Platinum and palladium as bullion investments

Platinum and palladium fundamentals: industrial demand (catalytic converters), supply concentration, IRA eligibility, and the role in a metals allocation.

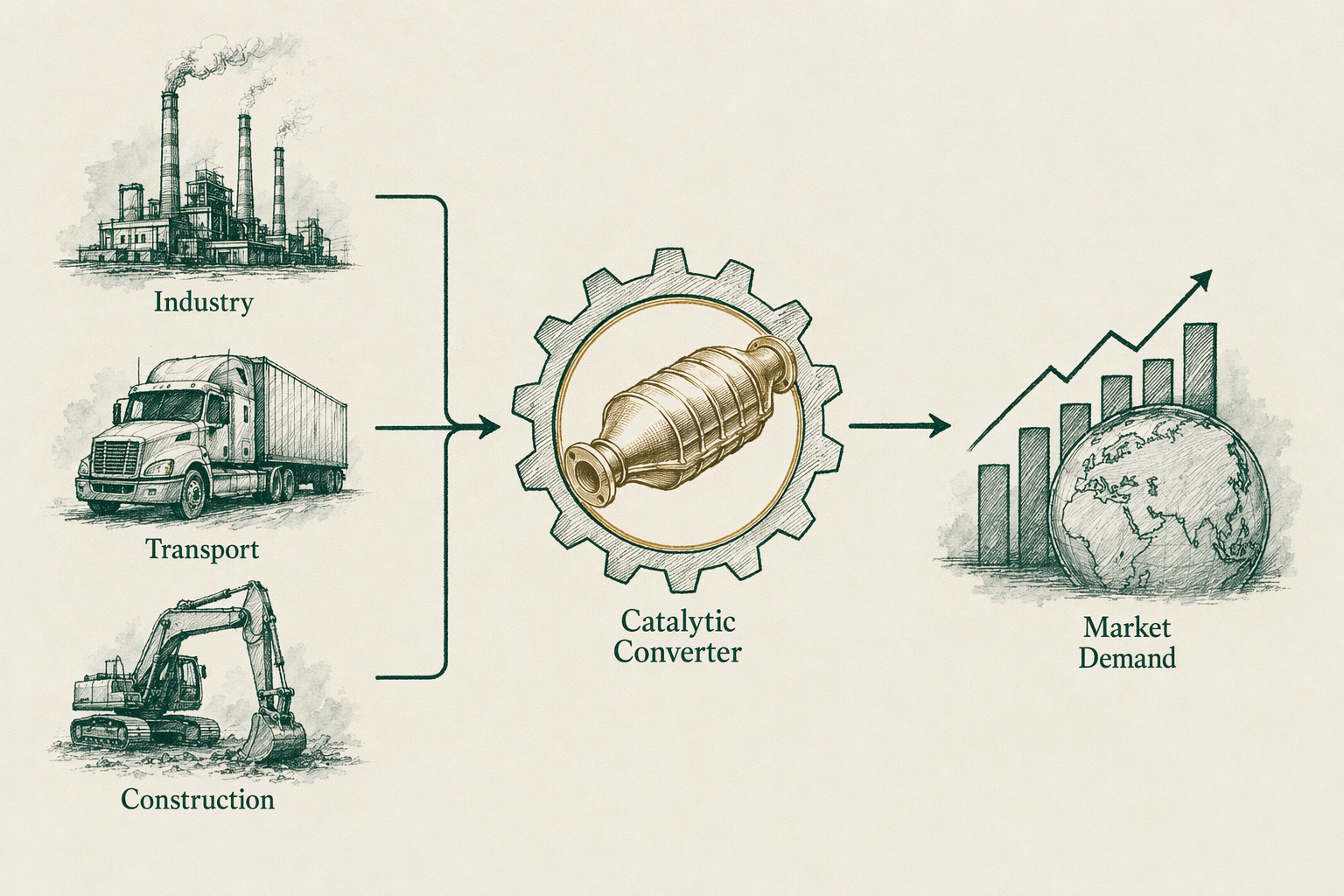

Industrial demand and the catalytic-converter market

Platinum and palladium belong to the platinum-group metals (PGMs), six chemically related metals that include rhodium, ruthenium, iridium, and osmium. The investment market for PGMs centers on platinum and palladium because they have liquid bullion markets, recognized refiners, and IRS-approved coin-and-bar formats. Their demand profile differs sharply from gold's: per the World Platinum Investment Council (WPIC) `2024` data, roughly `40-45%` of annual platinum demand goes to autocatalysts in diesel and gasoline engines, with the remainder split among jewelry, industrial chemical applications, and a smaller investment slice.

Palladium is even more autocatalyst-concentrated. Norilsk Nickel and other industry reports place autocatalyst demand at roughly `75-80%` of global palladium consumption, the bulk of it in gasoline-engine catalytic converters. The structural implication is direct: PGM prices track global vehicle production cycles, emissions-regulation tightening, and the gasoline-vs-diesel-vs-electric mix in major auto markets. The `2015` Volkswagen emissions scandal pushed European diesel deeply out of favor, shifting catalytic-converter demand from platinum toward palladium and contributing to palladium's `2017-2022` price rally. The reverse substitution (gasoline-engine palladium back toward platinum as palladium got expensive) is the kind of demand mix shift that gold simply does not have.

Supply concentration (South Africa, Russia)

PGM supply is geographically narrow. South Africa produces roughly `70%` of global mined platinum and a meaningful share of palladium; Russia (largely via Norilsk Nickel) produces roughly `40%` of global mined palladium and significant platinum. The next-largest producers (Zimbabwe, Canada, United States) are materially smaller. This concentration matters for price stability: a single labor action at a South African mine complex, a single sanctions decision affecting Russian metal, or a power-grid disruption in Mpumalanga can move PGM prices `10-20%` in a few weeks.

The supply-concentration story has produced multiple meaningful price episodes since `2010`. South African platinum-miner strikes in `2012` and `2014` (the AMCU strikes lasting months) tightened platinum supply. The `2022` Russian invasion of Ukraine raised concerns about palladium and platinum sanctions exposure; the LBMA suspended Russian refiners from its Good Delivery list, fragmenting the institutional market for new Russian-origin bars. Investors evaluating PGMs need to weight supply-chain risk in a way they do not for gold, whose supply is geographically diffuse and whose primary above-ground stock dwarfs annual mine flow.

IRA eligibility

Platinum and palladium are both IRA-eligible under IRC Section `408(m)` at a `99.95%` fineness requirement (versus `99.5%` for gold and `99.9%` for silver). The American Platinum Eagle is specifically named-permitted in the statute, analogous to the American Gold Eagle and American Silver Eagle exceptions. Other IRA-eligible formats include platinum and palladium bars from LBMA-Good-Delivery-listed refiners (PAMP Suisse, Valcambi, Credit Suisse, Royal Canadian Mint, and others), at the required fineness.

Custodian coverage of platinum and palladium varies. Some Gold IRA custodians (Equity Trust, STRATA Trust, Kingdom Trust historically) support PGM holdings within IRA accounts; others limit IRA-eligible metals to gold and silver only. If you intend to hold PGMs in an IRA, confirm with the custodian before opening the account that PGM purchases, storage, and reporting are supported. Depositories generally accept PGMs (Delaware Depository, Brink's, IDS) but storage fees may differ from the gold/silver schedule and the per-ounce storage cost-of-ownership can be higher relative to the metal's dollar value.

Volatility

PGM volatility has historically run materially higher than gold's. From `2010` to `2024`, palladium's annualized monthly-return standard deviation has been roughly `2.5-3x` gold's. Platinum's has been roughly `1.5-2x`. The episodes are vivid: palladium rose from roughly `$675/oz` in early `2016` to a peak above `$3,000/oz` in March `2022` — a `+345%` move — then fell to under `$900/oz` by late `2024`, a `-70%` drawdown from peak. Platinum's drawdown from its `2008` peak above `$2,200/oz` to its `2015-2018` range below `$900/oz` was similarly severe.

Drawdowns of this magnitude reflect the demand-substitution dynamic in the autocatalyst market plus the supply-chain fragility. When palladium got expensive enough that auto OEMs accelerated platinum substitution, palladium fell while platinum recovered. When the electric-vehicle transition story tightens, both metals come under demand pressure from a structural narrative that did not exist 15 years ago. The base rate for PGMs is that they can produce multi-year drawdowns deeper than gold or silver, and position-sizing has to account for that.

Where each fits in a metals allocation

PGMs do not function as monetary-debasement hedges in the way gold does. Their long-run correlation to gold is moderate (roughly `+0.3` to `+0.5` on monthly data over multi-year windows), and they have meaningful idiosyncratic industrial-cycle exposure. A reasonable framing: PGMs are commodity exposure with a precious-metals tax-treatment wrapper, not a monetary hedge. Investors holding them as part of a precious-metals sleeve should think of them as the cyclical-industrial portion of the sleeve, not the monetary-insurance portion.

Sizing guidance is necessarily personal — and BullionLens does not provide personalized advice — but practitioner conversations frequently land at `0-20%` of any precious-metals sleeve in PGMs combined, with `gold` carrying the bulk of the sleeve. PGMs make more sense for investors with a specific thesis on auto-catalytic-converter demand, EV-transition timing, or South-African-Russian supply risk; they make less sense for investors using metals strictly as portfolio insurance against monetary or financial-system shocks. Consult a licensed adviser before adding PGMs to a retirement portfolio.

Real-world example — palladium's 2017-2022 round trip

Consider an investor who entered palladium in January `2017` at roughly `$760/oz`. By March `2022`, the LBMA palladium fix peaked above `$3,000/oz` — a `+300%` move that materially outpaced any other major commodity over the same window. An investor who held a `$50,000` palladium position from January `2017` would have seen a peak portfolio value of roughly `$200,000` by Q1 `2022`. The same `$50,000` rolled into gold would have moved from roughly `$56,000` to roughly `$104,000` over the same window — meaningful but materially smaller.

The reverse side of the trade arrived. From the March `2022` peak, palladium fell to under `$900/oz` by late `2024`, a `-70%` drawdown that wiped out most of the rally for any holder who failed to take profits at or near the peak. An investor who bought palladium in early `2022` at `$2,500/oz` was sitting on a `-64%` loss less than three years later. The lesson is not that palladium is a bad investment; it is that PGMs produce both the rallies and the drawdowns to match. A `5%` portfolio sleeve in palladium contributes meaningfully different year-to-year noise than a `5%` sleeve in gold.

Common misconceptions about PGMs

**'Platinum and palladium are just precious metals like gold.'** Operationally and tax-wise yes, but their demand profile is industrial, not monetary. Treating them as substitutes for gold in a monetary-debasement-hedge thesis misreads the metal.

**'PGMs always rally during crises.'** No. PGMs sold off sharply in the `2008` recession alongside other industrial commodities. Their crisis behavior depends on whether the crisis is a monetary one (where gold rises but PGMs lag) or an industrial demand shock (where PGMs can fall faster than gold).

**'Electric vehicles will eliminate PGM demand.'** Slowly, partially, and unevenly. EV adoption removes catalytic converters from new gasoline-and-diesel vehicles, but the existing global fleet contains hundreds of millions of vehicles needing replacement catalysts for decades. Demand will likely peak before declining; the timing is the open question, not the direction.

What this means for you

Platinum and palladium are a different exposure from gold — more cyclical, more concentrated in supply, more volatile, and structurally tied to the auto-industry demand cycle. If you want monetary insurance, hold more gold and fewer PGMs. If you have a specific thesis on industrial-cycle pricing, supply-chain risk in South Africa or Russia, or the EV-transition timing, PGMs offer exposure that gold does not. Within an IRA, confirm custodian support for PGM holdings before opening the account. As with any allocation decision, BullionLens does not provide personalized advice; talk to a licensed adviser about whether and how PGMs fit your portfolio.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Is platinum a hedge like gold?

Less so. Platinum and palladium prices are heavily driven by industrial demand (especially auto catalytic converters), making them more cyclical and less monetary-store-of-value than gold. -

Are platinum and palladium IRA-eligible?

Yes, at 99.95% fineness or higher. American Platinum Eagles are the named sovereign exception (similar in pattern to Gold and Silver Eagles). -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority. -

When was this page last reviewed?

See the 'Last reviewed' date at the bottom of the page. We commit to a quarterly minimum review cycle; fee schedules, IRS rules, and company arrangements can change between reviews — confirm with primary sources before transacting.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.