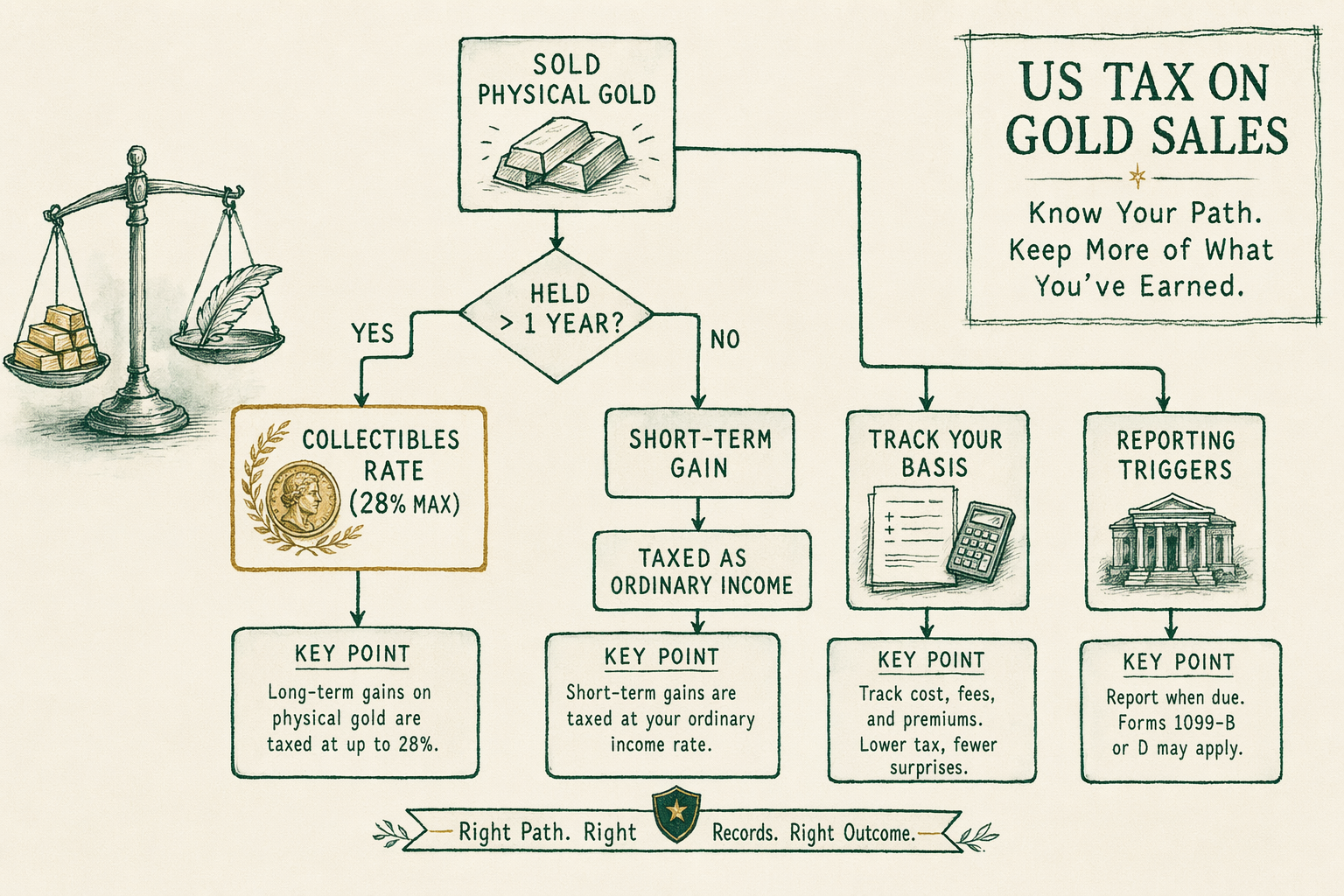

How is gold taxed when you sell it?

US tax treatment of physical gold sales: collectibles rate (28% max long-term), short-term gains as ordinary income, basis tracking, and reporting triggers.

The collectibles classification

Under US federal tax law, physical gold (and most other physical precious metals) is classified as a 'collectible' for capital gains purposes under Internal Revenue Code Section `408(m)`. This classification matters because long-term capital gains on collectibles are taxed at a maximum rate of `28%` — higher than the `20%` maximum that applies to most other long-term gains (stocks, bonds, real estate). The collectibles rate sits between the long-term equity-gain rate and the highest ordinary-income rate, reflecting Congress's intent to treat physical precious metals as a distinct asset class.

The `28%` figure is a ceiling, not a flat rate. Your actual long-term collectibles tax rate equals the lower of your ordinary marginal income tax rate or `28%`. A taxpayer whose marginal ordinary rate is `12%` pays `12%` on long-term gold gains; a taxpayer at the `37%` top marginal bracket pays `28%`. The Net Investment Income Tax (NIIT) of `3.8%` can also apply to high-income taxpayers on bullion gains, pushing the effective rate to `31.8%` for affected filers. State-level capital gains taxes apply on top of federal.

Long-term vs short-term gains

Short-term gains (gold held one year or less) are taxed as ordinary income at the seller's marginal tax bracket — no collectibles preference applies because the favorable rate kicks in only for long-term holding. For a taxpayer at the `32%` ordinary bracket, a short-term gold gain is taxed at `32%`. For someone at the `37%` top bracket, it's `37%`. Short-term gold trades are tax-inefficient compared to long-term holds.

The one-year holding period runs from the day after acquisition to the date of sale, calendar-day measured. Buy October `15, 2023`; the earliest day a sale qualifies for long-term treatment is October `16, 2024`. Sell on October `15, 2024` and the entire gain is short-term, taxed at ordinary rates. The arithmetic matters: an investor who would owe `28%` on a `$50,000` long-term gain (`$14,000` tax) but `37%` on the same as short-term (`$18,500` tax) saves `$4,500` by waiting one additional day across the year boundary.

Calculating your basis

Basis equals what you paid, including premiums over spot, shipping, insurance, and sales tax on the original purchase. For a bullion-grade `1 oz` American Gold Eagle purchased for `$2,520` (`$2,400` spot + `5%` premium), the basis is `$2,520` — even though the gold content was only `$2,400` of value at purchase. Gain on sale equals net sale proceeds minus basis. Sale price of `$3,000` minus basis of `$2,520` = `$480` taxable gain.

Multiple-purchase situations require lot tracking. If you bought `5` Eagles at `$2,520` each in `2022` and `5` Eagles at `$2,700` each in `2024`, then sell `3` Eagles in `2026`, you need to choose which lot to sell from. Specific-identification (you designate which `3` coins) gives you flexibility to optimize the gain. Absent specific identification, FIFO (first-in-first-out) typically applies. Keep purchase invoices indefinitely; the IRS does not have a statute of limitations on basis verification for assets you continue to hold.

Dealer reporting (1099-B)

Dealers must file IRS Form `1099-B` reporting certain customer sales above specific thresholds. The triggers are product-specific: sales (by you to the dealer) of `25` or more `1 oz` Gold Krugerrands, Maple Leafs, or Mexican Onzas trigger reporting; sales of `1 kg` gold bars or `100 oz` gold bars in certain finenesses trigger reporting; sales of American Gold Eagles are specifically excluded from `1099-B` reporting per IRS rules. The dealer files the `1099-B` with the IRS and sends a copy to you.

The `1099-B` triggers do not change your underlying tax obligation. Whether or not the dealer files a `1099-B`, you still owe capital gains tax on a profitable sale. The form changes only whether the IRS receives an independent third-party report of the transaction. Most US bullion sellers are tempted to think 'no `1099-B` = no taxable event' — this is incorrect. The IRS expects you to self-report all capital-asset sales on Schedule D regardless of whether a third-party form was filed.

Self-reporting on Schedule D

Sales of physical gold are reported on IRS Form `8949` and flow through to Schedule D (Capital Gains and Losses) on Form `1040`. The taxpayer enters acquisition date, sale date, proceeds, basis, and resulting gain or loss for each disposition. For collectibles like physical gold, gains are categorized separately so the `28%` maximum rate can be applied via the Schedule D Tax Worksheet (or its successor in the current IRS instructions).

Losses on physical gold sales are deductible on Schedule D against other capital gains, with up to `$3,000` of net capital loss applied against ordinary income per year (excess carried forward). The wash-sale rule that applies to stocks and securities does not apply to collectibles in the same way; you can realize a gold loss and re-purchase identical gold the next day without losing the loss deduction (consult a CPA — interpretation has nuances). Keep Schedule D records, supporting Form `8949`, and dealer paperwork for at least three years past the filing date, longer if you continue to hold other lots of the same asset.

Real-world example — a 7-year coin sale tax calculation

Consider an investor who purchased `20 × 1 oz` American Gold Eagles in August `2019` at `$1,520` per coin (`$1,450` spot + `4.8%` premium), total basis `$30,400`. In November `2026`, the investor sells the entire lot to a major online dealer for `$2,500` per coin (`$2,600` spot less a small buy-back discount), total proceeds `$50,000`. Holding period: over `7` years (long-term). Total gain: `$50,000 − $30,400 = $19,600`.

The investor is in the `32%` ordinary marginal bracket. Long-term collectibles rate is the lower of `32%` or `28%` = `28%`. Federal tax on the `$19,600` long-term gain: `$5,488`. NIIT does not apply at this income level. State capital gains tax (illustrative `5%` state) adds another `$980`. Total tax: `$6,468`, leaving net after-tax of `$43,532` on the original `$30,400` basis. American Gold Eagles are specifically excluded from `1099-B` dealer reporting per IRS rules, so no third-party form is filed — but the investor still reports the sale on Form `8949` and Schedule D and pays the tax owed. Records kept: original dealer invoice from `2019` (showing the `$30,400` basis), the `2026` dealer sale confirmation, and the Form `8949` worksheet.

Common misconceptions about gold taxation

**'Gold gains are taxed at the same rate as stocks.'** No. Physical gold is a collectible under IRS rules; long-term gains carry a `28%` maximum rate versus `20%` maximum for most other long-term capital gains. The difference is material for high-income filers.

**'No 1099-B = no taxable event.'** No. The `1099-B` is the dealer-reporting trigger, not the taxable-event trigger. Whether or not a `1099-B` is filed, you owe capital gains tax on profitable sales and must self-report on Schedule D.

**'I can claim a loss and buy back the next day without restriction.'** Probably yes for collectibles, but the wash-sale rule interpretation has nuances. Consult a CPA before relying on this position for any large loss harvest.

What this means for you

Physical gold gains are taxed at a maximum `28%` long-term collectibles rate, higher than the `20%` maximum for most other long-term gains. Short-term gains are taxed as ordinary income. Track basis carefully — keep dealer invoices indefinitely. Self-report on Schedule D regardless of whether a Form `1099-B` was filed. Inside an IRA wrapper, gains compound tax-deferred (Traditional) or tax-free-on-qualified-distribution (Roth), which is one of the structural reasons many investors prefer Gold IRA wrappers over after-tax holdings for substantial allocations. As always, BullionLens does not provide tax advice; consult a CPA who knows your specific situation.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is the maximum tax rate on physical gold gains?

Long-term capital gains on physical gold (held more than 12 months) are taxed at a maximum 28% rate under the collectibles rules — higher than the 20% maximum on most other long-term capital gains. Consult a CPA on your specific situation. -

How do I track my basis?

Keep dealer invoices showing the purchase date, weight, and total price paid (including premiums and shipping). Basis is what you paid; gain is sale price minus basis. -

What if I lose my purchase records?

The IRS expects taxpayers to document basis. Without records, the worst-case position is a zero-basis assumption (entire proceeds taxable). Keep dealer paperwork. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.