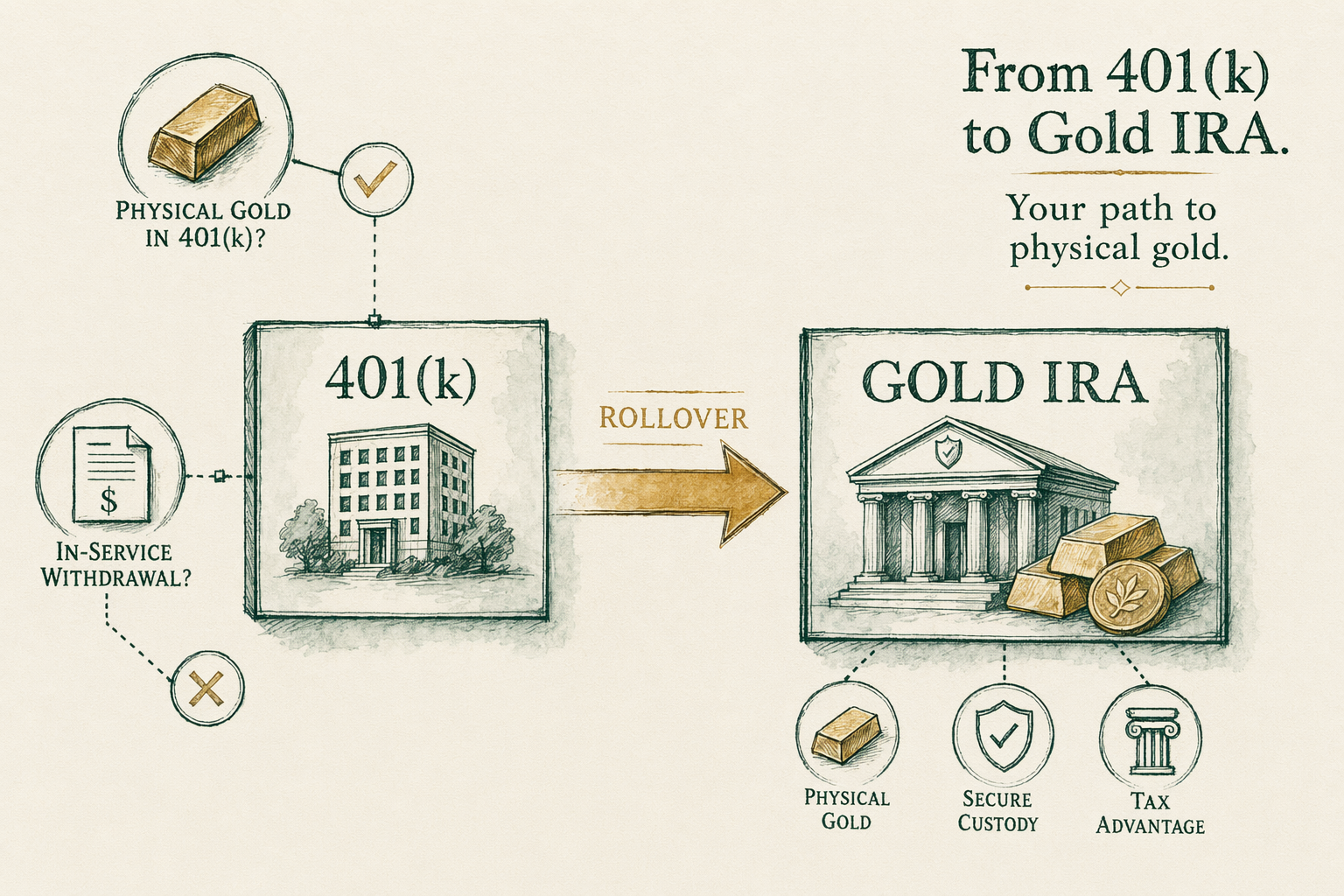

Can I buy gold with my 401(k)?

Whether you can hold physical gold in a 401(k), the in-service withdrawal option, and the rollover path to a self-directed Gold IRA.

Gold ETFs inside 401(k)s

The most accessible gold exposure inside a typical `401(k)` is a gold-backed exchange-traded fund. Major US-listed options include SPDR Gold Shares (`GLD`), iShares Gold Trust (`IAU`), abrdn Physical Gold Shares (`SGOL`), GraniteShares Gold Trust (`BAR`), and VanEck Merk Gold Trust (`OUNZ`). Each ETF holds physical gold in a London-vaulted institutional structure; ETF shares represent fractional claims on the pooled metal. Expense ratios vary roughly `0.10%-0.40%` annually; the structure is liquid intraday and held in normal brokerage form.

A gold ETF inside a `401(k)` is not the same as owning physical metal. ETF shareholders do not have a claim on specific bars; they have a pro-rata interest in a pool. The fund's prospectus governs trustee responsibilities, custodian arrangements, and the conditions under which physical delivery is possible (most ETFs allow physical redemption only at the institutional-creation-unit level, which means individual investors cannot take delivery). For investors whose thesis is monetary-debasement hedging or institutional-trust hedging, ETF exposure is a partial substitute; for investors specifically wanting physical possession outside the institutional system, ETFs are not what they're looking for.

In-service withdrawal provisions

Most `401(k)` plans restrict participant withdrawals while the participant is still employed. Some plans allow 'in-service withdrawals' — distributions taken while still employed and still contributing — under specific conditions. Common in-service withdrawal triggers include reaching age `59½` (most plans), reaching the plan's normal retirement age (varies), specific hardship qualifications under IRS rules, or rollover of employer matching contributions after a vesting period (rare).

If your plan allows in-service withdrawals, you can typically roll the eligible portion to a self-directed IRA, including a Gold IRA, while continuing to work and contribute to the `401(k)`. This is the most common path for a `60-year-old` who wants Gold IRA exposure without leaving the employer. Confirm with your specific plan administrator: 'Does my plan permit in-service rollovers, and what age/condition triggers them?' The answer varies plan-by-plan even at the same recordkeeper. The plan's Summary Plan Description (SPD) is the authoritative document.

Rollover at job change

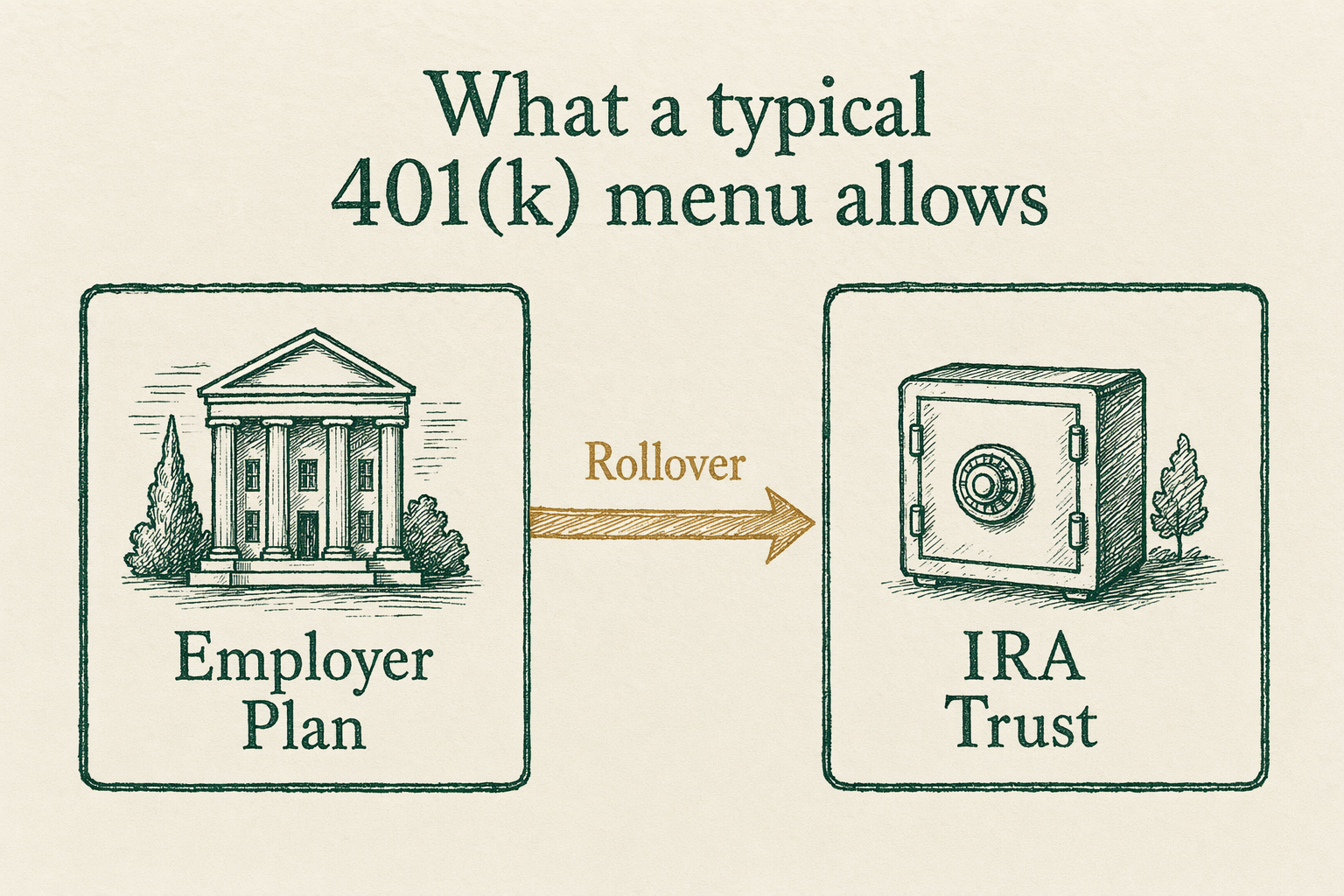

Separation from the employer (job change, retirement, layoff) is the most common trigger for `401(k)` distributability. When you separate, your former `401(k)` becomes eligible for rollover into an IRA — including a self-directed IRA holding physical gold. The mechanics: instruct the former-employer plan to perform a direct trustee-to-trustee rollover to your new Gold IRA custodian (Equity Trust, STRATA Trust, or another). Direct rollovers are not taxable events and do not count against the IRS one-rollover-per-12-months limit on indirect rollovers.

The paperwork involves Form `1099-R` from the distributing plan reporting the gross distribution (with distribution code `G` for direct rollover, meaning non-taxable), and Form `5498` from the receiving IRA custodian reporting the rollover contribution. Both forms must reconcile on the participant's tax return. Indirect rollovers (where the participant receives the funds personally and then deposits to the IRA within `60` days) carry the `60`-day rule, mandatory `20%` federal withholding by the distributing plan, and reporting complications — direct rollover is the cleaner path.

Self-directed 401(k) plans

Self-directed `401(k)` plans (sometimes called 'solo 401(k)s' for owner-only businesses, or 'self-directed plans' more generally) operate under a different administrative framework than employer 401(k)s. They allow the plan participant to invest in a broader set of assets including, in certain configurations, physical precious metals held at IRS-approved depositories under bailment with the plan.

Self-directed `401(k)` configurations are not the standard employer-plan template; they require a plan administrator that supports the broader-asset-class structure (Equity Trust, STRATA Trust, IRA Financial, Solo 401k Plans, and others offer them). For solo business owners (self-employed, single-member LLCs, sole proprietors), a self-directed solo `401(k)` can be a meaningful vehicle for holding gold within a tax-deferred retirement structure. For W-2 employees of larger companies, self-directed `401(k)`s are typically not available — the employer-sponsored plan determines the menu, and physical gold is not on it. The right path for most W-2 employees who want Gold IRA exposure remains a rollover at separation (or in-service rollover if the plan permits) into a self-directed Gold IRA.

Real-world example — a 58-year-old's three options

Consider a `58-year-old` participant in a large-employer `401(k)` with `$400,000` in plan assets, wanting some gold exposure. Option `1`: Allocate `5%` of the `401(k)` to a gold ETF inside the plan's SDBA, assuming the plan offers SDBA access. The participant holds `~$20,000` of `IAU` shares; total cost is the ETF's expense ratio (about `0.25%` annually = `$50/yr`) plus any SDBA-feature fee. No physical bullion involved.

Option `2`: At age `59½` (eighteen months away), the participant rolls a portion of the `401(k)` to a self-directed Gold IRA under the plan's in-service rollover provisions, if available. The Gold IRA holds physical bullion at Delaware Depository under Equity Trust custodianship. First-year costs run roughly `$50` setup + `$80` annual maintenance + `$100` storage + `5-8%` markup over spot on the bullion. Option `3`: The participant waits until job change or retirement to roll the full `401(k)`. All three options have tradeoffs; choice depends on plan provisions, the participant's preference for ETF versus physical exposure, and the timing of any anticipated separation. BullionLens does not recommend among them; a licensed adviser knows the participant's full picture.

Common misconceptions about 401(k) gold access

**'I can buy gold bars inside my employer 401(k).'** Almost never. Standard employer plans do not hold physical bullion. A self-directed IRA (via rollover at separation or in-service rollover) is the typical path to physical gold in a retirement wrapper.

**'Gold ETFs are the same as owning physical gold.'** No. ETFs are pooled-claim structures held by institutional custodians. Shareholders cannot take delivery (except at institutional creation-unit scale). The exposure is to gold price; the legal claim is to the fund.

**'I can do a 60-day rollover and pay no tax.'** Indirect rollovers carry the `60`-day rule, mandatory `20%` federal withholding by the distributing plan, and a one-per-12-months limit. A direct trustee-to-trustee rollover avoids withholding and counting limits. Use direct rollover whenever possible.

What this means for you

For most `W-2` employees with standard employer `401(k)` plans, the answer is: not directly. You cannot buy physical gold bars inside a typical `401(k)`. You can hold a gold ETF if your plan offers SDBA access; you can roll over (in-service or at separation) into a self-directed Gold IRA holding physical bullion. For self-employed individuals, a self-directed solo `401(k)` can hold physical gold under the right administrative setup. The right structure depends on your employment status, your specific plan's provisions, your age, and your preference for ETF versus physical exposure. As always, BullionLens does not provide personalized advice; consult a licensed adviser before initiating a rollover or changing retirement-account structure.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Can I hold physical gold inside a standard 401(k)?

Almost never. Standard employer 401(k) plans offer a menu of mutual funds; physical bullion is not on the menu. To hold physical gold in a retirement structure you typically need to roll funds into a self-directed Gold IRA. -

Can I roll over my current 401(k) while still employed?

Only if your plan permits 'in-service withdrawals' — a provision that varies by employer. Reaching age 59½ also unlocks rollovers under most plans. Separation from the employer is the most common trigger. -

Are gold ETFs a substitute?

Gold ETFs (GLD, IAU, SGOL, BAR, OUNZ) give you exposure to spot gold via a fund. They are not the same as owning physical metal — you do not have a claim on specific bars and you cannot take delivery from most of these structures. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.