Gold for self-directed IRA holders

Editorial guide for self-directed IRA holders adding physical gold: custodian selection, prohibited-transaction rules, and the practical opening sequence.

If you already have a self-directed IRA

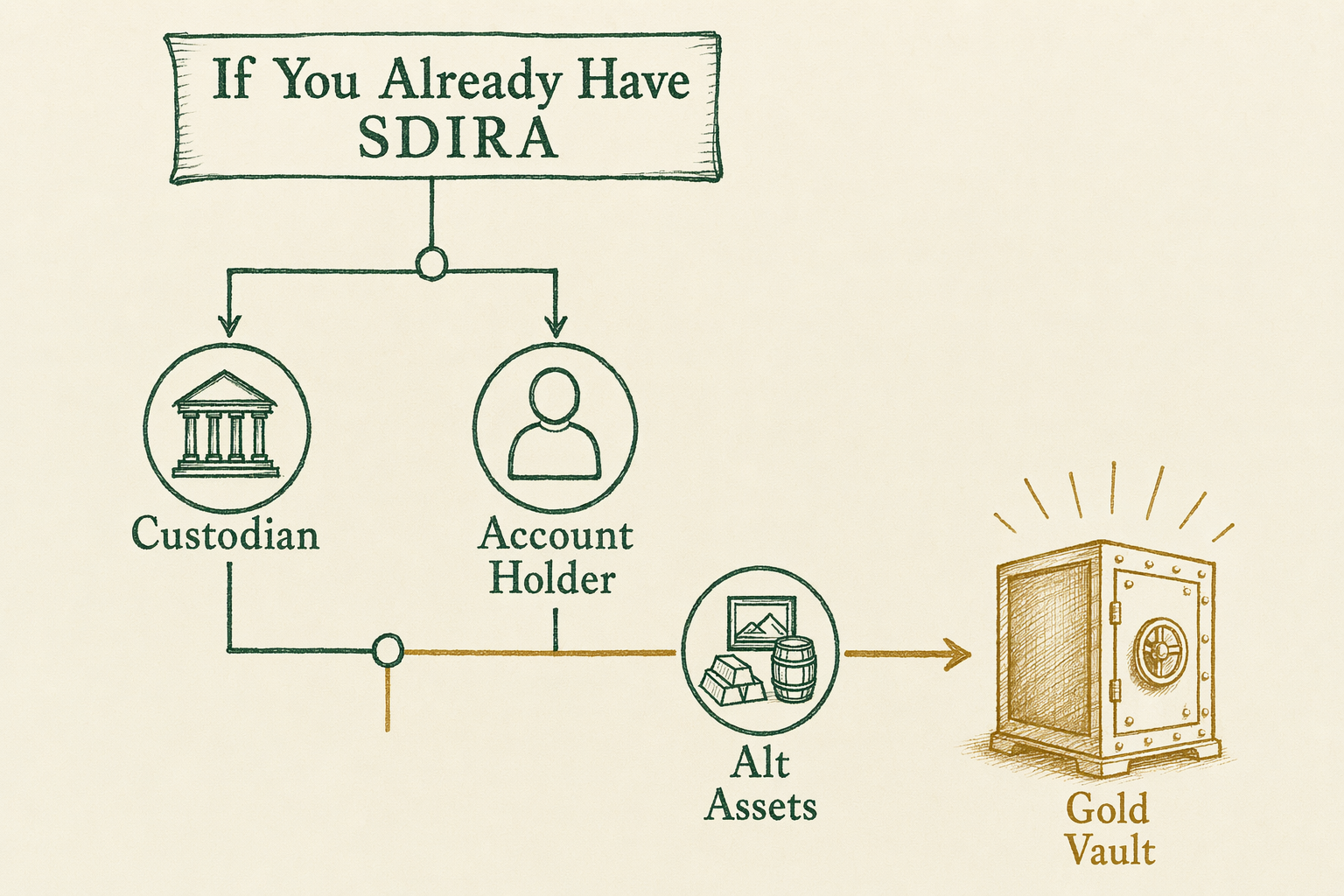

If you already hold a self-directed IRA — for real estate, private placements, precious metals, or any of the other non-traditional asset categories the SDIRA structure permits — and you are considering adding physical gold to the account, the editorial picture is different than it is for a first-time Gold IRA buyer. You already know the custodian landscape. You already have at least one IRS-recognized trust company managing an SDIRA on your behalf. The question is operational: does your current custodian support physical metals, and if not, is the move to a metals-capable custodian worth the operational overhead, or is opening a new SDIRA at a metals-capable custodian the cleaner path.

This guide is shorter than the equivalent guide for a first-time Gold IRA holder because the SDIRA holder already understands the prohibited-transaction framework, the disqualified-person rules, and the annual reporting mechanics. What this guide adds is the metals-specific layer: which SDIRA custodians support physical metals, the documentation those custodians require, the depository selection mechanics, and the prohibited-transaction edge cases specific to physical-metals holdings.

What this guide covers

Five sections. First, the scope of what a self-directed IRA permits in the precious-metals category under IRS rules (specifically, IRC `408(m)(3)`): which gold, silver, platinum, and palladium products are IRA-eligible, what fineness standards apply, and what the IRS treatment is on non-eligible items. Second, custodian selection specifically for physical-metals holdings: which SDIRA custodians support metals (most do, but the documentation depth varies), and what the fee schedule typically looks like at the custodian-level versus the gold-marketing-company channel.

Third, prohibited-transaction rules under IRC `4975` as they apply to physical metals, including the disqualified-person edge cases and the home-storage compliance issue. Fourth, the practical opening sequence for adding metals to an existing SDIRA — what documentation to gather, what timing to expect, and where the friction points are. Fifth, annual compliance and reporting: Form `5498` and how it handles metals valuations, the year-end depository statement, and the documentation to retain.

Each section ends with the relevant CPA or licensed-professional pointer for personalized questions.

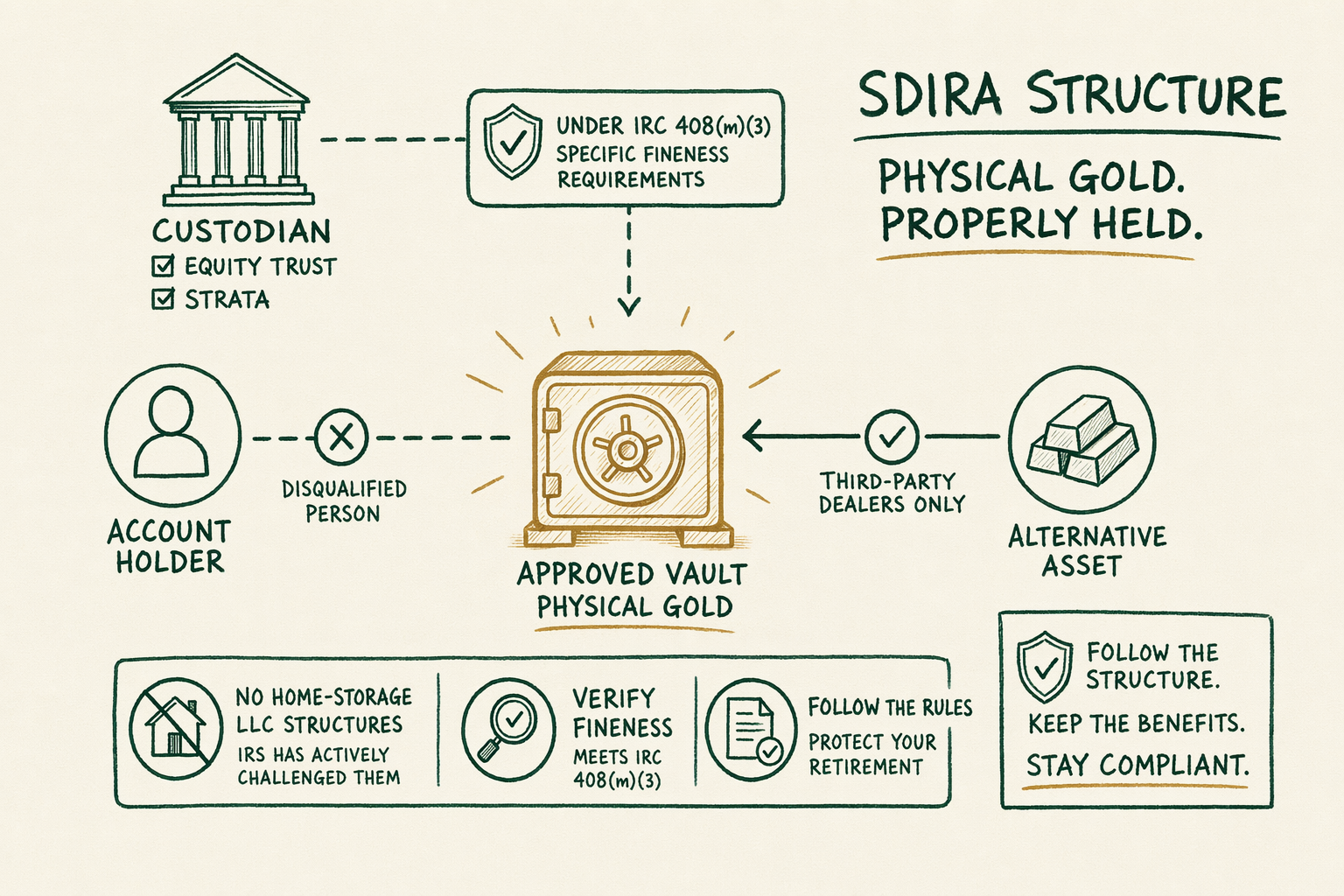

What a self-directed IRA permits

Self-directed IRAs permit a broader asset universe than traditional brokerage IRAs: real estate, private placements, certain private debt instruments, certain LLC interests, and (the topic of this guide) physical precious metals. The structural constraint is IRC `408(m)`, which limits IRAs from holding 'collectibles' — but Section `408(m)(3)` carves out specific precious-metals products from the collectible-prohibition rule.

The IRA-eligible precious-metals products under `408(m)(3)`: gold, silver, platinum, and palladium coins and bars meeting specified fineness standards. For gold the standard is `99.5%` minimum fineness; for silver `99.9%`; for platinum and palladium `99.95%`. Specific named coins are eligible regardless of fineness — American Gold Eagles (the only major exception, eligible despite being below `99.5%`), American Gold Buffalos, Canadian Maple Leafs, Krugerrands (older issues excluded; current `99.99%` issues eligible), Austrian Philharmonics, and others on the IRS-published list. Bars must be produced by an LBMA-recognized refiner.

Numismatic and collectible coins are NOT IRA-eligible. The market sometimes sees Gold IRA marketing material that pushes specialty proof coins or numismatic items inside the IRA wrapper; those products are eligible only if they meet the specific carve-outs of `408(m)(3)`. The desk's editorial position, consistent with the IRS position, is to verify eligibility against the IRS list before any specific item enters the account. Consult IRS Publication `590-A` and your custodian's published IRA-eligibility list.

Custodian selection for physical metals

Most major SDIRA custodians support physical precious metals. Equity Trust, STRATA Trust, Kingdom Trust, GoldStar Trust, Madison Trust, IRA Financial, and Mainstar Trust all have documented precious-metals programs with depository relationships. The depth of documentation, the depository options, and the fee schedule vary materially.

On fees, the custodian-level fee schedule typically includes an annual administration fee (`$80`-`$250/yr`), a transaction fee on each metal purchase or sale (`$30`-`$60` per transaction, sometimes folded into an annual flat fee), and a storage fee passed through from the depository (`$75`-`$300/yr` depending on tier). The Gold IRA marketing channel adds a markup over spot on the metal purchase (`5%`-`15%` depending on product mix and dealer), which is separate from the custodian's fees and is the largest dollar line item for most first-purchase setups.

If you already have an SDIRA with a non-metals-capable custodian (or one that supports metals only with limited documentation depth), the two paths are: open a new SDIRA at a metals-capable custodian and fund via direct transfer, or initiate the metals add-on at the current custodian if the custodian's documentation depth is sufficient for the holding size and configuration you want. The first path is operationally cleaner; the second avoids the second-custodian complexity. Both work. The choice depends on the specific custodian relationships and the documentation depth you need.

Prohibited-transaction rules

Under IRC `4975`, certain transactions between an IRA and a 'disqualified person' are prohibited and trigger disqualification of the IRA (with severe tax consequences). Disqualified persons include the IRA holder, the holder's spouse, ancestors, lineal descendants and their spouses, and certain related entities. The classic prohibited transaction examples involve real-estate SDIRAs (the IRA cannot buy a property the holder already owns, cannot rent property to the holder's family, etc.).

On physical-metals SDIRAs, the analogous edge cases are: the IRA cannot purchase metals from the holder's existing personal collection (the holder is a disqualified person and the sale would be a prohibited transaction), the IRA cannot lend metals to the holder or family (also a prohibited transaction), and the IRA cannot use metals as collateral for a personal loan to the holder. Verify the metals supply chain — purchases must be from third-party dealers, not from the holder's existing inventory.

The home-storage compliance issue is a different category of risk. Several private LLC structures marketed as 'home storage Gold IRAs' rest on a legal theory in which the IRA holds an LLC that owns the metals, and the LLC manager (the IRA holder) takes possession at home. The IRS has consistently challenged this structure, taking the position that personal possession of IRA assets constitutes a prohibited transaction and triggers full distribution of the IRA at fair market value (with possible early-withdrawal penalty if under `59½` and possible accuracy-related penalties on top). The desk's position, consistent with the IRS position and the case law (notably McNulty v. Commissioner, `155 T.C. No. 11`, `2021`), is that home-storage Gold IRA structures should be treated as IRS-flagged territory. Use an IRS-approved depository.

Opening sequence (or asset-addition sequence)

If you are opening a new SDIRA at a metals-capable custodian: complete the new-account application (typically `5`-`10` business days from submission to account-open confirmation), initiate a direct transfer from the existing IRA (`5`-`15` business days at the sending custodian), and once funds are confirmed at the new custodian, place the metal-purchase order through the dealer channel. End-to-end timing is typically `3`-`5` weeks. The dealer's purchase price is set on the day of purchase, not on the day funds left the prior custodian.

If you are adding metals to an existing SDIRA at a metals-capable custodian: the asset-addition sequence is shorter. Confirm with the custodian that physical metals are supported on the existing account configuration (some custodians require a separate account type for metals; others allow metals within an existing self-directed structure). Identify the depository options through the custodian's published list, confirm the dealer relationship (some custodians have preferred dealer partners; others permit any compliant dealer), and place the purchase order through the dealer.

Documentation needed: the new-purchase invoice from the dealer (showing the specific items, weights, finenesses, and prices), the custodian's transaction-instruction form (signed by the IRA holder, authorizing the purchase), the depository's incoming-receipt confirmation (acknowledging the metal entering the IRA holder's allocated registration), and the standard year-end statements thereafter.

Annual compliance and reporting

Form `5498` from the custodian reports the year-end fair market value of the IRA to the IRS. On a physical-metals holding the FMV is the depository's published valuation as of `December 31`, typically the depository's bid for the specific items held or a spot-reference applied to the relevant weight. Form `5498` arrives at the IRA holder by `May 31` of the following year and is informational — the IRA holder does not file it; the custodian files it with the IRS directly. The holder retains the form for records and reconciles against personal records of contributions, rollovers, and prior-year balances.

Distributions from the SDIRA — including in-kind metal distributions and cash distributions — are reported on Form `1099-R` from the custodian, sent to the IRA holder by `January 31` of the following year. The 1099-R reports the gross distribution at fair market value with the relevant distribution code. The IRA holder reports the distribution on Form `1040` with the appropriate taxation treatment (typically ordinary income for Traditional IRA distributions, none for qualified Roth distributions, with possible `10%` early-withdrawal penalty if under `59½` and no exception applies).

Annual valuation discrepancies can occur on physical-metals SDIRAs because the depository's bid-side valuation may differ materially from the LBMA spot reference or other public benchmarks. If your custodian's `Form 5498` valuation looks materially off, query the custodian for the basis (specific item bid prices, spot reference used, applicable spreads). The valuation drives RMD calculations once the holder reaches age `73` under SECURE 2.0; accurate valuation matters.

Recommended next steps

For the foundational mechanics of how a Gold IRA rollover works at the IRS rule level, see `/guides/gold-ira-rollover/`. For the company-side comparison of Gold IRA marketing companies that work with SDIRA custodians, see `/reviews/gold-ira-companies/`. For the depository-side comparison see `/reviews/storage-vaults/`. For the prohibited-transaction and disqualified-person details specific to SDIRAs, see `/learn/what-is-a-disqualified-person-in-an-ira/`.

For the personalized tax and compliance side, work with a CPA experienced in self-directed IRA reporting and (if the SDIRA holds multiple asset categories) the unrelated business income tax (UBIT) and unrelated debt-financed income (UDFI) edge cases that can apply to leveraged real-estate holdings. Pure precious-metals SDIRA holdings rarely trigger UBIT, but the CPA who handles the broader account configuration is the right point of contact for any specific question.

For the editorial standards and disclosure policies, see `/editorial-standards/`. Each company review carries a `2026-Q2` snapshot date; confirm current arrangements before committing.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Can I add gold to an existing self-directed IRA?

Often yes, if your current SDIRA custodian supports precious metals. If not, a transfer to a custodian that does is straightforward. -

What are the biggest pitfalls?

Prohibited transactions (especially purchases from disqualified persons) and home-storage compliance issues. Both are well-documented in IRS guidance and case law. -

Where do I go next?

Start with the linked topic hub for a deeper foundation, then the comparison page that matches your selection criteria. Every claim about a company carries a snapshot date — confirm current arrangements before committing. -

Is this personalized advice?

No. BullionLens publishes editorial coverage, not personalized investment advice. Use this material to understand the landscape, then consult a licensed adviser for your specific situation.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.