Roth vs Traditional Gold IRA

Tax treatment, contribution rules, distribution mechanics, RMD differences, and the situations in which each Gold IRA wrapper makes sense.

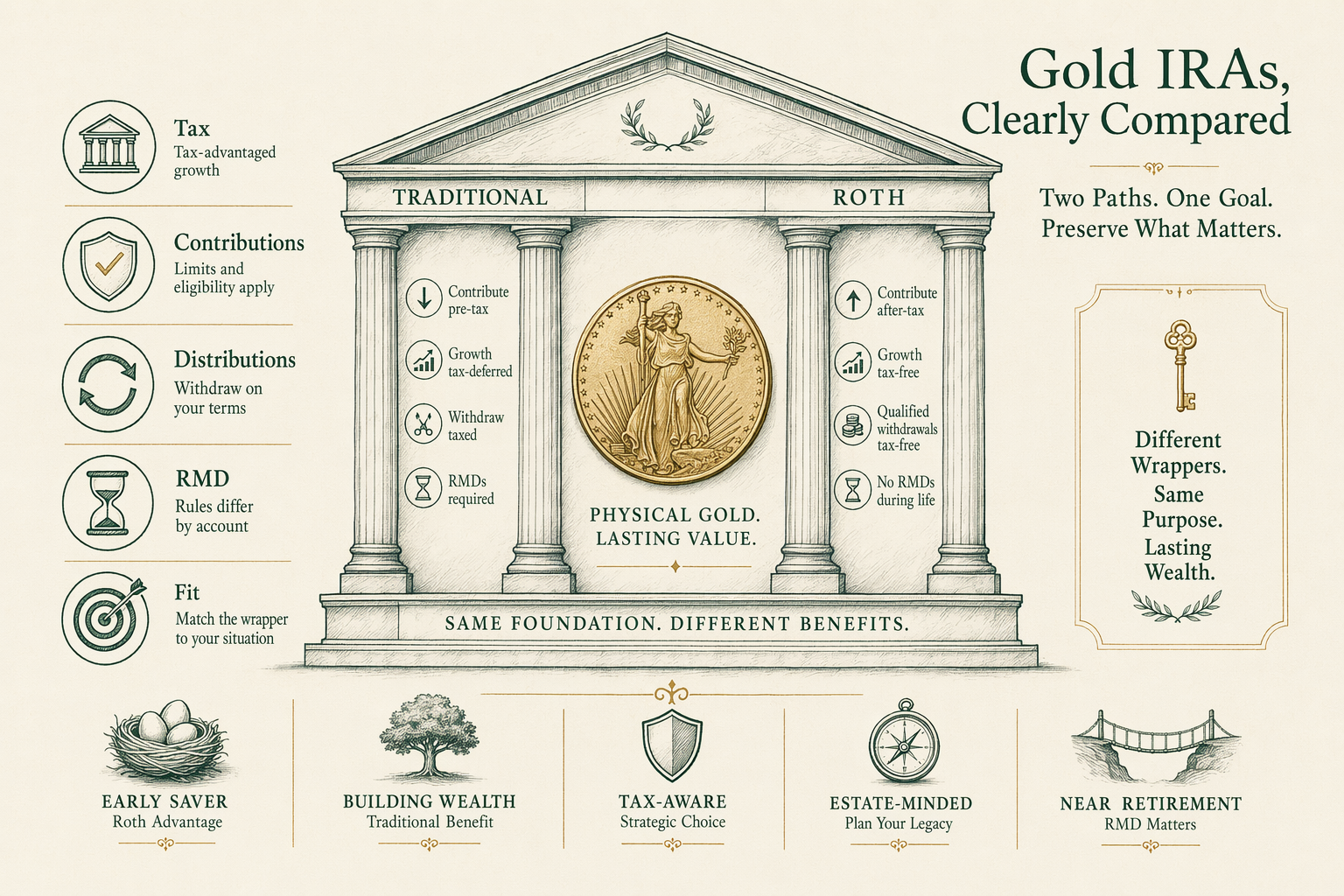

Contribution tax treatment

**Traditional Gold IRA**: Contributions may be tax-deductible in the year made, subject to income limits and active-participant rules under IRC § 219 and IRC § 408. For high-income earners with workplace retirement plan coverage, the deduction may phase out. The deductibility is the up-front tax benefit of a Traditional IRA — money goes in pre-tax (or with a tax deduction recovering the pre-tax effect), grows tax-deferred, and is taxed on the way out.

**Roth Gold IRA**: Contributions are NEVER tax-deductible. Money goes in after-tax — the IRA holder has already paid income tax on the contribution amount. The trade-off is that qualified distributions later are tax-free.

**Rollover contribution to either wrapper**: A 401(k)-to-Traditional-IRA rollover is tax-neutral if executed as a direct trustee-to-trustee transfer. A 401(k)-to-Roth-IRA rollover (a Roth conversion) is a taxable event — the rolled-over amount counts as ordinary income in the conversion year.

Snapshot as of `2026-Q2`. Contribution limits and income phase-out ranges adjust annually; verify against current IRS figures before any contribution.

Distribution tax treatment

**Traditional Gold IRA distributions**: Taxed as ordinary income at the holder's marginal rate in the year of distribution. The entire distribution — the original contribution amount plus all accumulated appreciation — is ordinary income, regardless of whether the appreciation is short-term or long-term in nature. There is no capital-gains tax treatment within a Traditional IRA. Distributions before age `59½` are also subject to a `10%` early-withdrawal penalty under IRC § 72(t) unless an exception applies.

**Roth Gold IRA qualified distributions**: Tax-free under IRS rules. A distribution is qualified if (1) the Roth account has been open at least 5 tax years AND (2) the holder is at least `59½`, has a disability, or qualifies under another IRC § 408A exception. Both conditions must be satisfied.

**Roth Gold IRA non-qualified distributions**: The contribution portion is always tax-free (the holder already paid tax on those amounts). The earnings portion is taxed as ordinary income and may also be subject to the `10%` early-withdrawal penalty under IRC § 72(t). The IRS ordering rules in IRC § 408A determine which portion of a non-qualified distribution is contribution vs earnings.

RMD rules

**Traditional Gold IRA RMDs**: Required Minimum Distributions begin at the SECURE 2.0 applicable age (currently `73` for most, moving to `75`). The annual RMD is calculated as the prior-year December 31 fair market value divided by the IRS Uniform Lifetime Table divisor. RMDs are taxable as ordinary income; failure to take an RMD triggers a `25%` excise tax under IRC § 4974 (reducible to `10%` for timely-corrected failures).

**Roth Gold IRA RMDs**: Generally NO RMD requirement during the original owner's lifetime. This is a structural advantage of Roth IRAs — the account can compound tax-free as long as the original owner is alive, with no forced distribution.

**Inherited IRAs**: Both Traditional and Roth inherited IRAs are subject to RMD rules under the SECURE Act (2019) — most non-spouse beneficiaries must distribute the full inherited IRA within 10 years. The RMD profile for inherited accounts is therefore similar across both wrappers, even though the Roth side carries no RMD during the original owner's life.

Income limits for Roth contributions

Roth IRA contributions are subject to income limits under IRC § 408A. The contribution limit phases out for higher-income earners. For `2026-Q2`-relevant calendar years, the phase-out range for single filers is approximately `$146,000-$161,000` modified adjusted gross income (MAGI), and for married filing jointly approximately `$230,000-$240,000`. Above the top of the range, direct Roth contributions are not permitted.

Traditional IRA contributions are subject to a separate (and different) set of income rules. The contribution itself is permitted regardless of income, but the deductibility phases out for high-income earners who are active participants in a workplace retirement plan.

**Backdoor Roth**: A high-income earner who cannot directly contribute to a Roth can contribute to a non-deductible Traditional IRA and then convert that amount to a Roth (a "backdoor Roth"). The conversion is taxable but on a much smaller amount than a full rollover. The strategy has IRS-blessed mechanics under current law but is contested in some commentary; consult a tax adviser before relying on it.

Verify current MAGI phase-out figures against IRS guidance — they adjust annually with inflation.

Conversion mechanics

A Roth conversion moves all or part of a Traditional IRA (including a Traditional Gold IRA) into a Roth IRA. The amount converted is taxed as ordinary income in the conversion year. There is no income limit on the conversion itself — even high-income earners can convert, as long as they pay the tax due.

**For a Gold IRA specifically**, the conversion can be executed as an in-kind transfer — the metal stays at the depository, the IRA wrapper changes from Traditional to Roth, and the fair market value at the conversion date determines the taxable amount. Custodians (Equity Trust, STRATA) handle the wrapper-change paperwork; the depository's custody of the metal is unaffected.

**Strategic context**: Roth conversions are most attractive when the holder expects higher tax rates in retirement than today, or has years with unusually low marginal rates (e.g., between retirement and the start of Social Security). They are least attractive when current marginal rates are at peak career levels.

**Pacing**: Many holders execute partial Roth conversions over multiple years to manage the tax bracket impact. A `$500,000` Traditional IRA converted in one year would land in the top federal bracket; the same amount converted over `10` years can be paced to fill lower brackets each year.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Which is better, Roth or Traditional Gold IRA?

Neither is universally better. Traditional makes sense if your current tax rate exceeds your expected retirement tax rate. Roth makes sense if you expect a higher tax rate in retirement, want no RMDs, or want to leave the account to heirs with favorable tax treatment. -

Can I convert a Traditional Gold IRA to Roth?

Yes — a Roth conversion is permitted at any time, with the converted amount taxed as ordinary income in the year of conversion. Conversion strategies are common but complex; consult a tax adviser. -

Do Roth Gold IRAs have income limits?

Contributions to Roth IRAs (including Roth Gold IRAs) have income limits under IRS rules. Conversions from Traditional to Roth do not have income limits, though the conversion is itself taxable. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.