Can I take physical possession of Gold IRA gold?

The IRS rules on taking distribution of physical gold from a Gold IRA: in-kind distributions, tax treatment, and home storage compliance issues.

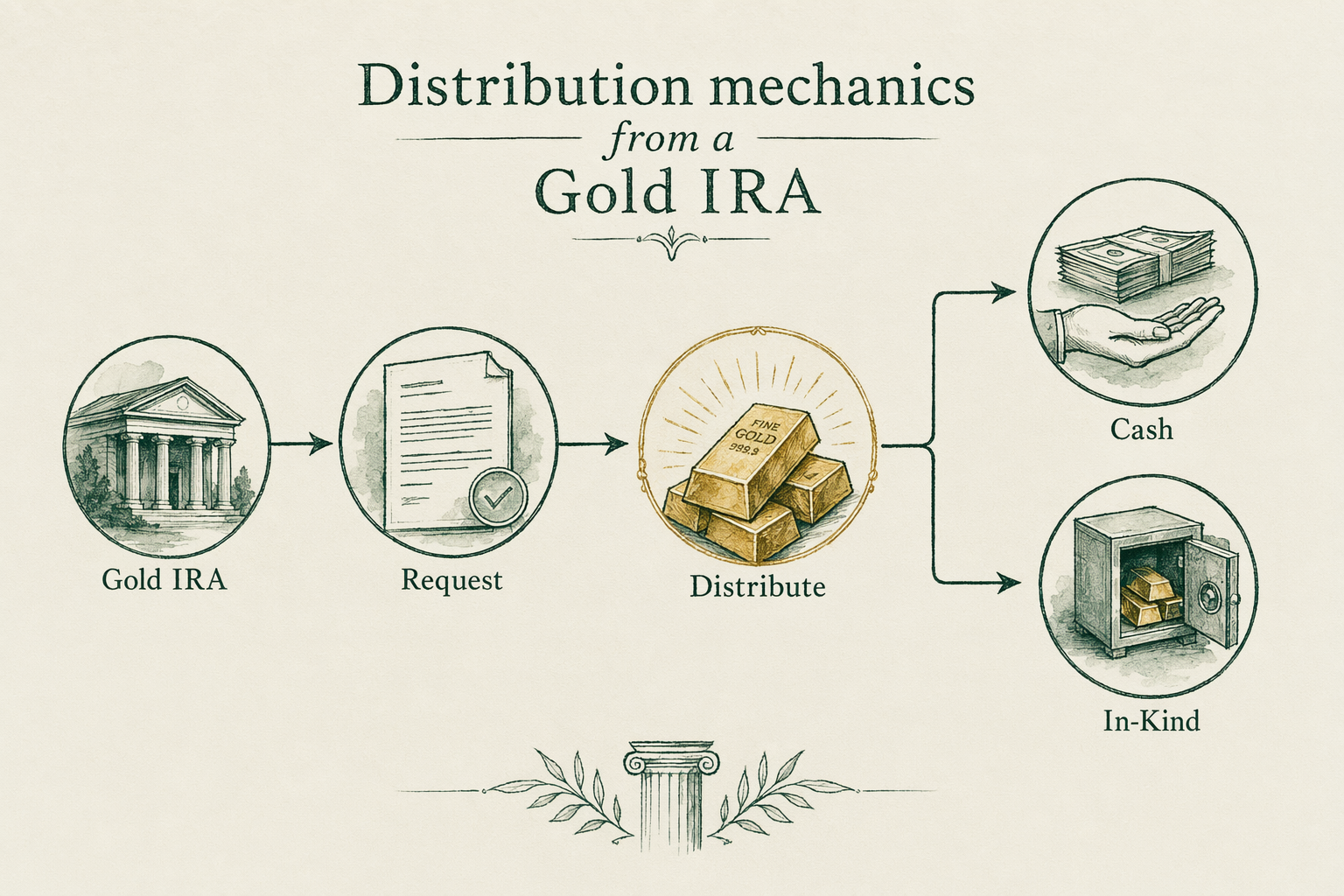

Distribution mechanics from a Gold IRA

A Gold IRA distribution is a tax event. You can take it in two forms — cash (the custodian sells metal at the depository, proceeds paid to you) or in-kind (the custodian arranges for physical bullion to be released from the depository to you). Either form is a distribution; either form is taxable.

The mechanical sequence for an in-kind distribution: (1) account holder instructs the custodian (Equity Trust, STRATA, etc.) of intent to take an in-kind distribution; (2) custodian issues instructions to the depository (Delaware Depository, Brink's, IDS of Texas); (3) depository releases the specified bullion via insured shipment (typically Brink's secure ground or air, USPS Registered Mail for smaller values); (4) account holder receives the physical metal; (5) custodian issues Form 1099-R reporting the fair market value of the released metal as a distribution; (6) account holder includes the fair market value as ordinary income on Form 1040 for the distribution year.

Fees apply: secure-shipment fees typically `$100-$500` depending on value and security tier; the custodian's standard distribution-processing fee. Account holders under age `59½` also face the `10%` early-withdrawal penalty under IRC § 72(t) unless an exception applies.

In-kind vs cash distribution

**Cash distribution**: Operationally simpler. The custodian sells the specified metal at the depository (typically into the wholesale bullion market or to a participating dealer), the proceeds are wired to the account holder, and the dollar amount is reported as the distribution. The taxable amount is the net cash received.

**In-kind distribution**: Operationally more involved. The metal is shipped to the account holder. The taxable amount is the fair market value of the metal at the date of distribution — typically the LBMA fix on that date applied to the troy ounces released. The metal becomes the holder's personal property with a cost basis equal to the in-kind distribution value.

**Why choose in-kind over cash**: The most common reason is to retain physical-gold exposure outside the IRA wrapper. Holders approaching `73` who want to preserve their gold position rather than convert to cash can take in-kind RMDs each year, building a non-IRA bullion holding while satisfying the RMD requirement. The metal is then personally owned and can be stored at home, at a bank safe deposit box, at a private vault, or sold individually.

Tax treatment of in-kind distributions

**Traditional Gold IRA**: The fair market value at the date of distribution is taxed as ordinary income on the account holder's Form 1040 for the year. The custodian reports the distribution on Form 1099-R. If the holder is under `59½`, the `10%` early-withdrawal penalty under IRC § 72(t) applies on top of the ordinary income tax unless an exception qualifies. The metal received takes a cost basis equal to the distribution fair market value — no built-in capital gain at the distribution event itself.

**Roth Gold IRA qualified distribution**: Tax-free under IRS rules if the Roth account has been open at least 5 tax years and the holder is at least `59½`, has a disability, or qualifies under another IRC § 408A exception. The metal received takes a cost basis equal to the distribution fair market value.

**Subsequent sale of distributed metal**: The metal is now personal-property bullion. A subsequent sale produces a capital gain or loss measured from the in-kind distribution cost basis. Long-term gains (held >1 year) are taxed at the collectibles rate under IRC § 408(m)(3), currently capped at `28%`. Short-term gains are taxed at ordinary income rates.

The two-step sequence — distribution at ordinary income tax, then sale at collectibles capital gains — is the standard tax structure for the in-kind option. Neither step is avoidable; both are predictable.

Home storage of IRA-distributed gold

Once metal has been distributed from the IRA via the in-kind mechanism, it is personal-property bullion subject to no special IRS storage rule. You can store it at home, at a bank safe deposit box, at a private vault — wherever you choose, subject to your own insurance and security considerations.

Home-storage best practices for distributed bullion: a quality home safe with appropriate fire and theft ratings (a UL-rated TL-15 or TL-30 safe is the typical recommendation for substantial bullion holdings); insurance via a scheduled-bullion rider on a homeowner's policy (standard homeowner's policies typically have a `$5,000-$10,000` bullion sub-limit); documented inventory with photos and serial numbers maintained separately from the metal itself.

The home-storage option for distributed gold is structurally fine. It is the home-storage option for IRA-wrapped gold (covered next) that is the IRS issue.

The home-storage Gold IRA controversy

Some marketing materials promote a "home-storage Gold IRA" or "checkbook IRA LLC" structure in which the IRA owns an LLC, the LLC owns gold, and the IRA holder controls the LLC and physically stores the gold at home. The pitch is that the bullion remains IRA-wrapped (tax-deferred) while the holder retains personal possession.

The IRS has consistently taken the position that this structure does not satisfy the requirements of IRC § 408(m) and IRC § 408(n). IRC § 408(n) requires IRA precious metals to be held by an IRS-approved non-bank trustee — the IRS has interpreted this as excluding the IRA holder personally as the storage party, even via an LLC structure.

The McNulty v. Commissioner case (2021, Tax Court) directly addressed this issue and ruled against the taxpayers. The court held that the IRA holder's personal possession of IRA-purchased gold coins — even via an intermediate LLC owned by the IRA — was a deemed distribution of the IRA. The ruling cost the McNulty taxpayers a substantial tax liability and is now a precedent on the home-storage Gold IRA question.

Practical guidance: do not use the home-storage Gold IRA structure. The IRS has won the cases that test the structure; the legal risk is meaningfully greater than the tax-deferral benefit. If you want physical possession of gold, take an in-kind distribution at the appropriate age, pay the ordinary-income tax, and store the post-distribution metal at home or wherever you prefer. If you want IRA-wrapped tax deferral, use an IRS-approved depository — Delaware, Brink's, IDS — for the storage.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Can I take my Gold IRA gold home?

Yes — by taking a distribution. The fair market value of the metal at the date of distribution is taxed as ordinary income (Traditional IRA) and may trigger a 10% penalty if you are under 59½. -

What about 'home-storage Gold IRAs'?

The IRS has consistently taken the position that home-storage Gold IRAs do not satisfy IRC Section 408(m) requirements. Multiple court cases have backed the IRS position. Avoid this structure. -

Can I store gold I bought outside an IRA at home?

Yes. After-tax physical gold has no IRS storage rule — you can store it wherever you like, subject to your own insurance and security choices. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.