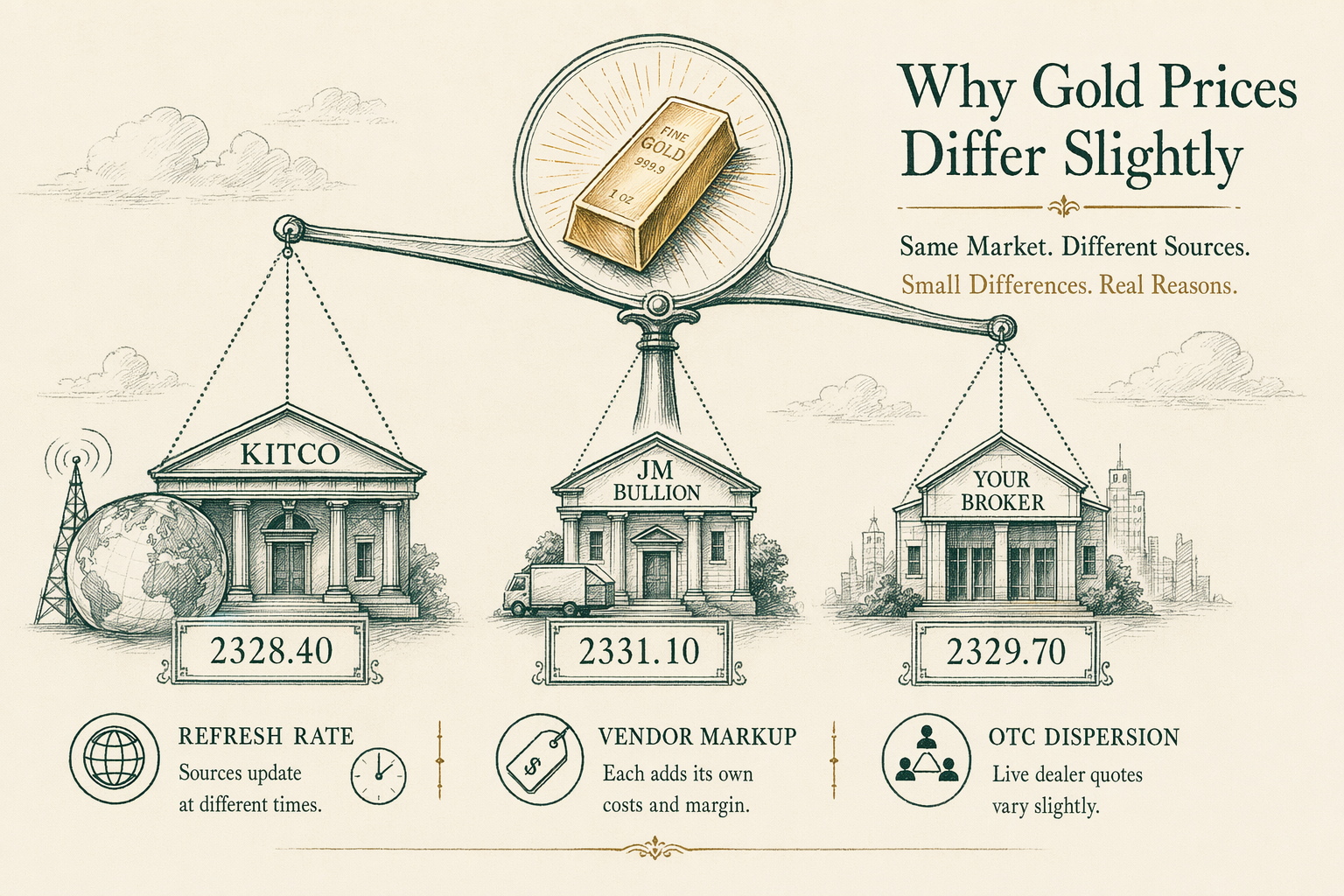

Why does the gold spot price vary between sources?

Why Kitco, JM Bullion, and your broker show slightly different gold spot prices. Vendor markups, refresh rates, and the OTC quote dispersion.

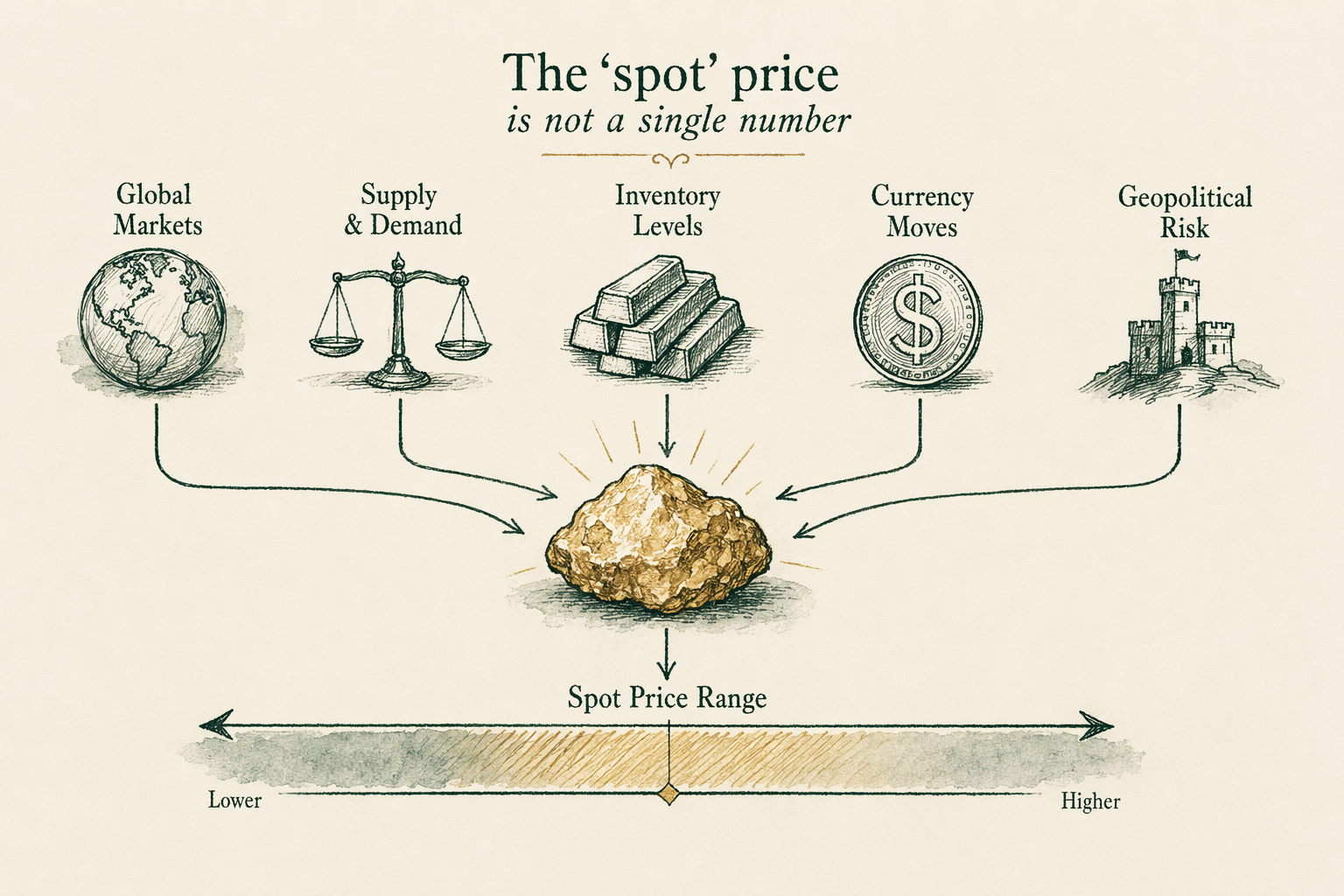

The 'spot' price is not a single number

There is no single 'spot price of gold' in the way there's a single closing price for a publicly-traded stock. Gold trades primarily in the over-the-counter (OTC) market — a network of banks, brokers, and dealers exchanging quotes via voice, electronic platforms, and bilateral relationships. At any given moment, dozens of institutional participants are quoting bid and ask prices on gold for immediate delivery. The 'spot' price is the consensus emerging from this distributed quote stream; different participants observe slightly different prices depending on which counterparties they see and how recently their quotes refreshed.

This structure is different from equity markets where a centralized exchange (NYSE, NASDAQ) consolidates orders into a single visible last-trade price. The OTC gold market has no central tape. Public-facing 'spot' tickers — what you see on Kitco, JM Bullion, APMEX, Bloomberg, your retail brokerage — are vendor-aggregated views of the underlying OTC stream. Each vendor uses its own selection of source quotes, its own averaging methodology, and its own refresh cadence. Two vendors looking at gold at the same wall-clock minute can legitimately show prices `$1-3` apart and both be 'correct' from their respective vantage points.

OTC dealer quotes and refresh rates

Major institutional dealers (JPMorgan, HSBC, ICBC Standard Bank, UBS, Goldman Sachs, and others) maintain continuous gold price-making operations across global trading sessions. London and Zurich open early UTC; New York opens late UTC; Hong Kong and Singapore cover the Asian window. Each dealer's quote stream updates frequently — typically every few seconds during liquid market hours — and the dealer's published bid and ask shift to reflect their inventory position, their recent counterparty flow, and the broader OTC consensus.

Retail-facing 'spot' tickers consume one or more of these institutional quote streams and republish them with their own update cadence. Kitco's stream typically refreshes every few seconds; JM Bullion's quote on a specific product reflects a slower refresh paired with the dealer's own markup. Some vendors update every minute; some on browser refresh; some only when a user initiates a quote request at checkout. The mix of source-quote freshness and vendor-republish cadence produces the dispersion users see comparing tickers across windows.

Vendor markups on retail tickers

Some retail bullion vendors display 'spot price' alongside product prices with their own embedded markup baked into the spot figure. Others display the institutional spot accurately and show the markup as a separate 'premium' line item. A vendor that adds `$5/oz` to its displayed 'spot' creates the appearance of a wider product premium when in fact the markup was already in the spot column. This is not necessarily deceptive — vendors disclose their methodology — but it does mean that comparing 'spot' prices across vendors should be done carefully.

For the cleanest 'what is gold worth right now' reading, the LBMA Gold Price (twice-daily auction-based London benchmark, set by participating banks) is the most-documented and most-cited benchmark. The fixings are formal, time-stamped, and archived; they're cited in regulatory and academic literature. For real-time indicative reference, established dealers' published streams (Kitco's, APMEX's, JM Bullion's, exchange-based COMEX futures fronts converted to spot-equivalent) all give reasonable readings; expect minor dispersion. For a high-stakes transaction, the price that matters is the one quoted by the dealer at the moment you confirm the order — that's the lock price you'll pay, not the public-ticker price.

LBMA fixings as a benchmark

The LBMA (London Bullion Market Association) Gold Price is the most widely cited institutional benchmark. The price is set twice daily — `10:30 AM` and `3:00 PM` London time — via an auction-based mechanism administered by ICE Benchmark Administration. Major bullion banks (currently including JPMorgan, HSBC, ICBC Standard, Toronto-Dominion, and others) participate; the fixing reflects the equilibrium price at which buy and sell orders match in the auction.

LBMA fixings are the reference price for institutional contracts, regulatory disclosures, central-bank reporting, and most academic gold-price research. When a research paper or financial report cites 'the price of gold' on a specific date, they almost always mean the LBMA PM Fix. For day-to-day retail buying, the fixings are too infrequent to use as live pricing; but they're the right benchmark for documenting a price at a specific point in time. BullionLens cites LBMA fixings in case studies, historical analyses, and any context where a documented reference price matters.

What dispersion is normal

In calm market conditions during liquid trading hours, dispersion of `$0.50-3.00 per troy oz` between mainstream retail spot tickers (Kitco, JM Bullion, APMEX, Bloomberg, retail-broker feeds) is typical. During high-volatility days, dispersion widens — `$3-10/oz` is observable between different vendors at the same wall-clock minute. During market closures or weekends (when liquid OTC trading is sparse), vendor streams can diverge more meaningfully.

When ordering bullion at retail, the spot price displayed on the vendor's site is indicative — the price that determines what you pay is the locked quote generated when you confirm the order, plus the premium the vendor charges over their then-current spot. Two vendors showing different 'spot' prices simultaneously may quote nearly-identical all-in costs once their respective premiums are applied. Compare total all-in landed cost (spot + premium + shipping + payment surcharge) at the time you intend to buy, not the displayed spot price alone.

Real-world example — three spot quotes at the same minute

Consider a buyer pulling spot quotes at the same wall-clock minute (say `2:30 PM ET` on a weekday) from three sources: Kitco shows `$2,398.50`; JM Bullion shows `$2,400.10`; APMEX shows `$2,399.20`. The dispersion is `$1.60/oz` — well within normal calm-market range. All three are 'correct' from their respective source-quote streams; the small differences reflect refresh-rate timing and aggregation methodology.

If the buyer then proceeds to confirm a `5 × 1 oz Gold Eagle` order at each dealer at the same minute, the all-in landed cost might be: JM Bullion `$12,550` (the dealer's premium and surcharge applied to their quoted spot); APMEX `$12,605`; a third dealer not even on Kitco might come in at `$12,490`. The all-in landed cost differs by `$115` — meaningful and worth comparison-shopping — but it isn't driven primarily by the displayed-spot differences; it's driven by dealer-premium structure and any payment-method surcharges. The lesson: the spot ticker is a useful real-time reference, but the dealer's specific quote at the moment of order is what matters for the transaction.

Common misconceptions about gold spot

**'There is one true spot price.'** No. Gold trades OTC with no centralized tape. Multiple legitimate streams produce slightly different readings at any moment.

**'Higher spot = higher quality source.'** No. Spot dispersion reflects refresh-rate timing and methodology, not data quality. A `$2,398.50` quote and a `$2,400.10` quote at the same minute are both correct from their respective vantage points.

**'The displayed spot is what I pay.'** No. Retail buyers pay spot plus a dealer premium plus any payment-method surcharge. The displayed spot is indicative; the locked dealer quote at order confirmation is what you'll actually pay.

What this means for you

The gold spot price varies across sources because there's no centralized exchange and no single tape — gold trades OTC through distributed dealer quote streams. Dispersion of `$0.50-3/oz` between mainstream spot tickers in calm markets is normal and expected. For a documented benchmark, cite the LBMA Gold Price (twice-daily London fixing). For real-time indicative reference, established dealer streams all give reasonable readings; expect minor variation. For actual transactions, the price that matters is the locked dealer quote at order confirmation, not the public-ticker spot. Compare all-in landed cost across dealers on the same product at the same minute. As always, BullionLens does not provide investment advice; consult a licensed adviser for allocation decisions.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Why is Kitco's gold price different from my dealer's?

Retail tickers reflect a stream of OTC quotes plus vendor formatting. Dealers add their own markup and refresh on their own cadence. Dispersion of $0.50-$3 between sources is typical. -

Which spot source should I trust?

For a documented benchmark, cite the LBMA Gold Price (twice-daily London fixing). For an indicative real-time reference, established dealers and exchanges all publish reasonable streams; expect minor dispersion. -

Why does the price 'lock' when I'm checking out?

Dealers offer a price lock at the moment you confirm the order, giving the dealer a few hours to hedge the position. Lock terms vary; some dealers void the lock if you do not pay within the window. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.