What is IRS Form 1099-B for gold sales?

When a dealer files a 1099-B on a customer's gold sale: thresholds by coin and bar, which products trigger reporting, and which do not.

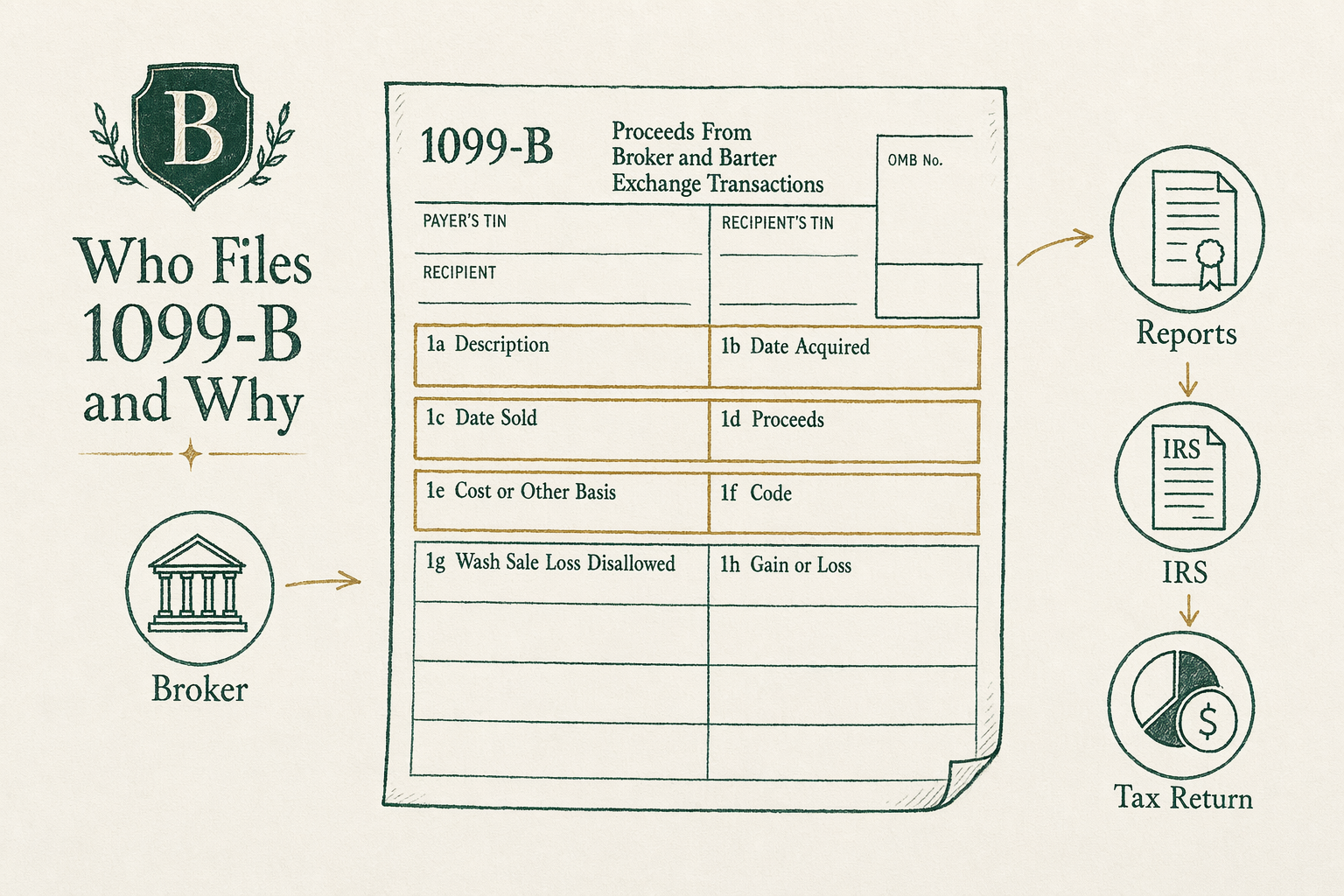

Who files 1099-B and why

IRS Form `1099-B`, 'Proceeds From Broker and Barter Exchange Transactions,' is filed by brokers and dealers on certain customer transactions. For precious-metals dealers, the obligation is triggered when a customer sells specific products at or above specific thresholds. The dealer files the `1099-B` with the IRS and sends a copy to the customer; the customer incorporates the form's information into their personal tax return (Form `8949` and Schedule D).

The purpose of the form is third-party reporting — the IRS receives an independent record of qualifying transactions, which the agency uses to cross-check taxpayer self-reporting on Schedule D. The form does not change the taxpayer's underlying tax obligation. A taxable gain remains taxable whether or not a `1099-B` is filed; the only difference is whether the IRS independently knows about the transaction. From the dealer's perspective, filing the form when required is a regulatory obligation under IRS broker-reporting rules dating to the `1980s` and updated periodically.

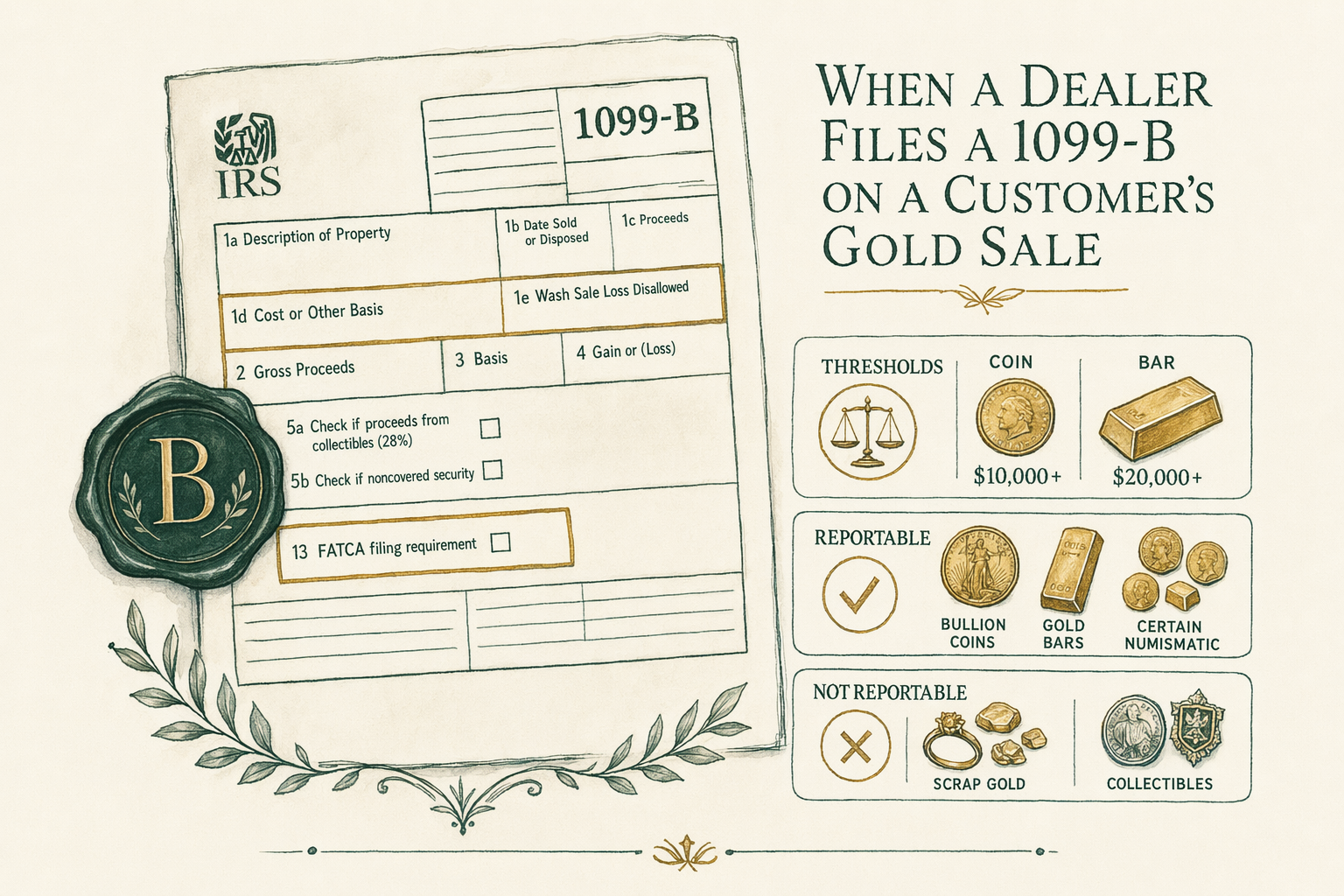

Reportable products and thresholds

IRS rules specify product types and quantity thresholds for `1099-B` reporting on customer sales to dealers. For gold, key reportable thresholds include: sales (by customer to dealer) of `25 oz or more` `1 oz` South African Krugerrands; sales of `25 oz or more` `1 oz` Canadian Gold Maple Leafs; sales of `25 oz or more` `1 oz` Mexican Onza coins; sales of `100 oz or more` gold bars of `0.995` or higher fineness; sales of `1 kilo or more` gold bars of similar fineness. These thresholds reflect the volumes at which an individual transaction is consistent with investment-grade scale rather than incidental collectible sale.

Silver reporting triggers include sales of `1,000 troy oz or more` of `0.999`-fineness silver bars and certain quantity thresholds on `90%`-silver pre-`1965` US coins. Platinum and palladium have their own thresholds at institutional-scale volumes rarely reached by retail customers. The thresholds apply per-transaction, per-product — selling `20` Krugerrands does not trigger reporting; selling `25` does. Sequential structured sales designed to avoid the threshold may be aggregated under IRS anti-structuring guidance; dealers exercise judgment on borderline patterns.

Products that do NOT trigger reporting

The most notable exclusion from `1099-B` reporting is the American Gold Eagle. The Eagle is specifically excluded from IRS broker-reporting requirements regardless of quantity sold. The American Silver Eagle is similarly excluded for the silver-bullion side. The American Gold Buffalo and various other sovereign-mint coins not specifically listed in IRS broker-reporting regulations also do not trigger reporting at the dealer-purchase scale that catches Krugerrands and Maples.

The exclusion of American Eagles is structural — Congress and Treasury have positioned the US Mint's flagship bullion products as preferred holdings, including via the `1099-B` reporting carve-out. From a seller's tax-administration perspective, this means a sale of any quantity of American Gold Eagles to a dealer does not generate a `1099-B`; the IRS receives no independent third-party report of the transaction. This does NOT change the seller's tax obligation. The gain is still taxable; the seller still self-reports on Schedule D. The carve-out affects only third-party reporting, not the underlying tax treatment of the gain.

What happens after a dealer files

When a dealer files a `1099-B` on a customer sale, the form goes to two places. Copy A goes to the IRS as part of the dealer's annual `1099` filing (typically due by the end of February for the prior calendar year). Copy B goes to the customer by the end of January of the following year. The form reports the gross proceeds (sale price), date of sale, product description, and customer identifying information. The form generally does not report the customer's basis (since the dealer doesn't know what the customer paid originally).

The customer uses the `1099-B` information to complete Form `8949` (sales and other dispositions of capital assets) on their personal tax return. Customer enters acquisition date and basis from their own records, the proceeds from the `1099-B`, calculates gain or loss, and the result flows to Schedule D. For collectibles like physical gold, the gain is categorized for the `28%` maximum long-term collectibles rate under Section `1(h)(5)`. Discrepancies between what the dealer reports on `1099-B` and what the customer reports on Schedule D can trigger IRS inquiries; reconcile them before filing.

Buyer vs seller — who triggers what

The `1099-B` is triggered by the customer selling to the dealer, not the customer buying from the dealer. The reporting obligation flows from the dealer's purchase of metal from the public — the dealer is the buyer in that transaction and is treated as a broker for IRS reporting purposes. When the customer is the buyer (purchasing metal from the dealer), there is no `1099-B`; the customer simply has a new asset with a basis equal to what they paid.

Form `8300` is a different reporting requirement, triggered by the dealer receiving more than `$10,000` in cash (or cash-like instruments) from a customer in a single transaction or related transactions summing to that amount. Form `8300` is filed on the dealer's customer-buy side, in contrast to the `1099-B` which fires on the dealer's customer-sell-back side. The two forms serve different purposes — `1099-B` for income reporting, `8300` for anti-money-laundering / cash-transaction reporting. They are not interchangeable. Read your dealer's transaction confirmation carefully to understand which form applies to your specific transaction.

Real-world example — selling 30 Krugerrands to a dealer

Consider a seller delivering `30 × 1 oz` South African Krugerrands to a major US bullion dealer for buyback. The transaction is above the `25 oz` reportable threshold for Krugerrands. The dealer files Form `1099-B` reporting the gross proceeds (illustrative: `$2,400/oz × 30 oz × small under-spot discount = $71,500`). The customer receives Copy B of the `1099-B` by late January of the following tax year.

The customer's tax-reporting obligation: complete Form `8949` showing the `$71,500` proceeds (matching the `1099-B`), the basis from original purchase records (say `$60,000` for the lot purchased in `2020`), acquisition date, and resulting gain (`$71,500 − $60,000 = $11,500`). Holding period over `1` year qualifies as long-term, taxed at the `28%` maximum collectibles rate (lower of `28%` or the customer's ordinary marginal bracket). Federal tax: `$3,220` on the `$11,500` gain. The `1099-B` is the form that triggered third-party IRS notice; the tax calculation is done by the taxpayer on Schedule D. Compare to the equivalent sale of `30` American Gold Eagles: same tax calculation, but no `1099-B` filed. Taxpayer's obligation is identical; only the third-party-reporting layer differs.

Common misconceptions about 1099-B

**'No 1099-B = no taxable event.'** False, and one of the most common errors. The form is the dealer's reporting obligation, not the taxpayer's tax-liability trigger. Profitable sales of gold are taxable on Schedule D whether or not a `1099-B` was issued.

**'Eagles avoid all tax reporting.'** No. American Gold Eagles avoid the dealer-side `1099-B` reporting requirement on certain sales. The seller's own tax obligation is unchanged; self-reporting on Schedule D applies to all gold sales above the basis.

**'The 1099-B reports my gain.'** Partially. The `1099-B` reports the gross proceeds, not the net gain. Basis comes from the taxpayer's own records (dealer invoices, purchase confirmations). The taxpayer calculates gain on Form `8949`.

What this means for you

Form `1099-B` is the dealer's third-party reporting form, triggered on certain customer sales at or above specified thresholds (`25 oz` Krugerrands/Maples/Onzas, `100 oz` gold bars, etc.). American Gold Eagles are notably excluded from the reporting requirement. The form does not change your tax obligation — sales of gold above basis are taxable on Schedule D regardless of whether a `1099-B` was issued. Keep dealer invoices indefinitely for basis tracking. If you receive a `1099-B`, reconcile its proceeds figure against your records and complete Form `8949` accordingly. As always, BullionLens does not provide tax advice; consult a CPA who knows your specific situation.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Who issues a Form 1099-B?

The dealer (broker) issues Form 1099-B to the IRS and to the customer for certain qualifying transactions. The customer does not file the 1099-B themselves — they incorporate it into Schedule D on the personal tax return. -

Which gold sales trigger a 1099-B?

IRS-specified reportable transactions include 25+ oz gold Krugerrands, 25+ oz gold Maple Leafs, 25+ oz gold Mexican Onzas, and certain gold bar quantities of specific finenesses. American Gold Eagles are notable for NOT being on the reportable list at retail-customer scale. -

Does this only apply to the dealer?

The 1099-B reporting obligation is on the dealer. Tax reporting on the gain itself is still the seller's responsibility, regardless of whether a 1099-B was issued. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.