Gold storage options — the editorial guide

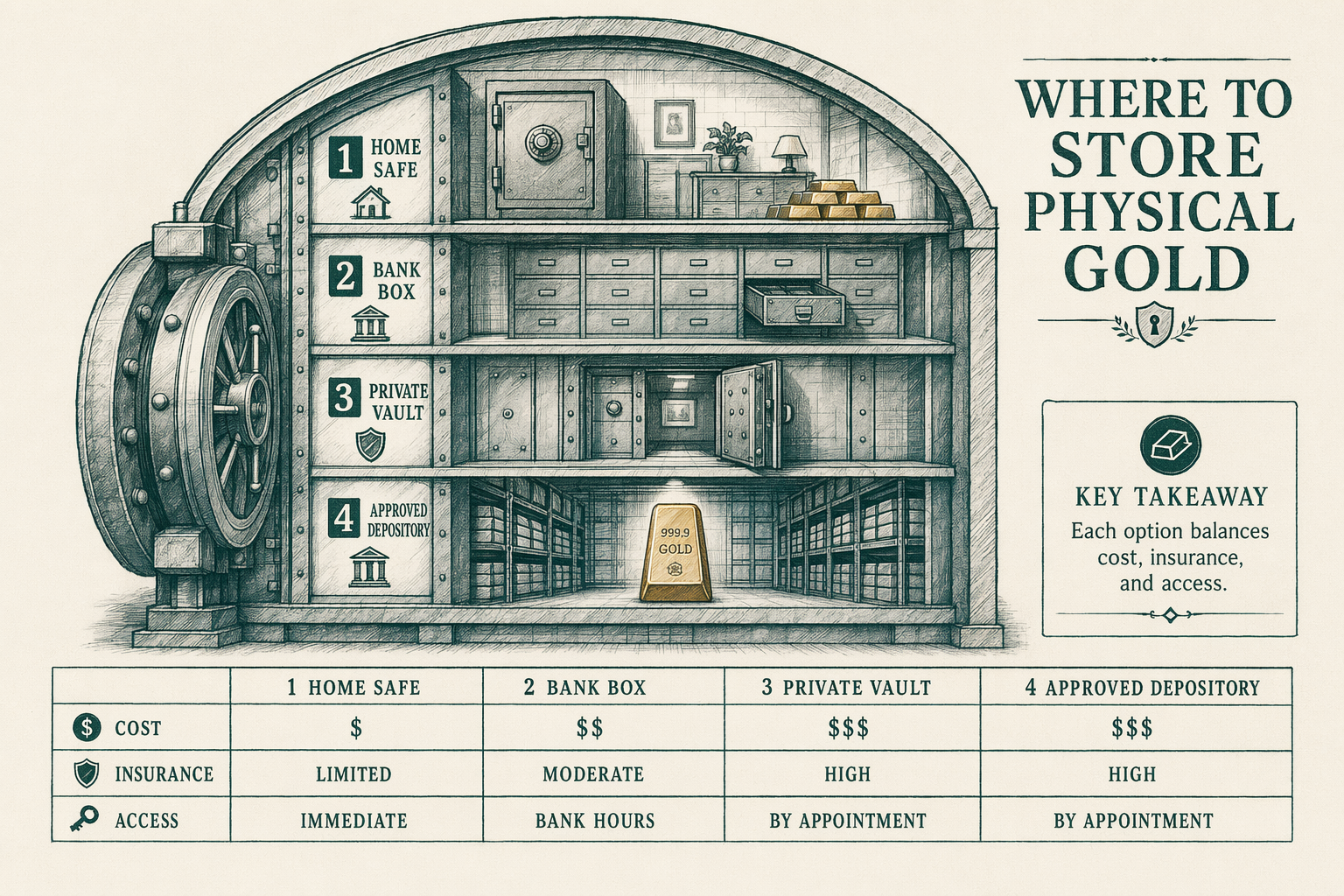

Where to store physical gold: home safe, bank safe-deposit box, private vault, IRS-approved depository. Costs, insurance, and access tradeoffs.

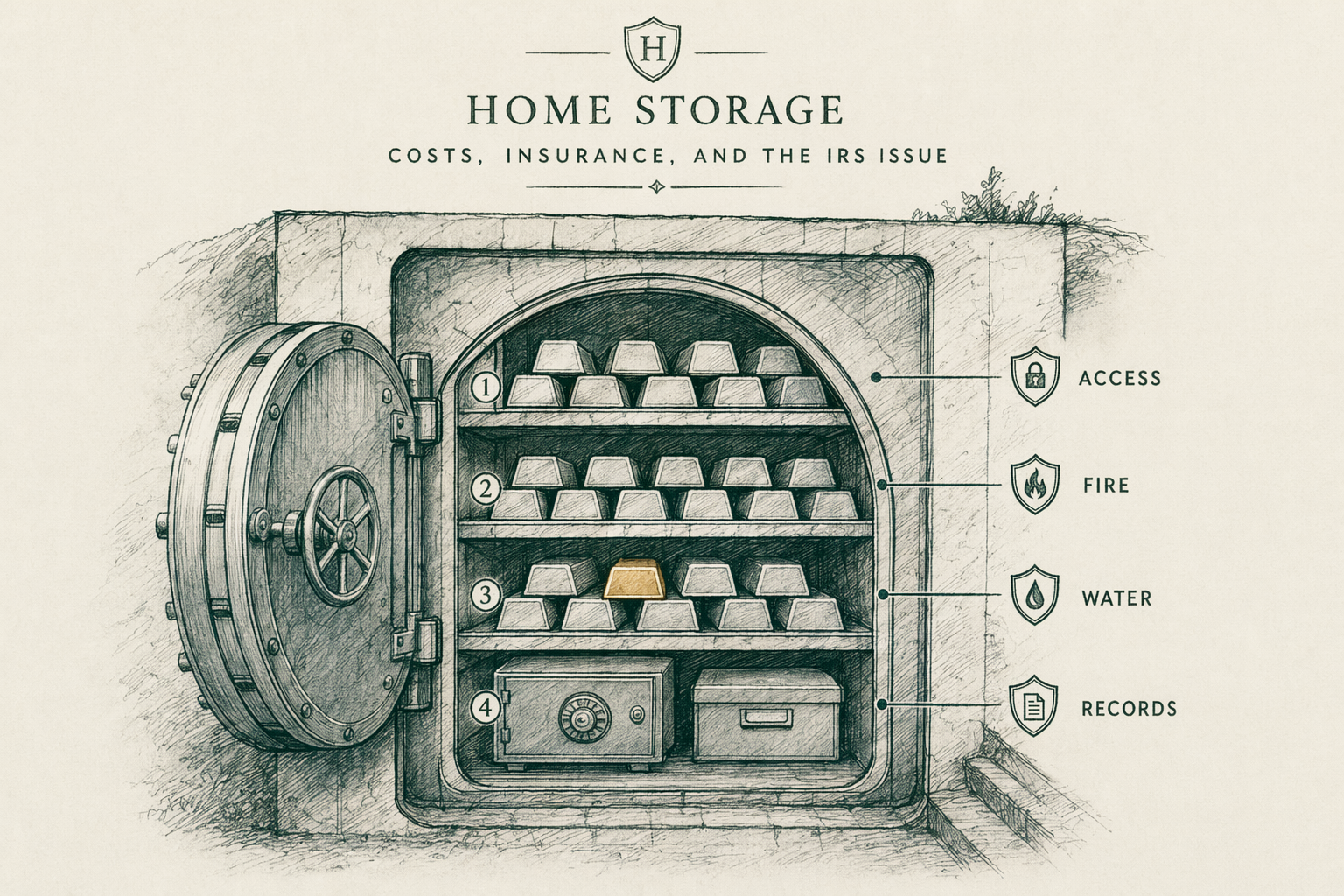

Home storage — costs, insurance, and the IRS issue

For after-tax bullion holdings (not inside an IRA wrapper), home storage is operationally legal and is what many buyers do. The relevant questions are physical security, insurance coverage, and the practical access-vs-security tradeoff.

Physical security at home typically means a fire-and-theft-rated safe. A residential safe rated TL-15 or TL-30 (the UL ratings indicating resistance to common safe-cracking techniques for `15` or `30` minutes against specific tooling), bolted to the slab through the floor or to a wall structural member, costs `$1,500` to `$5,000` depending on size and rating. Lower-grade safes (TL-only without fire rating, or fire-only without security rating) cost less but provide correspondingly less protection.

Insurance coverage at home is where most buyers underestimate the risk. Standard homeowner's insurance policies typically cap coverage on unscheduled valuables (the catch-all category covering jewelry, coins, bullion, watches, art) at `$200` to `$2,500`. That cap is per-occurrence — meaning the policy will pay up to the cap in the event of a theft or fire loss, but no more, regardless of the actual value of the bullion lost.

Scheduled valuables coverage (a named-item rider) is required for meaningful coverage of bullion above the unscheduled cap. The rider typically adds `$1` to `$3` per `$1,000` of insured value annually, with the insured value usually capped at a specified amount per item and per policy. Many insurers exclude bullion entirely from scheduled-valuables riders — confirm in writing with the specific insurance carrier before relying on coverage. For meaningful retail holdings (`$50,000` and above) the bullion-exclusion is common enough that home storage typically operates on a self-insurance basis.

For Gold IRA holdings the home-storage question is settled by IRS guidance. The IRS has consistently taken the position that home-storage Gold IRAs do not satisfy Section 408(m) requirements; the IRS treats home-stored Gold IRA bullion as a distribution event, triggering immediate income tax on the distributed amount and a possible `10%` early-withdrawal penalty if the holder is under `59½`. Use an IRS-approved depository for IRA holdings; home storage is a separate decision for after-tax holdings only.

Bank safe-deposit boxes — what they cover and do not

Bank safe-deposit boxes are a common retail-bullion storage choice with two structural caveats that buyers consistently underestimate. The first is insurance — bank insurance typically does NOT cover the contents of safe-deposit boxes. The bank insures the building, the vault structure, and its operations. It does not insure your specific box contents. Loss from the bank's negligence may be recoverable under specific circumstances; loss from general events (fire, theft, flood) is typically not covered by the bank's policy.

Separate scheduled valuables coverage from your homeowner's or umbrella insurance policy may extend to safe-deposit-box contents — but the rider must specifically include 'off-premises' coverage, since the bullion is no longer at the homeowner's address. Confirm the rider's off-premises language with the insurer before storing meaningful value in a bank box. Some scheduled-valuables riders specifically include safe-deposit-box coverage; others specifically exclude it.

The second caveat is access. Bank safe-deposit boxes are accessible only during the bank's business hours, which excludes evenings, weekends, federal holidays, and (during extraordinary events) bank-closure periods. The 2008 financial crisis saw temporary bank closures in some US regions; the 2020 COVID-era saw extended branch-closure schedules at major banks. Bullion stored in a bank box during such an event is operationally inaccessible regardless of the holder's ownership.

FDIC insurance does not cover safe-deposit-box contents. FDIC insures deposit accounts (checking, savings, CDs) up to the per-depositor limit. The safe-deposit-box service is a separate ancillary product not covered by FDIC.

Practical fit: bank safe-deposit boxes work reasonably for small-to-moderate bullion holdings (`$5,000` to `$50,000` range) where the access profile matches the holder's expected liquidity needs and where the holder has confirmed off-premises scheduled-valuables coverage. For larger holdings or for holdings where access during off-hours is important, private vaults or IRA depositories are typically a better fit.

Private non-IRA vaults

Private commercial vaults offer institutional-grade storage outside the IRA-depository regulatory framework. The major bullion-vault operators (Brink's Global Services, IDS of Texas and Delaware, Loomis, Malca-Amit, and several specialty operations) maintain US retail vaults that accept after-tax bullion storage from individual clients.

Pricing varies. Brink's Global Services maintains retail-vault programs through retail partners (the bullion dealers offering 'storage' as a service usually back this with a Brink's or IDS account) at annual fees in the `$100` to `$300` range for retail-position-size storage. Direct vault accounts with Brink's or IDS at institutional-position scale operate on volume-priced schedules.

Insurance at private vaults is typically institutional-grade — Lloyd's of London underwriting for the major operators, with policy limits at the vault level well above any single retail account's exposure. The vault's storage agreement specifies the coverage terms, sub-limits, and the deductible structure. Read this carefully — major operators publish clean storage-agreement language with explicit coverage disclosure; smaller operators sometimes provide less clarity.

Allocated vs unallocated structure at private vaults follows the same property-law framework discussed in /guides/allocated-vs-unallocated/. Major operators offer both segregated allocated and commingled allocated. Unallocated is typically reserved for institutional clients.

For after-tax bullion holdings above roughly `$50,000`, private vaults are usually the better fit than home storage or bank safe-deposit boxes. The insurance coverage is institutional-grade, access can be scheduled with reasonable notice (typically 24-48 hours for retrieval), and the operational profile matches what bullion-holders typically need.

IRS-approved depositories for Gold IRAs

For Gold IRA holdings the storage choice is constrained to IRS-approved depositories. The IRS-approved framework requires the metal be held in identifiable form (allocated, not unallocated) at a depository meeting the IRS's qualified-trustee or qualified-non-bank-trustee standards.

Major IRS-approved depositories for Gold IRA holdings include Delaware Depository Service Company (Wilmington, Delaware), Brink's Global Services USA (multiple US locations), International Depository Services (IDS) of Texas (New Castle, Delaware and Dallas, Texas), HSBC Bank USA (New York), JPMorgan Chase Bank (New York), and a small number of others. Your Gold IRA custodian's relationship with one or more of these depositories determines which is available on your account.

Pricing for Gold IRA storage at the major depositories (2026-Q2 indicative): • Delaware Depository: `$150/yr` segregated, `$100/yr` commingled, for retail-IRA-account-size positions up to a tier threshold. • Brink's Global Services USA: `$200/yr` segregated, `$125/yr` commingled, indicative for retail IRA accounts. • International Depository Services: `$125/yr` segregated, `$100/yr` commingled, indicative.

All three carry institutional-grade insurance via Lloyd's of London or comparable underwriters. The storage agreement specifies the coverage in detail including the policy limits and any sub-limits per account or per category. Read this before signing.

Allocated storage at IRS-approved depositories is the dominant arrangement. The depository's holdings statement to the IRA custodian (and onward to the account holder) lists the specific bars by refiner, serial number, weight, and fineness. The /reviews/storage-vaults/ hub covers each major depository in more detail.

The /guides/allocated-vs-unallocated/ guide covers the allocated-vs-unallocated property-law distinction. The /case-studies/allocated-storage-after-mf-global/ case study covers the canonical historical episode in which the allocated-vs-unallocated distinction mattered operationally.

Insurance coverage details

Insurance coverage is the variable most commonly under-examined across all four storage options. The relevant questions for each option are (a) what is covered, (b) what is excluded, (c) what is the per-occurrence limit, and (d) what is the per-item or per-category sub-limit.

Home storage: standard homeowner's policies typically cap unscheduled valuables at `$200` to `$2,500`, with scheduled-valuables riders required for meaningful coverage. Bullion-specific exclusions are common in scheduled-valuables riders — confirm in writing. Earthquake and flood are commonly excluded base-policy events; separate riders may be required. Self-insurance above the rider cap is the practical default for meaningful retail holdings.

Bank safe-deposit box: bank insurance does NOT cover box contents. Off-premises scheduled-valuables rider from homeowner's insurance may extend, depending on rider language. FDIC insurance does not apply. Bullion stored here typically operates on a self-insurance basis above the rider cap.

Private vault: institutional Lloyd's of London or comparable coverage, with policy limits at the vault level. The storage agreement specifies the per-account coverage. Read this carefully. Most major operators provide meaningful coverage; smaller operators sometimes provide less.

IRS-approved depository (for Gold IRA holdings): institutional Lloyd's of London or comparable, with policy limits and the agreement language specifying coverage detail. Major depositories (Delaware, Brink's, IDS) publish meaningful coverage information. Verify the per-account coverage matches your account size before assuming it does.

Practical guidance for any meaningful bullion position: read the insurance language explicitly before signing any storage arrangement, including a homeowner's-policy-rider extension. The mere assertion 'insured by Lloyd's of London' is not coverage detail — the policy limits, the per-account sub-limit, the deductible structure, and the excluded-event list are the coverage detail. Confirm in writing.

Access frequency tradeoffs

The four storage options sit on a spectrum from immediate-access to scheduled-retrieval. The right point on the spectrum depends on the holder's expected access frequency, the time-sensitivity of any access event, and the holder's view on the value of physical-immediate-access versus reduced friction in normal periods.

Home storage: immediate access at any time. The holder can hold a coin in hand any moment. The tradeoff is the insurance and security gaps described above.

Bank safe-deposit box: business-hours access only. Friction is moderate during normal periods (a trip to the bank during business hours), high during off-hours and during bank-closure events. Suitable for moderate holdings with infrequent expected access.

Private vault: scheduled retrieval, typically `24` to `48` hours for retrieval at the vault location or via secure shipment to the holder. Some major operators offer expedited retrieval at premium fees. Suitable for larger holdings with infrequent expected access where the institutional security and insurance is the dominant consideration.

IRS-approved depository (Gold IRA): scheduled in-kind distribution or cash distribution, with timing typically `5` to `15` business days depending on the custodian's processing. Not immediate access. The IRA wrapper itself imposes additional friction (custodian paperwork, tax-reporting implications of any distribution). Distinct property regime — the metal is not directly accessible to the holder while it is inside the IRA wrapper; it is held by the depository on behalf of the IRA custodian on behalf of the holder.

Practical guidance: match the storage to the holder's actual expected access frequency. A holder who expects to retrieve bullion only on a multi-decade horizon (typical for retirement-allocation buyers) gets little marginal value from immediate-access home storage compared to institutional vaulting with cleaner insurance. A holder who expects frequent small partial sales gets correspondingly more marginal value from quicker-access arrangements. The /reviews/storage-vaults/ hub covers the specific operational profiles of major operators.

How we sourced this

Citations draw from the published storage-fee schedules of major IRS-approved depositories (Delaware Depository Service Company, Brink's Global Services USA, International Depository Services); IRS Publication 590-A and 590-B for the home-storage Gold IRA guidance; the UL safe-rating standards (UL 687 for tool-rating safes); and the published storage-agreement language from a sample of bullion-vault operators.

Insurance coverage detail was compiled from a sample of homeowner's insurance carrier policies, the typical scheduled-valuables rider structure across major US insurers, and the published storage-agreement insurance disclosure from major depositories. Bullion-specific exclusion language varies by carrier; the generalizations here reflect the dominant pattern but every specific policy should be confirmed in writing.

Storage-pricing snapshot dates: 2026-Q2 for the depository fees, drawn from the depositories' published fee schedules as of May 2026.

In plain English

In plain English: four options. Home storage works for after-tax holdings if you have a real safe and a real scheduled-valuables rider; it does NOT work for Gold IRA holdings (the IRS forbids it). Bank safe-deposit boxes work for moderate after-tax holdings if you have off-premises insurance coverage — but the bank does not insure your box contents. Private vaults (Brink's, IDS) work well for larger after-tax holdings at $100-$300/yr with institutional insurance. IRS-approved depositories (Delaware Depository, Brink's, IDS) are mandatory for Gold IRA holdings; pricing is similar to the private-vault tier. Read the insurance language before signing anything. Match the storage to your actual expected access frequency, not your imagined need for immediate access.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Can I store gold at home?

For after-tax holdings, yes — many people do. For Gold IRA holdings, the IRS has consistently taken the position that home storage does not satisfy Section 408(m) requirements. Use an IRS-approved depository for IRA holdings. -

Does homeowner's insurance cover gold?

Most standard policies cap unscheduled valuables (jewelry, coins, bullion) at $200-$2,500. Scheduled coverage (named-item rider) is needed for meaningful coverage above that. Some insurers exclude bullion entirely; confirm in writing. -

Are bank safe-deposit boxes insured?

Bank insurance typically does NOT cover the contents of safe-deposit boxes. The bank insures the building and its operations, not your box contents. You must arrange separate scheduled valuables coverage. -

What insurance do IRS-approved depositories carry?

Major depositories (Brink's, Delaware Depository, IDS) carry institutional insurance via Lloyd's of London or comparable underwriters. Coverage details and exclusions are disclosed in the storage agreement; read them before signing.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.