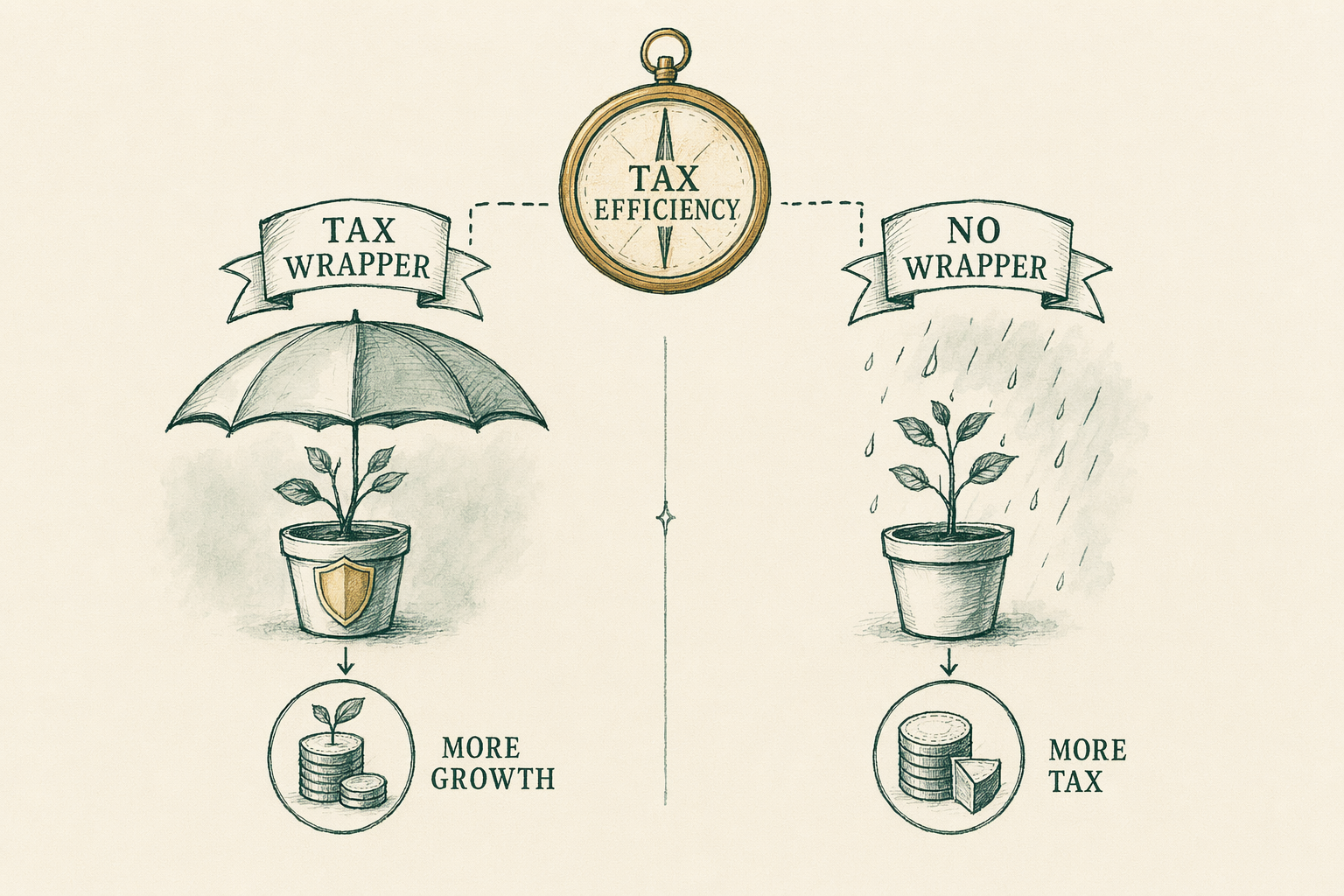

Tax wrapper vs no wrapper

**Gold IRA (Traditional)**: Pre-tax contributions or pre-tax 401(k) rollover. Growth is tax-deferred. Distributions taxed as ordinary income at the holder's marginal rate. Subject to RMDs starting at the SECURE 2.0 applicable age (`73`, moving to `75`). Early distributions before `59½` are subject to a `10%` penalty under IRC § 72(t).

**Gold IRA (Roth)**: After-tax contributions. Growth is tax-free. Qualified distributions tax-free. No RMD during the original owner's lifetime. Direct contributions subject to income limits.

**Direct physical gold (no IRA)**: Bought with after-tax dollars. No annual reporting on the holding itself. On sale, gains are taxed at the collectibles capital-gains rate under IRC § 408(m)(3) — currently capped at `28%` for long-term holdings (held >1 year), with short-term gains taxed at ordinary income rates.

**The tax-wrapper math**: A `28%` collectibles cap on non-IRA gold is meaningful. For a holder in the `32%-37%` federal bracket, the `28%` collectibles cap is actually LOWER than the marginal ordinary income rate that a Traditional IRA distribution would attract. The Traditional IRA's nominal tax deferral does not translate into a lower lifetime tax rate for high-bracket holders — it can translate into a higher one.

Custody cost comparison

**Gold IRA custody**: IRS rules require an IRS-approved depository under IRC § 408(n) — Delaware Depository, Brink's Global Services, IDS of Texas, or another approved facility. Annual storage runs `$100-$300/yr` for segregated, `$50-$150/yr` for commingled, depending on depository and value. Custodian fees (Equity Trust, STRATA) add `$80-$200/yr` for account administration.

**Direct physical custody options**: (1) Home safe — `$200-$2,000` one-time, no recurring fee, but home-insurance riders typically have a `$5,000-$10,000` bullion limit; (2) Safe deposit box at a bank — `$50-$200/yr`, no FDIC coverage on contents; (3) Private vault storage (Brink's, BullionVault, Loomis) — `$0.50-$1.20 per $1,000 of value per year`; (4) Allocated storage at a bullion dealer (Money Metals Depository, others) — comparable to private vault rates.

**Apples-to-apples**: For `$100,000` of gold over `10` years, Gold IRA custody is approximately `$2,500-$5,000` total. Direct physical at allocated private-vault storage is approximately `$1,000-$1,500` total. Direct physical at home with insurance is approximately `$400-$1,000` total (insurance rider). The Gold IRA's custody cost is meaningfully higher than direct alternatives — which is part of the cost of the tax wrapper.

Access and liquidity

**Gold IRA access**: To use the metal, you must take a distribution from the IRA. Cash distribution: sell metal at the depository, receive cash. In-kind distribution: receive physical bullion. Either path triggers ordinary-income taxation (Traditional) on the distributed amount. Distributions before `59½` add the `10%` early-withdrawal penalty. The IRA wrapper structurally constrains access.

**Direct physical access**: Immediate. The metal is in your safe, your bank's safe deposit box, or your vault account where you have direct title. You can sell to a local coin shop, ship to an online dealer for buyback, or hold indefinitely with no forced distribution. The flexibility is the practical advantage of direct ownership.

**Liquidity considerations**: Selling Gold IRA bullion at the depository is a multi-day process (custodian instruction, depository sale, cash proceeds). Selling direct physical bullion at a local coin shop can be same-day cash; selling to an online dealer is `1-2` weeks. Storage-program clients at private vaults can sell on the platform with same-day settlement. The Gold IRA is the least liquid of these options.

Estate planning considerations

**Gold IRA inheritance**: Traditional Gold IRA passes to the named beneficiary under the IRA beneficiary designation, bypassing probate. The SECURE Act (2019) requires most non-spouse beneficiaries to distribute the inherited IRA within `10` years; distributions remain ordinary-income-taxable to the beneficiary. Roth Gold IRAs pass similarly, with the `10-year` rule applying but distributions remaining tax-free (the beneficiary loses the tax-free compounding but not the tax-free distributions).

**Direct physical inheritance**: Goes through the estate per the will or applicable state law. Subject to estate tax above the federal estate-tax exemption. Receives a step-up in basis at the holder's death under current rules — the heir's cost basis is the fair market value at the date of death, eliminating any built-up unrealized gain for capital-gains tax purposes at subsequent sale.

**The estate-planning trade-off**: Direct physical receives a step-up in basis at death; Traditional IRA does not (the IRA's ordinary-income tax burden passes to the heir). For high-net-worth holders with substantial built-up gains, the step-up on direct physical can be more tax-efficient at inheritance than the Traditional IRA's deferred-ordinary-income structure. Consult an estate-planning attorney for specific scenarios.

When to use each (or both)

**Use a Traditional Gold IRA when**: You have an existing pre-tax 401(k) or Traditional IRA you want to allocate to gold and rolling it over to a Gold IRA preserves the tax deferral; your expected retirement tax bracket is meaningfully lower than your current bracket; you want the discipline of forced retirement-account separation.

**Use a Roth Gold IRA when**: You expect a higher retirement tax bracket than today; you want no lifetime RMDs; you want to leave the wrapper to heirs with favorable tax characteristics; your MAGI permits direct Roth contributions (or you can execute a backdoor conversion).

**Use direct physical gold when**: You are using after-tax dollars; your time horizon is less than `10` years; you want immediate physical access; you want the step-up in basis at death; you prefer the lower custody-cost structure.

**Use both when**: You have substantial gold allocation and the wrappers serve different purposes. Many holders run a `5-15%` allocation split across both — IRA-wrapped for the retirement-asset portion, direct physical for the access-and-flexibility portion. This split also diversifies operational/custody risk across two distinct custody arrangements.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Why pay Gold IRA fees if I can just buy physical gold?

Gold IRA fees buy you tax-deferred or tax-free (Roth) treatment on gains. If your gold position will sit untouched for 10-20+ years and you're using retirement-account funds, the wrapper can be worth it. For after-tax dollars and short holding periods, direct physical often beats IRA-wrapped after fees. -

Can I hold both?

Yes — and many bullion buyers do. After-tax physical gold provides direct access and bequest flexibility; IRA-wrapped gold gets tax treatment on the growth. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority. -

When was this page last reviewed?

See the 'Last reviewed' date at the bottom of the page. We commit to a quarterly minimum review cycle; fee schedules, IRS rules, and company arrangements can change between reviews — confirm with primary sources before transacting.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.