Silver vs gold as an investment

Volatility, industrial demand, storage density, premium structures, and tax treatment: how silver differs from gold in a precious-metals allocation.

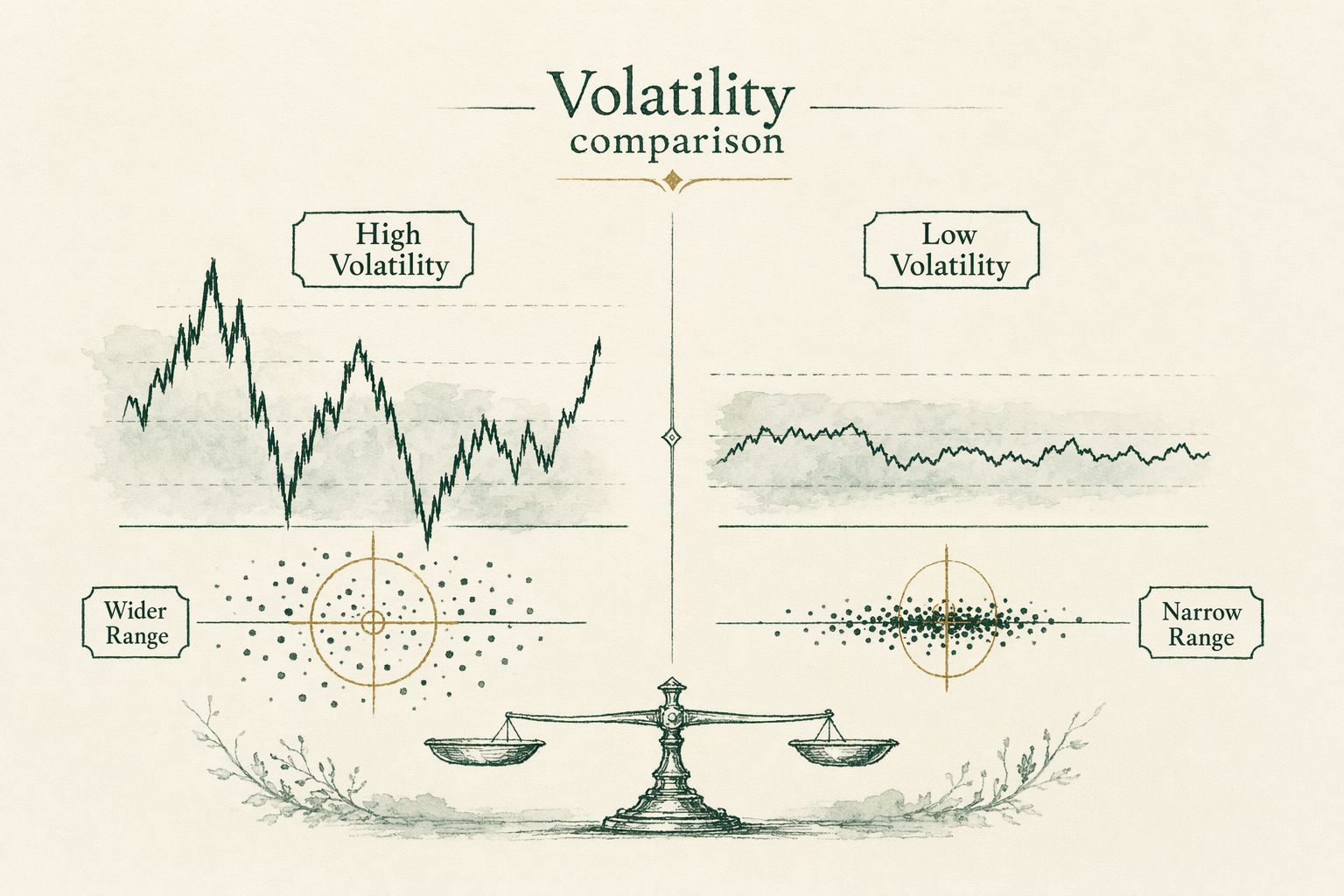

Volatility comparison

Silver and gold are both precious metals, both monetary metals at different points in history, and both held by retail investors as portfolio diversifiers. They are not interchangeable. Silver's annualized standard deviation of monthly returns since `1971` has run roughly `1.5`-to-`2` times gold's. In the 2010-2011 rally, silver rose from roughly `$18/oz` to a `$48.70` peak in April `2011` — a `+170%` move that outpaced gold's `+85%` in the same window. The mirror image followed: from the `2011` peak, silver fell to under `$14/oz` by January `2016` — a `-71%` drawdown — while gold lost roughly `-43%`.

Silver's volatility is structural, not anomalous. It has a smaller market (`LBMA` silver fix daily volumes run roughly `5-10%` of gold's by dollar value), broader industrial-vs-investment demand mix, and a more limited central-bank reserve role. Position sizing that works for gold will often produce uncomfortable swings in silver. A `5%` portfolio gold allocation contributes meaningfully different volatility than a `5%` portfolio silver allocation; the silver sleeve will dominate the portfolio's year-to-year noise in a way the gold sleeve will not.

Industrial demand for silver

Roughly `50%` of annual silver demand comes from industrial uses — solar panels, electronics, brazing alloys, medical applications, photography (residual). Per the Silver Institute's `2024` World Silver Survey, industrial fabrication demand hit a record `654.4` million ounces in `2023`, with solar/photovoltaic consumption alone reaching roughly `200+` million ounces. Investment demand (coins, bars, ETF flows) is the other roughly `50%`. Gold's split is roughly inverted: investment + central-bank demand dominates, with industrial and dental at single-digit percentages.

The industrial-demand mix matters for the investment thesis. Silver's price responds to global industrial-cycle indicators (PMI prints, solar-panel-deployment forecasts, semiconductor cycle) in addition to monetary-and-financial drivers that move gold. In recessions, industrial demand can soften silver even when monetary-debasement narratives lift gold. In strong industrial cycles with positive monetary backdrops (the `2020-2021` post-pandemic window is the cleanest recent example), silver can materially outpace gold. Investors expecting silver to behave as 'gold with leverage' get only a partial picture; silver is a hybrid monetary-industrial metal, and the industrial half can dominate.

Storage density (silver is bulky)

At current spot prices around `$30/oz` for silver and `$2,400/oz` for gold (illustrative — confirm at LBMA at the time of any purchase), `$50,000` of silver weighs roughly `52` kilograms (about `115` lbs). `$50,000` of gold weighs roughly `0.65` kilograms (about `1.4` lbs). The ratio is structural: silver is intrinsically less expensive per ounce, so any given dollar value carries roughly `80x` the weight by mass.

Storage and shipping costs scale with weight and volume. Allocated-storage fees at IRS-approved depositories are typically quoted per-troy-ounce or per-pound; storing `52 kg` of silver in segregated allocated storage runs materially more per year than storing `0.65 kg` of gold for the same dollar exposure. Home storage faces the same arithmetic: a `5%` portfolio silver sleeve on a `$1,000,000` portfolio means storing roughly `52 kg` of metal somewhere, while the equivalent gold sleeve is small enough to fit in a single safe-deposit-box drawer. Storage density is one of the practical reasons large investment allocations skew gold-heavy.

Tax treatment

Under US tax law, both gold and silver are classified as 'collectibles' under IRC Section `408(m)`. Long-term capital gains on physical bullion of either metal are taxed at a maximum `28%` rate (versus `20%` for most other long-term gains). Short-term gains (held one year or less) are taxed as ordinary income at the holder's marginal rate. This treatment is symmetric across metals; the dealer can issue an IRS Form `1099-B` on certain qualifying sales of either silver or gold of certain quantities and finenesses.

Inside a Gold IRA wrapper, both gold and silver enjoy tax-deferred (Traditional IRA) or tax-free-on-qualified-distribution (Roth IRA) treatment, subject to standard IRS rules. American Silver Eagles are specifically named-permitted under IRC `408(m)`, as are several other silver coins and `.999`-fineness silver bars from IRS-approved refiners. State sales-tax treatment varies; most states exempt investment-grade silver above a threshold dollar amount, but a minority of states tax silver fully. Confirm with your state's department-of-revenue published rules and read your custodian's IRA-eligibility list before transacting.

Real-world example — sizing $50,000 in silver vs gold

An investor allocates `$50,000` of a retirement IRA to precious metals and is deciding between an all-gold sleeve and a split gold/silver sleeve. At illustrative prices of `$2,400/oz` gold and `$30/oz` silver, the all-gold scenario buys roughly `20.5 oz` of gold (a stack of bullion coins fitting in a small box). A `60/40` gold-to-silver split buys `12.5 oz` of gold and `666 oz` of silver — the silver portion alone weighs over `20 kg`.

Storage economics shift accordingly. Segregated allocated storage at Delaware Depository runs roughly `$150/yr` for a small all-gold sleeve. The mixed sleeve adds material per-pound storage cost on the silver portion — call it another `$80-150/yr` depending on the depository's silver schedule — so total storage runs roughly `$250-300/yr`. Over `10` years, the mixed sleeve incurs `$1,000+` more in storage costs in exchange for the diversification of having two metals. Whether that tradeoff fits the investor's allocation thesis depends on whether silver's industrial-cycle exposure adds something the gold sleeve lacks; if the goal is monetary-debasement hedging, the all-gold sleeve does that more cheaply.

Common misconceptions about silver

**'Silver is gold with leverage.'** Partially true — silver has historically moved roughly `1.5-2x` gold's percentage in both directions. But silver's industrial demand component means it can decouple from gold during recessions or industrial-cycle weakness. It is not a pure beta on gold.

**'Silver will catch up to gold (the ratio thesis).'** The gold-silver ratio sat near `15:1` for centuries under bimetallic monetary regimes; it has averaged closer to `60:1` over the past `40` years. There is no academic literature establishing that the historical bimetallic ratio is a predictive benchmark for modern markets. The gold-silver ratio is a descriptive metric, not a trading signal.

**'Silver storage is the same as gold storage.'** No. Silver storage is materially more expensive per dollar of exposure because the metal is roughly `80x` heavier per dollar. Home storage of large silver allocations also requires more secure space than equivalent gold.

What this means for you

Silver and gold are not substitutes; they are complements with different risk profiles. If your thesis is monetary-debasement hedging or diversification against equity drawdowns, gold does that more cheaply and with lower volatility. If your thesis includes industrial-cycle exposure or you specifically want the higher-beta precious-metals position, silver adds something gold does not. Storage economics, premium structure, and volatility all push large-dollar allocations toward gold; smaller allocations or those with industrial-cycle conviction can support a silver sleeve. As always, BullionLens does not provide personalized allocation advice; consult a licensed adviser who knows your full portfolio context.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Is silver more volatile than gold?

Yes, historically by a wide margin. Silver's price swings have typically been 1.5-2x larger than gold's, both up and down. The gold-silver ratio reflects this — it ranges widely as silver outpaces or lags gold. -

Why is silver storage harder than gold?

At current prices, $50,000 of silver is roughly 30-50 times bulkier and heavier than $50,000 of gold. Storage and shipping costs scale with weight and volume, making silver less practical for large allocations. -

Is silver IRA-eligible?

Yes — silver bullion at 99.9% fineness or higher is IRA-eligible under IRC Section 408(m), as is the American Silver Eagle (which has a special named exception similar to the Gold Eagle). -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.