Gold mining stocks vs physical bullion

Operational leverage, dividend yield, jurisdictional risk, and the tradeoffs of holding gold-mining equities versus physical bullion.

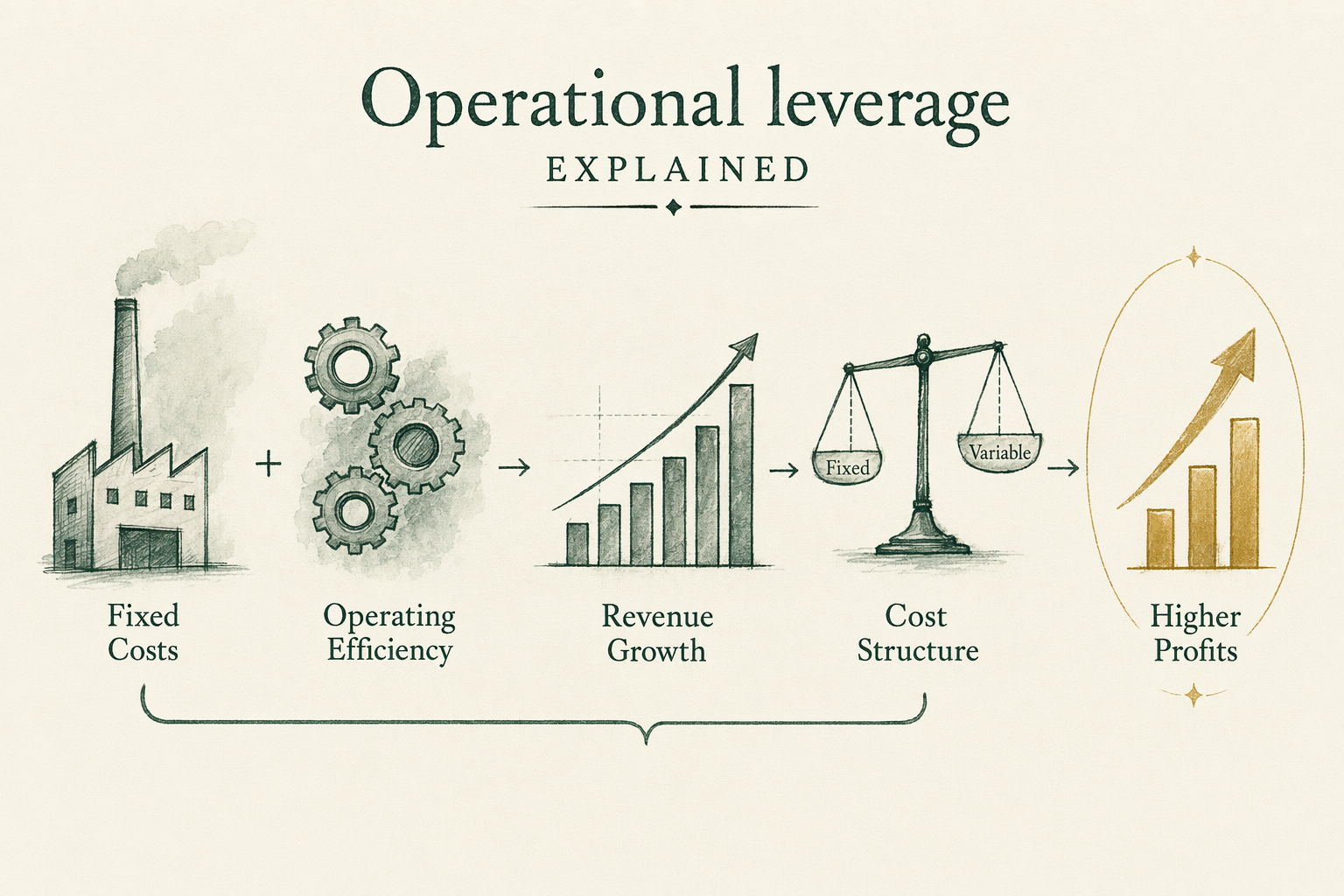

Operational leverage explained

Mining companies sell gold (and silver, copper, other co-products) at the prevailing market price. Their cost structure is largely fixed in the short run: extracting an ounce from a mature mine costs roughly what it cost last quarter, regardless of where spot moves. When the gold price rises, the price moves through to revenue while costs stay flat, so earnings rise faster than the metal itself. This is what mining analysts call 'operational leverage.' For a hypothetical miner producing gold at an all-in sustaining cost (AISC) of `$1,400/oz` when gold is `$2,000/oz`, a `10%` move in gold to `$2,200` raises margin from `$600` to `$800` per ounce — a `33%` jump in per-ounce gross profit.

Operational leverage cuts both ways. A `10%` decline in gold from `$2,000` to `$1,800` cuts the same miner's per-ounce margin from `$600` to `$400` — a `33%` drop. For higher-cost miners closer to break-even, the leverage is more extreme; a small move in gold can flip them between profitability and loss. This is the structural reason gold miners exhibit beta to gold typically in the `1.5x-3x` range, with junior miners frequently above `3x`. The headline 'miners give you leverage on gold' is mathematically correct, but the leverage compounds operational and company-specific risk on top of gold's own volatility.

Dividend yield

Major producing gold miners pay dividends; physical gold does not. Newmont's trailing dividend yield has run roughly `2-4%` in recent years; Barrick Gold's roughly `1.5-3%`; Agnico Eagle's roughly `1.5-2.5%`. The dividend income is taxable as ordinary dividend income (qualified or non-qualified depending on holding period and account type), which is a meaningfully different tax profile than physical gold's collectibles-rate `28%` long-term capital gains treatment.

The dividend is also a structural floor on miner share prices in flat-to-positive gold environments. A miner trading at a `3%` yield with stable production and reasonable balance sheet has a recurring cash return that physical bullion lacks. In a multi-year sideways gold market (say `2013-2019`), the dividend income meaningfully outperformed holding the equivalent dollar amount in physical gold, which produced no income. Dividends are not guaranteed; miners have cut or suspended dividends in commodity downturns (Newmont in `2013-2014`, Barrick in 2015). The yield is income, not a coupon.

Jurisdictional risk

Mining companies operate in specific countries with specific tax, regulatory, royalty, and political risk profiles. Newmont's operations span the US, Canada, Australia, Ghana, Argentina, Peru, Mexico, and the Dominican Republic. Barrick's span the US, Canada, Dominican Republic, Argentina, Mali, Tanzania, Saudi Arabia, and others. The Fraser Institute's annual mining-jurisdiction survey ranks jurisdictions on policy attractiveness; the spread between top-quartile (Nevada, Saskatchewan, Western Australia) and bottom-quartile (Venezuela, certain African operations, parts of South America) jurisdictions is significant in policy stability and expropriation risk.

Jurisdictional risk is non-trivial. The `2017` Tanzanian export ban on unprocessed mineral concentrates materially hit Acacia Mining (later absorbed by Barrick). The `2015-2018` Argentine currency-control regime affected mine-revenue repatriation. The `2022-2024` Mali military-government tax-reassessment dispute hit Barrick's Loulo-Gounkoto complex. Investors holding a gold-mining ETF (GDX, GDXJ) get a basket that diversifies some jurisdictional risk, but individual large-miner positions concentrate it. Physical bullion held in a stable-jurisdiction depository has none of this exposure.

Major vs junior miner profiles

Senior producers (Newmont, Barrick, Agnico Eagle, AngloGold Ashanti, Gold Fields, Kinross) produce in the `1-6 million ounces per year` range, carry diversified mine portfolios, pay dividends, and have liquid equity markets. They are the conservative end of gold-equity exposure. Beta to gold typically runs `1.5-2.5x`, drawdowns are deep but recoverable, and the businesses are durable across multi-year commodity cycles.

Junior miners (exploration-stage and small-production companies) are a different risk profile. They typically have a single project or small portfolio, often pre-revenue or marginally profitable, often equity-financed through frequent secondary offerings. Junior-miner beta to gold can reach `4-6x` or higher in some windows. Drawdowns can be terminal: the junior space includes a steady population of companies that wind down or get acquired at distressed prices when capital markets close. The GDXJ ETF aggregates this exposure into a basket. Investors approaching juniors should expect equity-like permanent-loss risk, not a leveraged claim on gold.

Why miners can lag bullion

Despite operational leverage, gold miners as a group have frequently lagged physical gold over multi-year windows. From `2010` to `2024`, gold rose roughly `60-70%` in nominal terms while the NYSE Arca Gold Miners Index (the GDX benchmark) was approximately flat to modestly negative. The drag came from cost inflation (energy, labor, equipment), reserve depletion forcing higher AISC, dilution from secondary equity offerings, ill-timed acquisitions during the `2011-2012` peak (Barrick's Equinox acquisition, several others), and impairment charges that crystallized during the `2012-2015` downturn.

Mining-equity returns also depend on management decisions investors cannot evaluate from the gold price alone: capital-allocation discipline, hedging policy, project-execution capability, and balance-sheet management. The 'miners as leveraged gold' framing assumes management converts every dollar of margin into shareholder return. The historical record is messier — large portions of the `2009-2012` margin expansion got reinvested into projects that subsequently impaired, leaving shareholders worse off than holders of physical bullion. Miners are equities first and gold proxies second; that ordering produces the lag.

Real-world example — Newmont, Barrick, and bullion 2020-2024

Consider an investor who put `$10,000` into each of three positions at the start of `2020`: physical gold, Newmont Corporation common stock, and Barrick Gold common stock. LBMA spot gold opened `2020` near `$1,520/oz` and ended `2024` near `$2,650/oz` — roughly `+74%` nominal. The `$10,000` in physical gold (less premiums and storage fees) ended near `$17,400` in spot-equivalent value.

Newmont (NEM) opened `2020` near `$43.50` and ended `2024` near `$37.50` — a price decline of roughly `-14%`, with cumulative dividends of roughly `$5.50/share` ($1.50/share annualized, declining mid-period). The position ended near `$9,900` (price + dividends, ignoring reinvestment). Barrick (GOLD) opened near `$18.50` and ended near `$15.50` — roughly `-16%` price-only, with cumulative dividends of roughly `$2.20/share`. The position ended near `$9,500`. Both miners materially underperformed bullion despite rising gold. Cost inflation, project-execution headwinds, and write-downs explained the gap. The case study is not a forecast — different periods produce different results — but it illustrates why the 'miners as leveraged gold' frame is incomplete.

Common misconceptions about miners

**'Miners are leveraged gold.'** Mathematically, operating leverage gives miners higher beta to gold than `1.0`. Empirically, that leverage often gets eroded by cost inflation, dilution, and capital-allocation missteps. The leverage shows up in short-window moves but frequently disappears over multi-year periods.

**'Big miners are safer than physical gold.'** Different risk, not less risk. Senior miners carry geopolitical, management, and operational risk that physical gold does not. Bullion's risk is custody and price; miners stack equity-business risk on top of gold price.

**'Junior miners are a sensible way to get gold exposure.'** Juniors function more like venture-stage equity than commodity exposure. Permanent loss is a normal outcome in the junior space. They are a different investment category than physical gold and should be sized as such.

What this means for you

Physical bullion and gold-mining equities are different exposures, not substitutes. Bullion gives you the metal — no business risk, no jurisdictional risk, no dividend, no income. Miners give you exposure to gold-price beta plus everything else that goes into running a mining business in real jurisdictions. If you want monetary insurance, hold bullion. If you want equity-style exposure to gold producers and you can tolerate equity-business risk on top of gold's own volatility, consider a senior-miner basket or ETF (GDX). Junior miners belong in a small, speculative sleeve, sized as equity venture-stage exposure rather than commodity allocation. As always, BullionLens does not provide personalized advice; consult a licensed adviser before adding mining equities to a portfolio.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Do mining stocks track the gold price?

Imperfectly. Miners have operational leverage (a 10% move in gold can produce a 20-40% move in a miner's earnings), but they also carry jurisdictional, management, and project-execution risks unrelated to the gold price. -

Are miners a substitute for physical gold?

No. Miners are equities with their own business risk profile. They are an exposure to gold-price beta plus company-specific factors. Physical gold is a pure metal position. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority. -

When was this page last reviewed?

See the 'Last reviewed' date at the bottom of the page. We commit to a quarterly minimum review cycle; fee schedules, IRS rules, and company arrangements can change between reviews — confirm with primary sources before transacting.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.