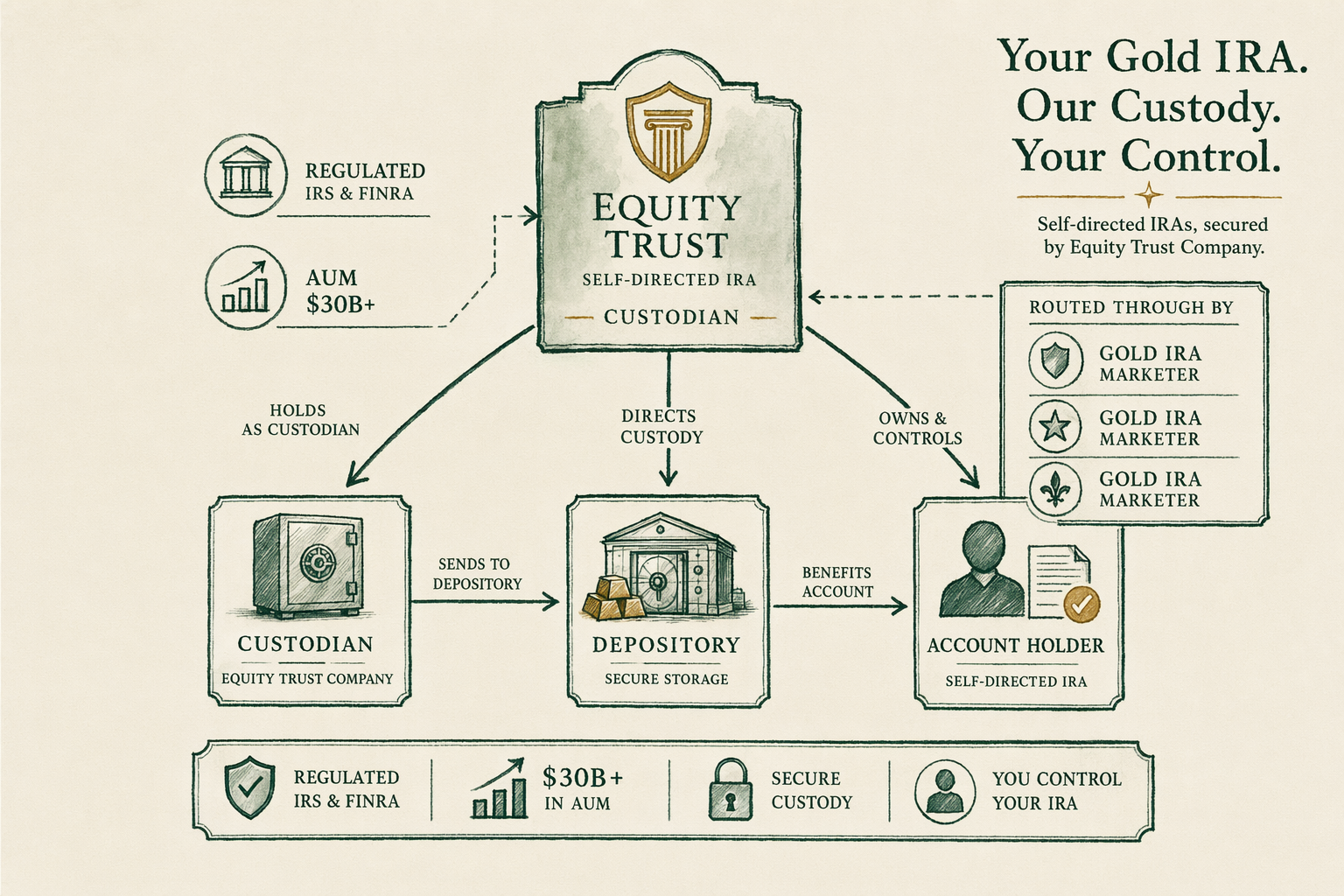

Who is Equity Trust Company?

Equity Trust Company as a self-directed IRA custodian: regulatory status, AUM, custody role, and which Gold IRA marketers route accounts through them.

Founding and background

Equity Trust Company was founded in 1974 and is headquartered in Westlake, Ohio. The company is a state-chartered trust company — originally chartered in South Dakota and more recently restructured under different state charters — that specializes in self-directed Individual Retirement Account custody. The company is privately held and reports custodied assets in the tens of billions of dollars across hundreds of thousands of accounts.

Self-directed IRA custodians are a small specialty industry within US retirement services. The main players — Equity Trust, STRATA Trust, Kingdom Trust, Madison Trust, the Entrust Group — collectively hold the substantial majority of self-directed IRA assets in the United States. Equity Trust is the largest of these by account count. Snapshot as of `2026-Q2`.

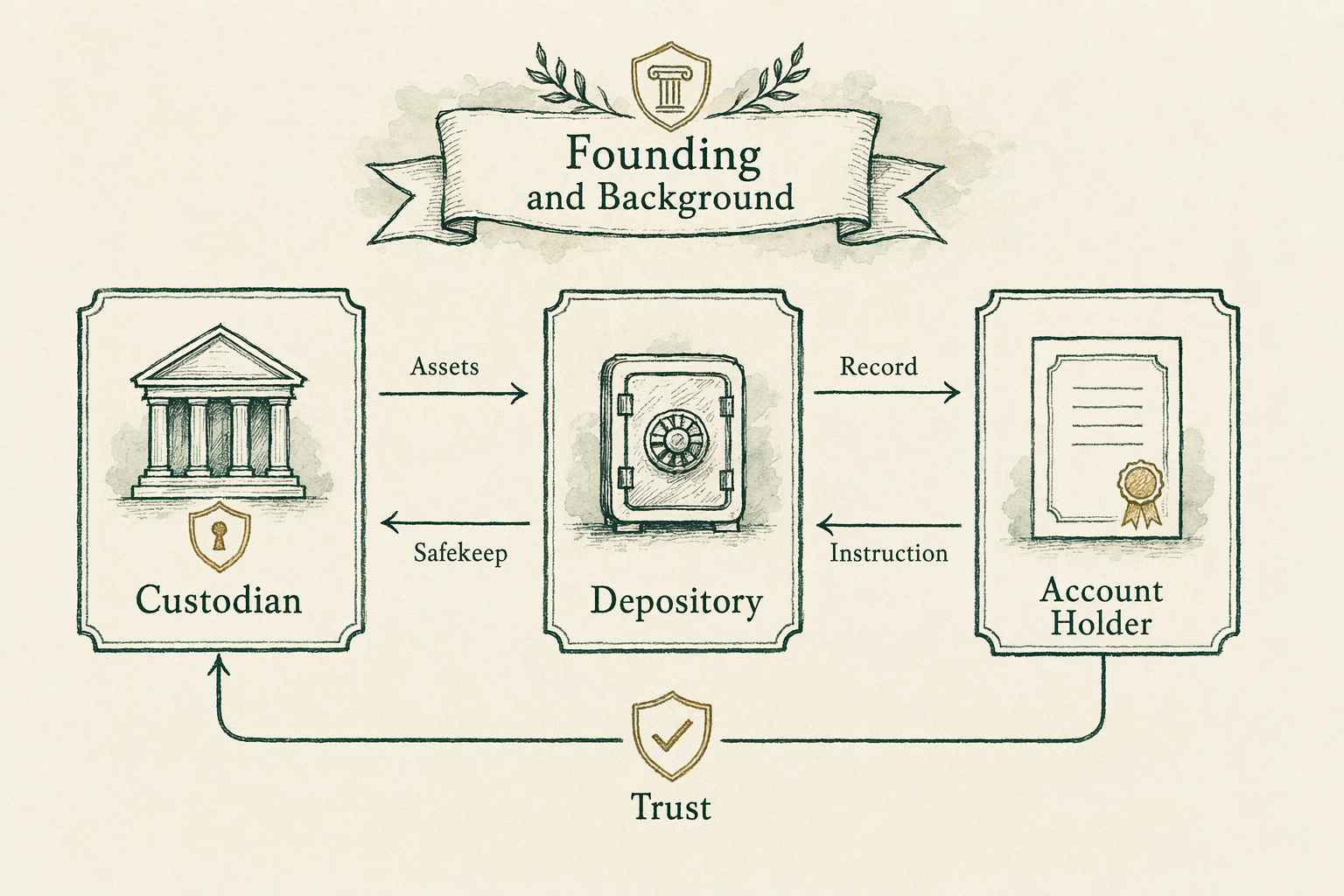

Custodian role under IRS rules

Under Internal Revenue Code § 408, every IRA must have a qualified custodian or trustee. The custodian is the entity that holds legal title to IRA assets, files Form 5498 annually with the IRS reporting contributions and fair market value, files Form 1099-R when distributions are taken, and ensures the IRA complies with the prohibited-transaction rules under IRC § 4975.

For Gold IRAs specifically, IRC § 408(m) restricts permissible bullion to specifically enumerated coin types and bars meeting `0.995` fineness for gold (`0.999` for silver). IRC § 408(n) requires the metal to be held by an IRS-approved non-bank trustee — that is, by an approved depository (Delaware Depository, Brink's Global Services, IDS of Texas, others). The custodian (Equity Trust) holds the legal IRA title and the recordkeeping; the depository holds the physical metal. The two roles are separate.

AUM scale

Equity Trust reports custodied assets in excess of `$45 billion` across roughly `420,000` accounts at the time of this review. The scale is meaningful — it makes Equity Trust the dominant custodian in the self-directed IRA category, comfortably ahead of STRATA Trust (the second-largest in the precious-metals subset) and ahead of more niche custodians like Kingdom Trust and Madison Trust.

The scale advantage matters in two ways. The first is operational maturity — Equity Trust's account-opening, distribution, and rollover processes are heavily templated, which reduces error rates and timing delays. The second is fee stability — at this AUM scale, the custodian can afford steady fee schedules without surprise increases. Smaller custodians have, historically, raised fees more frequently.

Which Gold IRA companies route through Equity Trust

The major Gold IRA marketing companies that have historically used Equity Trust as a primary or co-equal custodian include Goldco, Augusta Precious Metals, Birch Gold Group, American Hartford Gold, Noble Gold, Lear Capital, and Preserve Gold. Several of these companies also route accounts through STRATA Trust as an alternate, and the assignment can be at the buyer's discretion in some cases.

The implication for a Gold IRA buyer: the custodian relationship is roughly the same regardless of which Gold IRA marketing company sold the account. The marketing-company differences live in the markup on the bullion, in the sales-process experience, and in the buyback policy — not in the underlying custody arrangement at Equity Trust. Confirm in writing which custodian will be assigned to your account before signing the application; ask for the published custodian fee schedule separately from the marketing materials.

Account holder responsibilities

The IRA account holder retains responsibility for compliance with IRS rules. The custodian processes the paperwork and files the required forms, but does not provide investment advice or guarantee that the account holder's instructions comply with prohibited-transaction rules under IRC § 4975. The custodian will execute the account holder's directed transactions; it is the account holder's responsibility to ensure each transaction is permissible.

Practical responsibilities for a Gold IRA account holder at Equity Trust: (1) verify the depository assignment in writing and contact the depository directly to confirm; (2) review the annual Form 5498 for accuracy; (3) understand the in-kind distribution mechanics if you intend to take physical possession at distribution age; (4) maintain personal records of the cost basis on each metal purchase for tax purposes at distribution; (5) confirm prohibited-transaction rules apply to your specific circumstances before engaging any transaction involving a disqualified person.

The custodian does not warn you if a directed transaction violates the prohibited-transaction rules. The responsibility for compliance rests with the account holder.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Is Equity Trust a Gold IRA company?

No — Equity Trust is a self-directed IRA custodian. Many Gold IRA marketing companies use Equity Trust as the underlying custodian, but Equity Trust itself does not market Gold IRAs to retail buyers. -

Is Equity Trust regulated?

Yes. Equity Trust is a South Dakota-chartered trust company subject to state and federal trust-company regulation. -

How do custodian fees compare to Gold IRA marketing company fees?

Custodian fees (account administration, recordkeeping) are usually a flat $80-$200 annually. Gold IRA marketing-company fees are typically bundled into the markup on the metal purchase — a much larger first-year cost. -

Can I change custodians later?

Yes. A trustee-to-trustee transfer between IRA custodians is permitted and tax-neutral. You can re-route an existing Gold IRA to a different custodian if you become dissatisfied, though logistics may take 2-6 weeks.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.