What is the spread on gold?

Bid-ask spread on gold explained: how dealers set their buy and sell prices, what spread to expect on common products, and what tight vs wide spreads tell you.

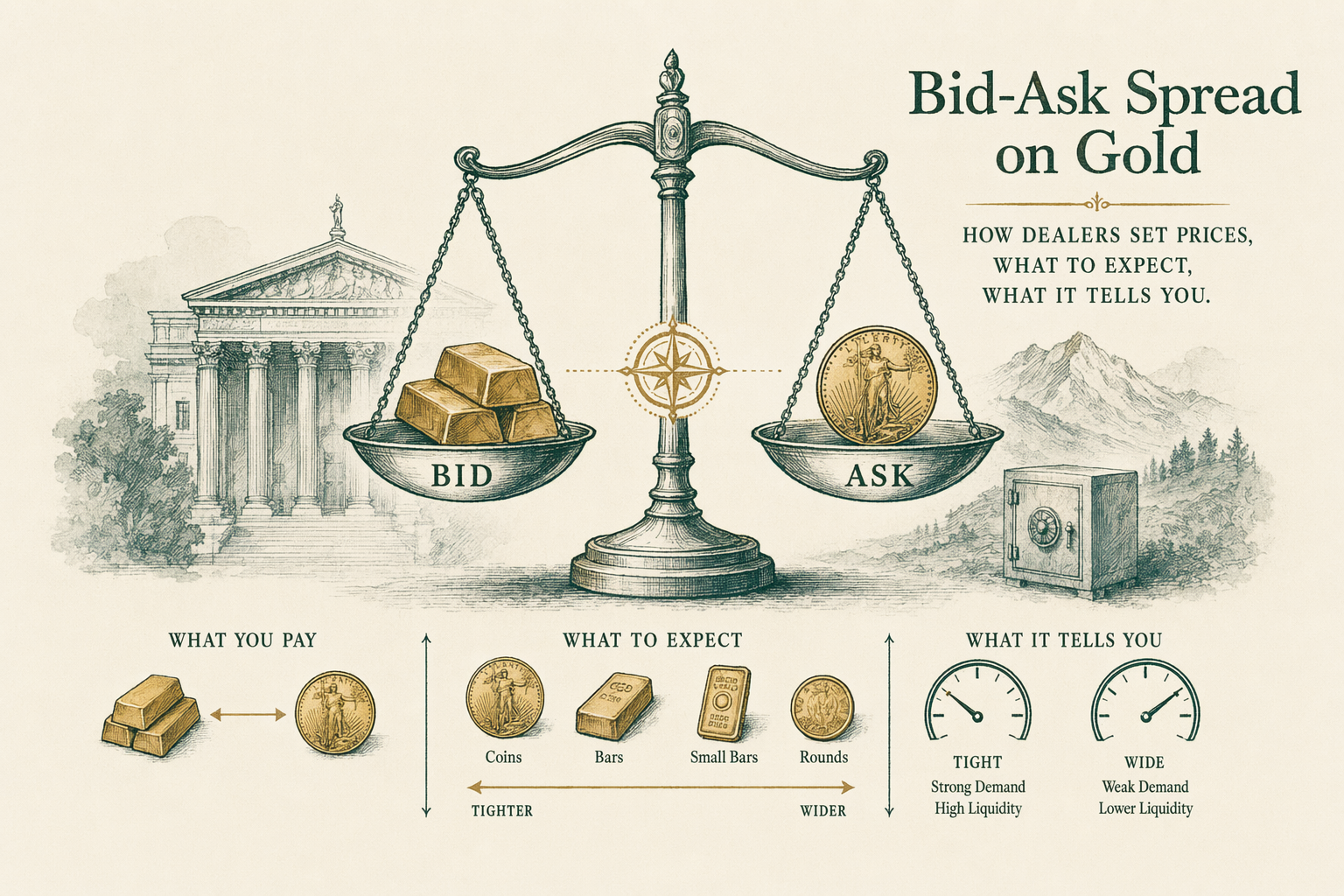

Bid, ask, and the spread

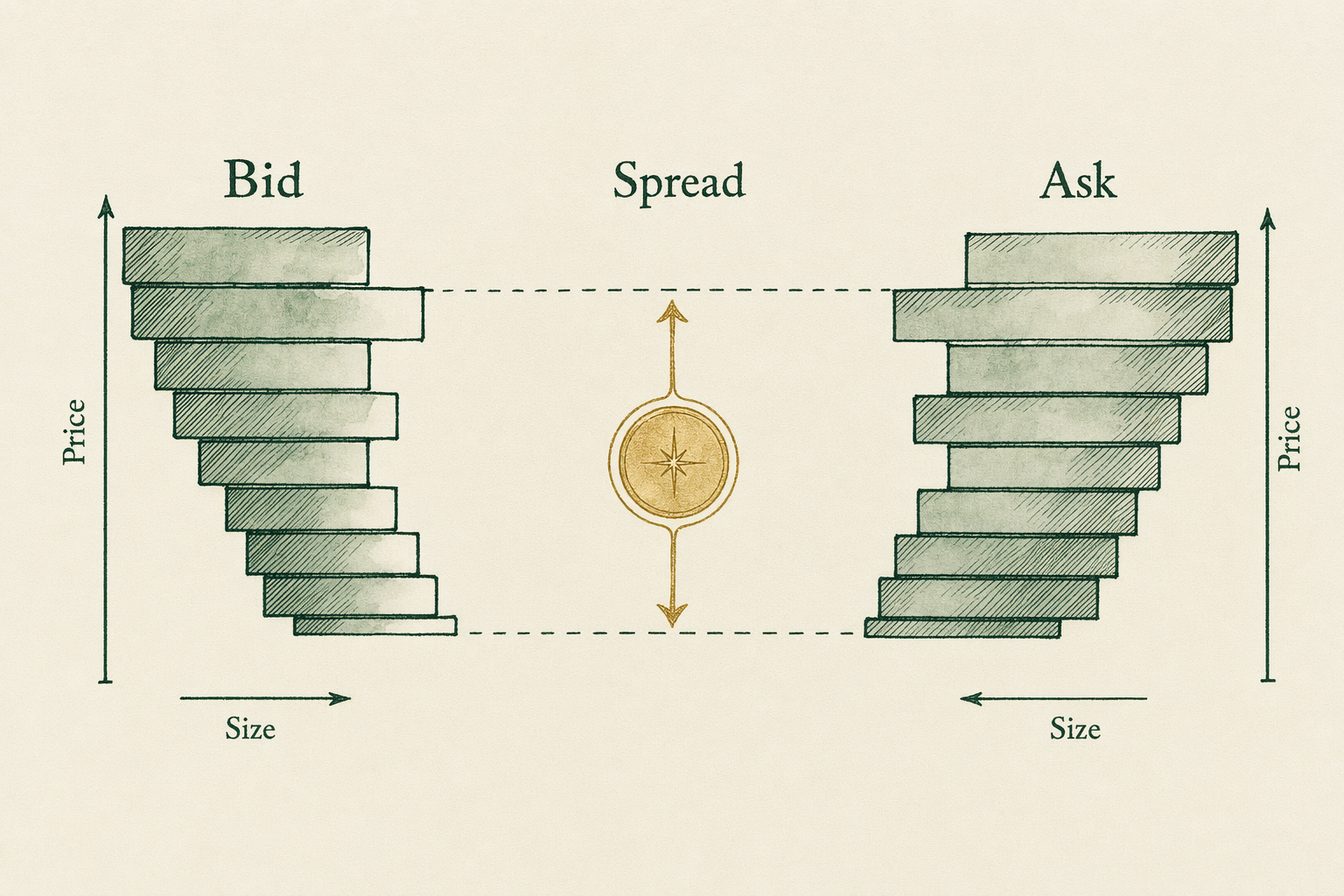

The bid-ask spread is the gap between the dealer's bid price (what they pay if you sell to them) and the dealer's ask price (what they charge if you buy from them). At an illustrative LBMA spot of `$2,400/oz`, a dealer might quote a bid of `$2,395` per coin and an ask of `$2,520` per coin on a `1 oz` American Gold Eagle — a `$125` spread, or roughly `5.2%` of the ask. The spread covers fabrication cost (mint markup over spot to the dealer), distribution cost, dealer operational overhead, dealer margin, and the dealer's risk capital tied up in inventory.

Both sides of the spread move together as spot moves. If spot rises `$50/oz`, both the bid and ask typically rise by approximately `$50` (after a brief delay as the dealer re-prices inventory). The percentage spread remains roughly constant in calm markets. During supply-stress periods or rapid spot moves, the spread can widen sharply — the bid sometimes lagging, the ask sometimes rising faster than spot — as the dealer protects against inventory risk. Buyers should pay attention to both the headline ask price and the dealer's bid (the latter is what determines exit liquidity if you ever sell back).

Spread on common 1 oz gold coins

Typical bid-ask spreads on `1 oz` sovereign gold coins at major US dealers in calm market conditions: American Gold Eagle, `4-7%` of spot; Canadian Gold Maple Leaf, `3-5%`; American Gold Buffalo, `5-8%`; Austrian Gold Philharmonic, `3-5%`; Australian Gold Kangaroo, `3-5%`. Bullion-grade rounds from private mints (`1 oz` rounds from PAMP Suisse, Credit Suisse, Sunshine Mint, etc.) typically run `2-4%` spread — tighter than sovereign coins because of the lower fabrication overhead.

These ranges reflect calm-market norms at major online dealers (APMEX, JM Bullion, Money Metals Exchange). Smaller regional coin shops typically run wider spreads — `8-12%` on the same products is not unusual at independent shops without the volume and direct-mint relationships of major dealers. The spread variance across dealers on identical products is real and material; for any meaningful purchase, comparison-shop at least three dealers at the same minute on the specific product configuration.

Spread on larger bars

Per-ounce spreads narrow on larger bullion formats. A `1 oz` minted bar from an LBMA-Good-Delivery-listed refiner (PAMP Suisse, Valcambi) runs roughly `3-5%` spread. A `10 oz` minted bar runs roughly `1.5-3%`. A `kilo bar` (`32.15 troy oz`) runs roughly `1-2%`. A `400 oz` London Good Delivery bar (the institutional-tier format) runs roughly `0.25-1%`. The narrowing reflects fixed fabrication cost being spread over more ounces — making a `10 oz` bar costs less than `10x` making a `1 oz` bar, so per-ounce overhead drops as size grows.

Tradeoffs as bar size grows: lower per-ounce spread, but reduced flexibility on partial liquidation. A `kilo bar` cannot be split into smaller pieces — to sell `5 oz`, you must sell the whole bar. For investors building positions in the `10-50 oz` range, the kilo-bar economics are compelling; for smaller positions or those with potential partial-liquidation needs, a mix of `1 oz` coins and `10 oz` bars provides spread efficiency plus flexibility. The right format depends on the holder's exit-strategy expectations, not just the headline spread.

Why spreads widen

Spreads widen during three identifiable scenarios. First, supply stress: when US Mint coin allocations tighten (March `2020`, certain `2022-2023` windows), retail dealers can't restock at their usual pace and protect margins by widening the ask. Premiums on `1 oz` American Gold Eagles reached `10-15%` over spot for weeks during the early-`2020` window; spreads on the bid widened proportionally. Second, rapid spot moves: in high-volatility days, dealers re-price more frequently and conservatively, widening spreads against the risk of inventory whiplash.

Third, low-liquidity products. Spreads on rare sovereign coins (Australian Lunar series with specific years, older British Sovereigns, Swiss Vrenelis) run wider than on staple Eagles or Maples because the dealer's inventory turnover on the niche product is slower. Numismatic coins (graded examples, scarce dates, specialty issues) have spreads in the `20-40%+` range — the dealer is taking inventory risk on a product with thin retail demand. For staple bullion-grade product, the spread is a function of the metal's own structural costs; for niche product, the spread is a function of dealer-inventory risk.

Comparing dealer spreads

To compare dealer spreads across vendors, pull live bid and ask quotes on identical product (single `1 oz` American Gold Eagle, payment by bank wire, shipping to your state) from three dealers at the same minute. Calculate the all-in landed cost — ask price plus shipping plus any payment surcharge — and the spread to the same dealer's bid for the same product. The all-in cost on the ask side is what determines your purchase economics; the bid spread to that dealer's own buy price determines round-trip cost if you ever sell back to them.

Comparison patterns: APMEX and JM Bullion typically run similar spreads on staple products, within a few dollars of each other on any given minute. Money Metals Exchange and SD Bullion typically run slightly tighter spreads on the cheapest end. Local coin shops vary widely — the established ones can compete with online dealers on staple products, while smaller or specialty shops often run wider spreads. The right shop for any specific transaction depends on the buyer's location, the specific product, the payment method, and the moment in time. Spreads are not stable benchmarks; they're momentary readings.

Real-world example — spread on a 5 oz purchase

Consider a buyer purchasing `5 × 1 oz` American Gold Eagles. At illustrative LBMA spot of `$2,400/oz`, three dealers offer simultaneously: Dealer A — ask `$2,525` per coin, bid `$2,395` per coin (spread `5.4%`); Dealer B — ask `$2,510` per coin, bid `$2,400` per coin (spread `4.6%`); Dealer C — ask `$2,540` per coin, bid `$2,410` per coin (spread `5.4%`). All three are A+ BBB-rated established dealers.

Total purchase cost: Dealer A `$2,525 × 5 = $12,625`; Dealer B `$12,550`; Dealer C `$12,700`. Lowest-cost purchase is Dealer B at `$12,550`. On round-trip math: if the buyer sells back to Dealer A `2` years later at the then-current bid (assuming flat spot), Dealer A's bid would be `$2,395 × 5 = $11,975`. Round-trip cost at Dealer A's spread: `$650`. Dealer B's round-trip cost at the same hold period: `$2,400 × 5 = $12,000` recoverable, so `$550` round-trip cost. Dealer C's would be `$700`. The tightest-spread dealer (B) is cheapest for both the initial purchase and the eventual round-trip exit. Comparison-shopping pays.

Common misconceptions about gold spreads

**'The headline spot price is what I pay.'** No. The headline spot is the institutional reference; retail buyers pay spot plus the dealer's ask spread. For a `1 oz` Gold Eagle, that's typically `4-7%` over spot under normal conditions.

**'Tighter spread = better dealer.'** Tight spread is one factor among several. Reputation, BBB record, shipping discipline, buyback fairness, and operational history matter alongside the headline price. A dealer with the tightest spread but poor BBB record is not obviously the right choice.

**'Spreads are constant.'** No. Spreads widen during supply stress, rapid spot moves, and on low-liquidity products. The percentage spread you see at one moment is not a reliable forecast of spread at another time.

What this means for you

The spread on gold reflects the gap between what a dealer charges to sell and what they pay to buy. Typical retail spreads on `1 oz` American Gold Eagles run `4-7%` in calm markets, wider during supply stress. Per-ounce spreads narrow as bar size grows — kilo bars run `1-2%` versus `5%+` on `1 oz` coins. To minimize total cost-of-ownership, comparison-shop at least three established dealers on the same product and same minute, evaluate both the ask (purchase cost) and the bid (eventual exit), and choose based on total round-trip economics rather than headline price alone. As always, BullionLens does not provide personalized investment advice; consult a licensed adviser for allocation decisions.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is a typical spread on a 1 oz Gold Eagle?

At retail dealers, the bid-ask spread on a single 1 oz American Gold Eagle is typically 4-7% in calm markets. During supply stress (early 2020) spreads widened to 10-15% briefly. -

Is a tighter spread better?

For the buyer, yes — but tight spreads can also signal a thinly-capitalized dealer matching aggressive competitors. Reputation and BBB record matter alongside spread. -

Are spreads tighter on bigger bars?

Yes. Per-ounce spread on a 10 oz bar or kilo bar is typically half the per-ounce spread on a 1 oz coin, because fixed fabrication and dealer costs spread over more ounces. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.