Gold for 401(k) rollovers

Editorial guide to rolling 401(k) assets into a Gold IRA: distributable events, direct vs indirect rollover, 60-day rule, and the operational sequence.

If you are sitting on a 401(k) and thinking about gold

If you have a `401(k)` balance from a current or former employer and you are considering moving some portion into a Gold IRA, the path forward depends on three operational details most retirement plans do not advertise. First, whether your plan permits a rollover at this point in time (the answer is yes if you have left the employer, are over `59½` with in-service distribution rights, or have specific hardship qualifications, and is often no otherwise). Second, whether you do a direct rollover (trustee-to-trustee, simpler, fewer pitfalls) or an indirect rollover (you receive a check, deposit within `60` days, withholding complications). Third, which Gold IRA company, custodian, and depository to use on the receiving side.

This guide walks each of the three operational decisions with the IRS rules attached. The desk does not recommend a specific allocation amount or argue that gold is the right answer for your portfolio; the percentage question belongs with a licensed adviser. What the desk does is walk the mechanics so you know what to expect, where the friction points are, and which questions to bring to the receiving Gold IRA company's representatives before you sign paperwork.

What this guide covers

Five sections. First, the 'distributable event' question: under what conditions your current plan permits a rollover. Second, the direct rollover mechanics (trustee-to-trustee transfer, no withholding, no `60`-day clock). Third, the indirect rollover mechanics and the `60`-day rule that governs them, including the mandatory `20%` withholding on indirect rollovers from `401(k)` plans. Fourth, the timing and likely friction points — paperwork delays, plan-administrator processing windows, and the practical sequencing of the new-account opening at the receiving Gold IRA company.

Fifth, the receiving-side decisions: which Gold IRA company, which custodian, which depository. The custodian holds the IRS-recognized trust company role; the depository holds the physical metal; the Gold IRA marketing company introduces you to both. The three roles are legally separate and the comparison criteria are different for each. Each section ends with the questions worth asking the relevant party before you sign.

Note: every claim about a Gold IRA company in this guide and the linked reviews carries a `2026-Q2` snapshot date. Fees and policies change. Confirm current arrangements with the company's published fee schedule before committing.

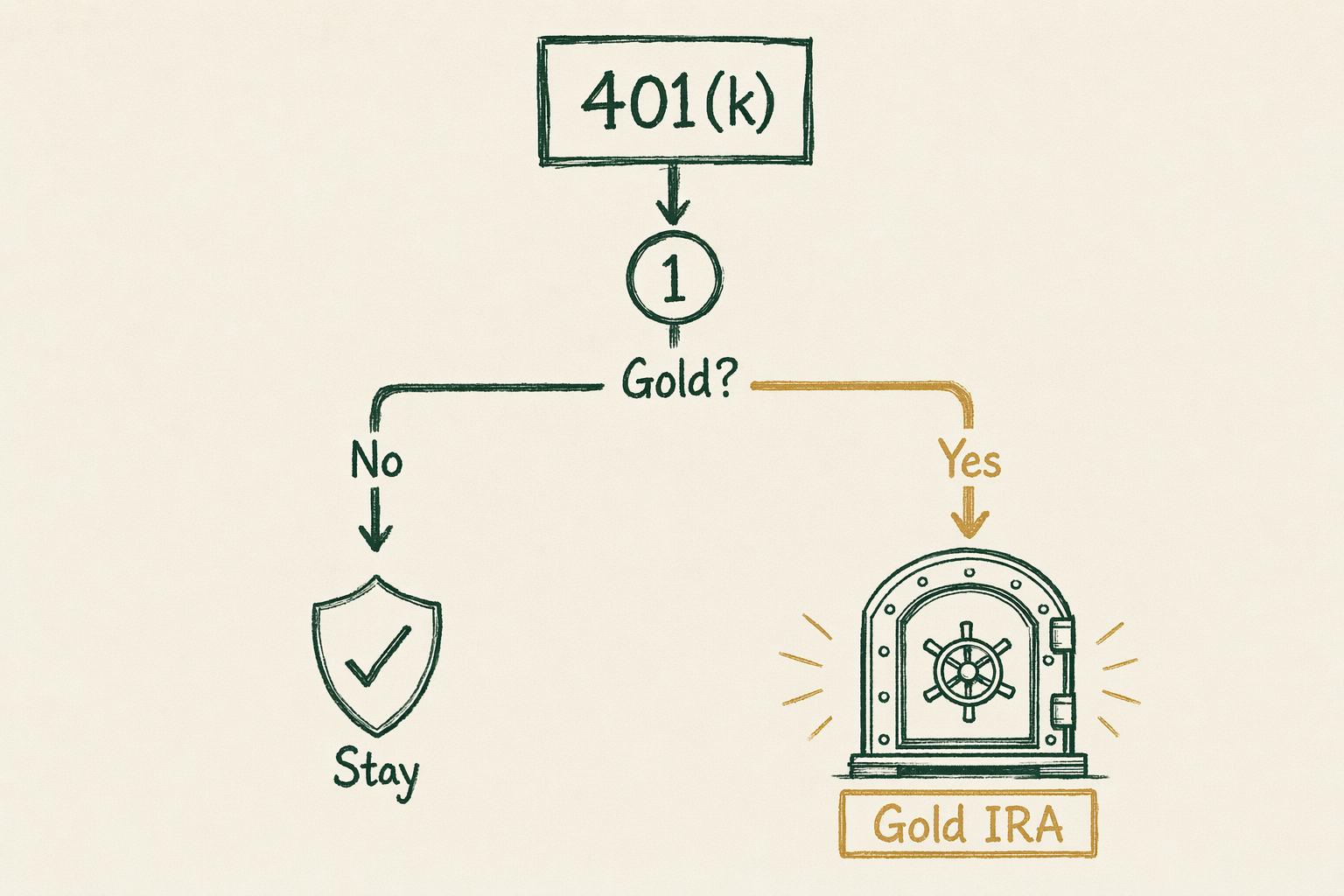

Distributable events that unlock a rollover

A `401(k)` rollover requires a 'distributable event' under the plan's terms and under the IRC. The most common distributable events are separation from the employer (whether voluntary departure or termination), reaching age `59½` with in-service distribution rights enabled by the plan, attainment of normal retirement age as defined in the plan, disability, and (rarely) hardship withdrawal which has different treatment and is not typically used for rollover purposes.

Active `401(k)` accounts with a current employer typically cannot be rolled over unless the plan explicitly permits in-service distributions. Some plans permit in-service distributions at age `59½`; others permit them only at normal retirement age; others not at all. The plan's Summary Plan Description (SPD) is the governing document — request a copy from the plan administrator if you do not already have one.

If you have separated from a former employer, the `401(k)` balance from that employer is rollover-eligible immediately. If you have multiple `401(k)`s from multiple former employers, each is independently rollover-eligible (though some readers consolidate into a single IRA for simpler administration). The mechanics described below apply equally to a separated-employer `401(k)`, a `403(b)` from a former educational or non-profit employer, a `457(b)` from a former government employer, and a Thrift Savings Plan for former federal employees.

Direct rollover paperwork

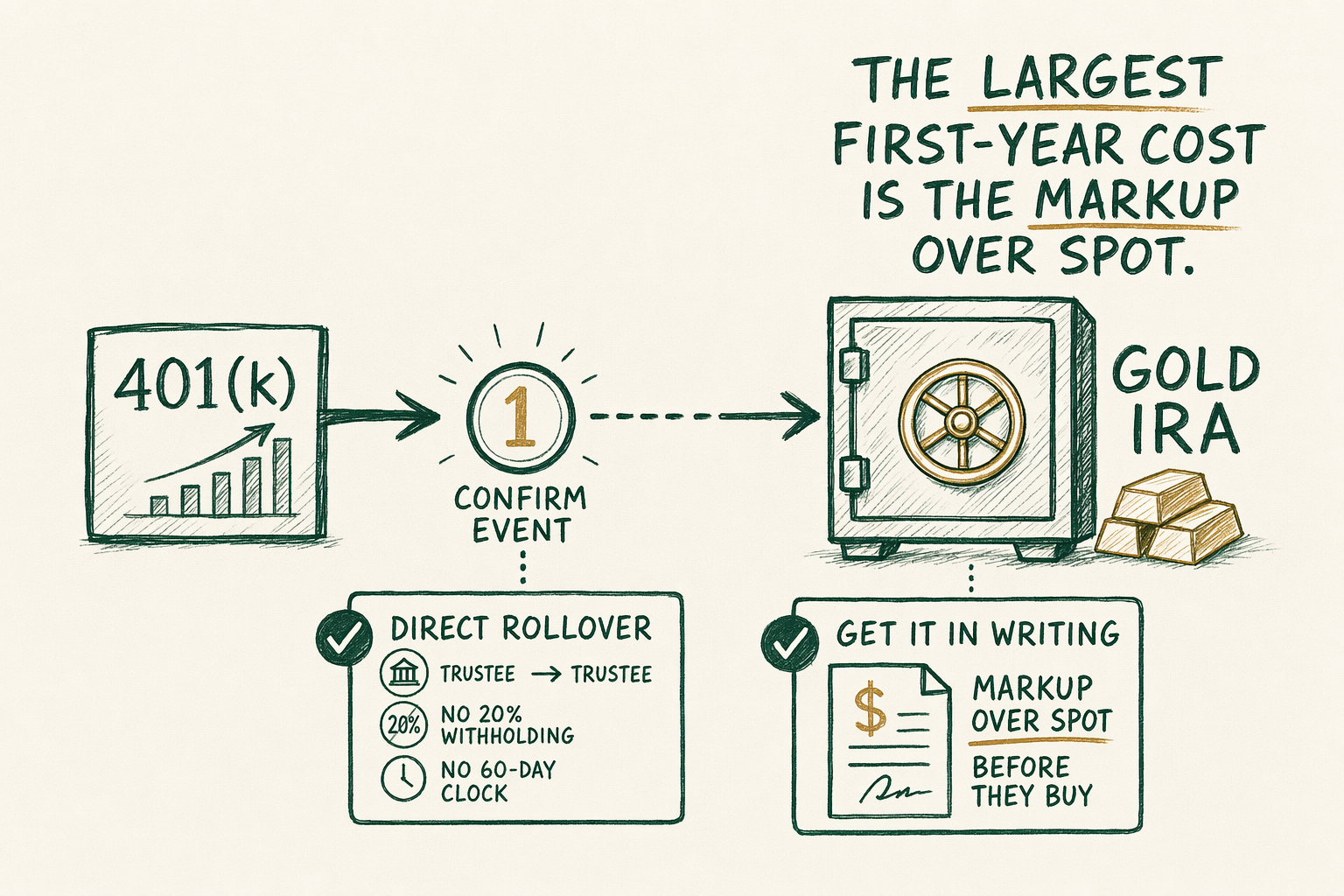

A direct rollover (trustee-to-trustee transfer) is the operationally simpler path. The funds move directly from the current plan's trustee to the new IRA's custodian without passing through your hands. No `20%` withholding applies. No `60`-day clock starts. Form `1099-R` reports the gross distribution with a code indicating a direct rollover, and Form `5498` from the receiving custodian reports the rollover contribution. The two forms reconcile on your tax return; the distribution is reported but not taxed.

The paperwork sequence: open the new Gold IRA at the receiving custodian first (this typically takes `5`-`10` business days from initial application to account-open confirmation). Once the new IRA account is open, the receiving custodian issues a direct-transfer request to the current plan administrator. The current plan administrator processes the transfer (typically `5`-`15` business days, sometimes longer depending on the plan's procedures), and the funds arrive at the new custodian. The receiving custodian then notifies the Gold IRA marketing company that funds are available, the marketing company processes the metal purchase, and the metal is shipped to the IRS-approved depository.

End-to-end timing is typically `2`-`4` weeks for a direct rollover from a cooperative plan administrator. Slower plan administrators can extend the timeline to `6`-`8` weeks. The desk's editorial advice: do not let the receiving Gold IRA company's representative pressure you toward an indirect rollover for the sake of speed — the indirect rollover is faster only by a few days and carries materially more pitfall risk.

Indirect rollover and the 60-day rule

An indirect rollover is the operationally more complex path. The current plan administrator distributes the funds to you (a check made payable to you personally), and you have `60` calendar days from receipt to deposit the funds into the new IRA. If you deposit within the `60` days, the transaction is reported as a rollover and is not taxed. If you miss the window — even by a single day, for almost any reason — the entire amount becomes a taxable distribution, with possible `10%` early-withdrawal penalty if you are under `59½`.

The complication on `401(k)` indirect rollovers is the mandatory `20%` federal withholding. Under IRC `§ 3405`, the plan administrator must withhold `20%` of the gross distribution and remit it to the IRS, even if you intend to roll the full gross amount into the new IRA. To complete a full rollover under indirect mechanics, you must deposit the gross amount in the new IRA — meaning you must come up with the `20%` from another source to deposit alongside the `80%` check from the plan. You then recover the withheld `20%` when you file your taxes the following year.

Example. A `$100,000` `401(k)` balance is rolled over indirectly. The plan administrator distributes `$80,000` to you (after `$20,000` withholding). To complete a full `$100,000` rollover within `60` days, you must come up with `$20,000` from another source to add to the `$80,000` check, depositing the full `$100,000` in the new IRA. The `$20,000` withholding is then recovered as a tax refund when you file your taxes — typically `4`-`16` months later depending on when the rollover occurred relative to your tax filing date. If you only deposit the `$80,000`, the `$20,000` becomes a taxable distribution with possible early-withdrawal penalty. The direct rollover avoids all of this complexity, which is why the desk treats it as the default recommendation.

Timing and likely friction points

Three friction points come up routinely in reader questions. The first is the plan-administrator processing window. Some plan administrators (TIAA, Vanguard, Fidelity, Schwab on retirement plans they administer) move within `5`-`10` business days; others move more slowly, particularly smaller third-party administrators on smaller employer plans. There is no way to materially speed up a slow plan administrator; building in `4`-`6` weeks of timing buffer is the realistic plan.

The second friction point is the receiving Gold IRA company's metal-purchase process. Once the funds arrive at the receiving custodian, the Gold IRA marketing company processes the metal purchase. The purchase price is set on the day of purchase, not on the day the funds left your `401(k)`. If gold has moved during the transit window, you buy at the day-of-purchase price. This is normal and expected; it is not a fault of any party in the chain.

The third friction point is the markup-over-spot question on the receiving side. The dealer's quoted price on the purchase day includes a premium over spot covering fabrication, distribution, and dealer margin. For bullion-grade coins and standard bars the premium is `5%`-`7%`; for specialty proof coins marketed inside the IRA channel the premium can run `12%`-`20%` or higher. Ask the Gold IRA representative for the exact premium on the products being recommended, in writing, before the funds are committed. The premium is the single largest first-year cost and is the line most commonly under-disclosed in marketing material.

Custodian and depository selection

Three roles, three sets of disclosures. The custodian is the IRS-recognized trust company that administers the IRA, files Form `5498` reporting, and handles the in-kind distribution mechanics. The most common custodians in the Gold IRA channel are Equity Trust, STRATA Trust, Kingdom Trust, GoldStar Trust, and IRA Financial. Custodian quality determines reporting accuracy, fee transparency on the custodian side, and account portability if you want to move the account later. Ask the Gold IRA marketing representative which custodian will hold the account before signing.

The depository is the IRS-approved vault that physically holds the metal. Delaware Depository, Brink's Global Services, IDS of Texas, IDS of Delaware, HSBC, and JPMorgan are the largest. The depository's insurance arrangements, audit cadence, and segregation policy all matter; we cover the comparison at `/reviews/storage-vaults/`. The depository on your account is typically set by the custodian's approved list and may be a default choice rather than a freely selected one; ask for the available-depositories list before opening the account.

The Gold IRA marketing company is the entity you spoke to first. The marketing company introduces you to the custodian and depository and earns its commission on the metal sale. The marketing company is not the custodian and not the depository (with rare exceptions). The seven Gold IRA marketing companies covered at `/reviews/gold-ira-companies/` are Augusta Precious Metals, Birch Gold Group, Goldco, American Hartford Gold, Noble Gold Investments, Lear Capital, and Preserve Gold; each has a standalone review with the fee schedule, custodian relationships, and storage partners as of `2026-Q2`.

What can go wrong

Three documented failure modes. First, missing the `60`-day deadline on an indirect rollover. The IRS has very limited discretion to waive this deadline — there are documented private letter rulings granting waivers in cases of clear administrative error or hardship, but they are narrow and the audience cannot count on them. The defense is to never use indirect rollover when direct rollover is available, which is almost always.

Second, signing for specialty proof coins or high-markup numismatic products inside the IRA wrapper without realizing the markup. The IRS rules permit proof coins and certain numismatic items inside an IRA, but the dealer's markup on these products is materially higher than on bullion-grade items. A `$50,000` rollover into a `15%`-markup specialty allocation pays `$7,500` to the dealer in the first transaction. The same `$50,000` into a `5%`-markup bullion-grade allocation pays `$2,500`. The difference is real money. Ask for the markup in writing on every product the representative recommends.

Third, home-storage 'IRA' marketing pitches. Several private LLC structures marketed as 'home storage Gold IRAs' rest on legal theories the IRS has actively challenged. The desk's position, consistent with the published IRS position, is that home storage does not satisfy Section `408(m)` requirements for IRA-eligible custody. Use an IRS-approved depository for IRA holdings, and direct after-tax precious-metals storage decisions to the separate after-tax framework at `/guides/storage-options/`.

Recommended next steps

If you have decided that a Gold IRA rollover is right for your portfolio (a question for your licensed adviser, not for this desk), the operational sequence is: confirm the distributable event status with your plan administrator, choose direct rollover (default) over indirect rollover, choose the receiving Gold IRA company and confirm the custodian and depository, and ask for the markup-over-spot disclosure on the recommended product mix in writing before funding the metal purchase.

For the rollover-mechanics IRS rules in deeper detail, see `/guides/gold-ira-rollover/`. For the Gold IRA company comparison see `/reviews/gold-ira-companies/`. For the depository comparison see `/reviews/storage-vaults/`. For the markup-over-spot and ongoing-fee mechanics see `/guides/gold-ira-fees-explained/`.

For the personalized allocation and tax-sequencing questions, find a CPA and a licensed financial adviser. The desk's role is to point at the questions worth asking; the licensed professionals deliver the personalized answer for your specific tax position, time horizon, and overall portfolio composition.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Can I roll over my current employer's 401(k)?

Only if you have a 'distributable event' — typically separation from the employer, reaching age 59½, or an in-service withdrawal provision if your plan allows it. -

Should I do a direct or indirect rollover?

Direct (trustee-to-trustee) is operationally simpler and avoids the 60-day deadline. Indirect requires you to receive a check and deposit it within 60 days, with withholding considerations. Direct is the editorial default unless you have a specific reason otherwise. -

Where do I go next?

Start with the linked topic hub for a deeper foundation, then the comparison page that matches your selection criteria. Every claim about a company carries a snapshot date — confirm current arrangements before committing. -

Is this personalized advice?

No. BullionLens publishes editorial coverage, not personalized investment advice. Use this material to understand the landscape, then consult a licensed adviser for your specific situation.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.