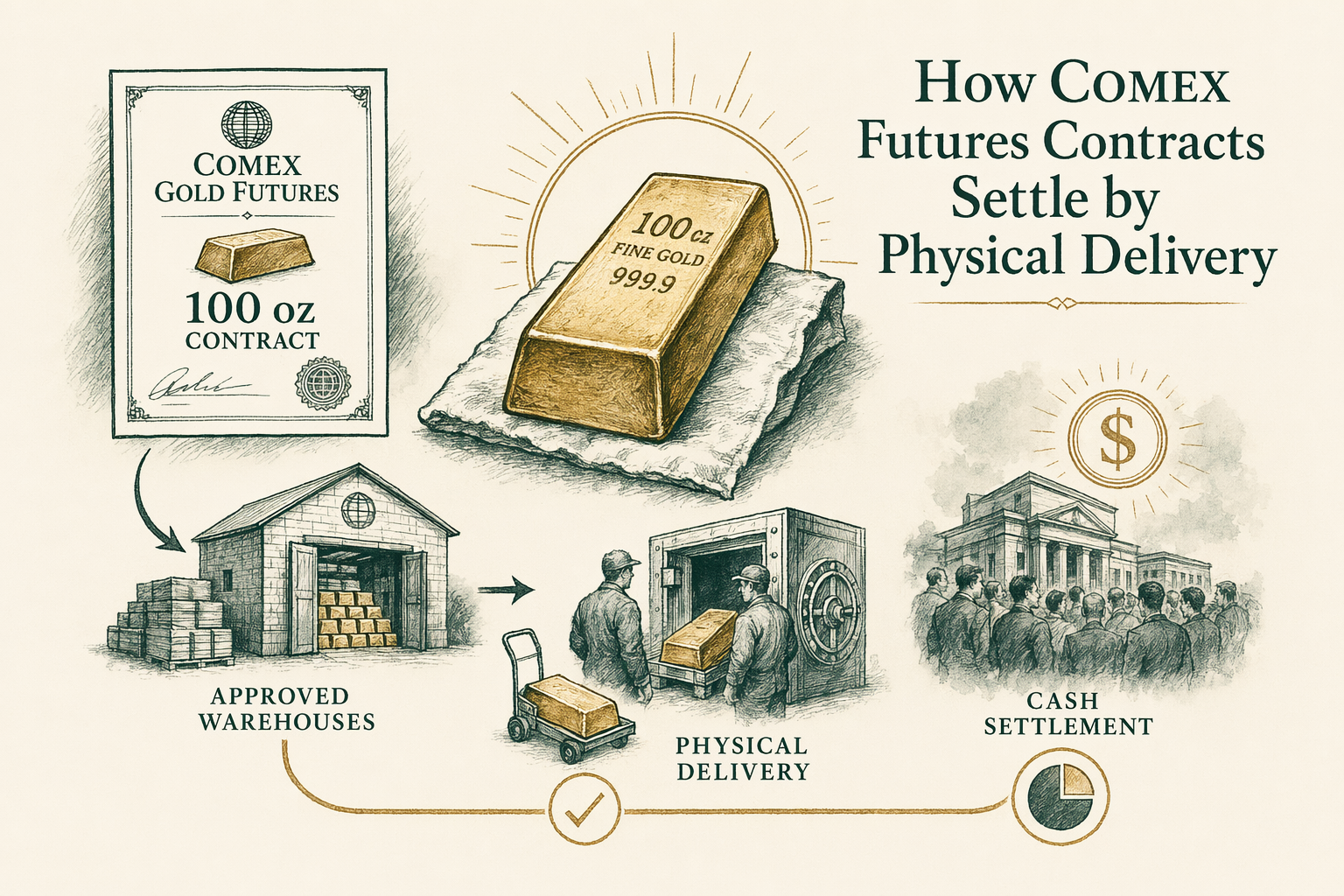

What is COMEX physical delivery?

How COMEX futures contracts settle by physical delivery: the 100-oz contract spec, approved warehouses, and why most contracts settle in cash.

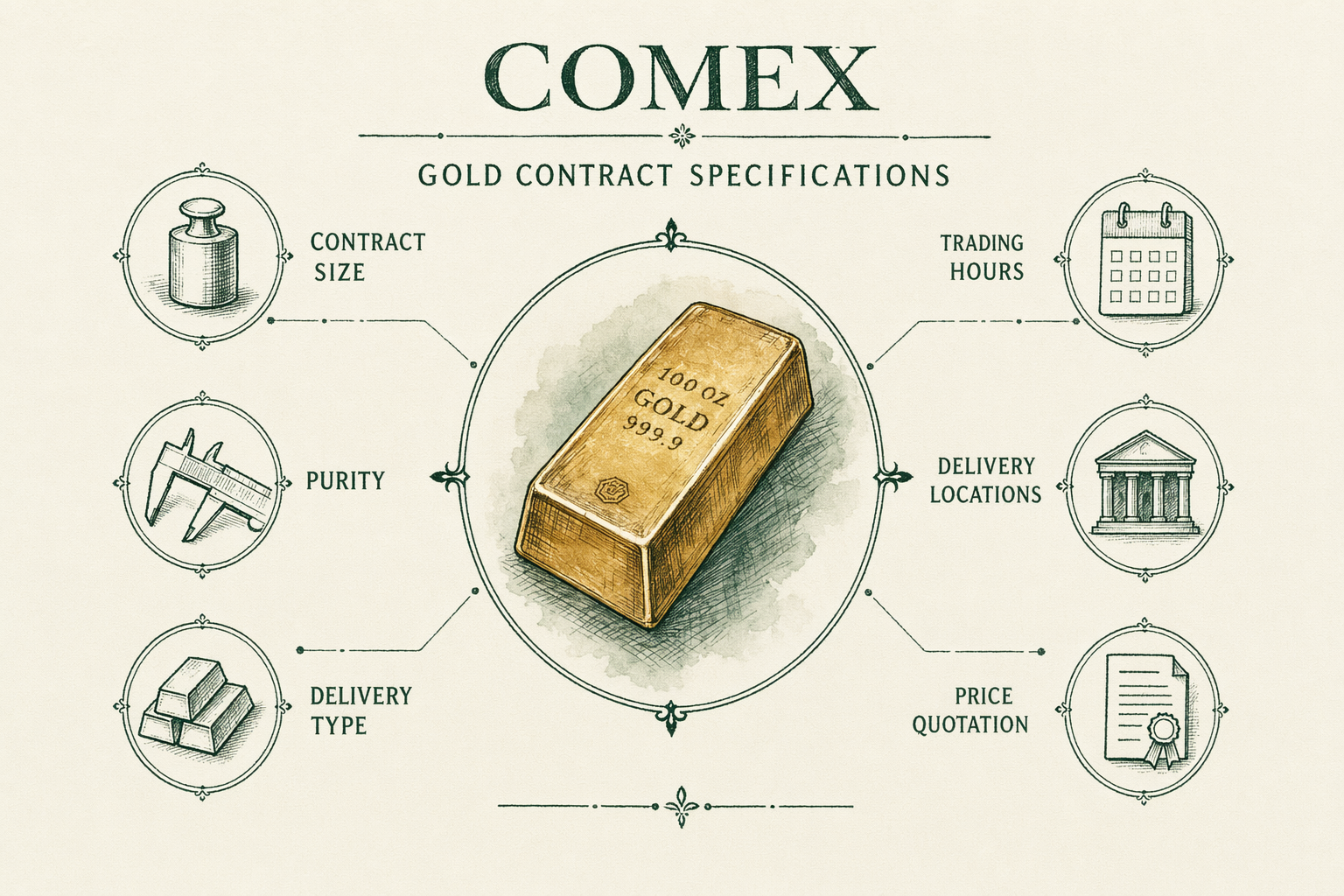

COMEX gold contract specifications

The CME Group's COMEX gold futures contract, ticker symbol `GC`, represents `100 troy ounces` of gold with minimum `0.995` fineness. The contract size sets the threshold for participation — at a spot price of `$2,358/oz`, one `100 oz` contract carries a notional value of `$235,800`. Smaller contract sizes exist (the E-Micro Gold contract `MGC` at `10 oz`, the Micro Gold contract at `1 oz`), but the standard `GC` is the benchmark institutional contract.

Deliverable forms specified in the contract: one `100 troy ounce` gold bar OR three `1 kilo` gold bars, each from a refiner approved by the exchange. Bars must come from a refiner on the approved list (which historically has included PAMP Suisse, Credit Suisse, Argor-Heraeus, Metalor, Heraeus, Johnson Matthey, Royal Canadian Mint, and others) and must be accompanied by the appropriate assay documentation. Snapshot as of `2026-Q2` — the approved refiner list is updated periodically by the exchange.

Approved warehouses and assayers

Physical delivery against a COMEX gold contract requires delivery from an exchange-approved warehouse. The approved warehouse list has historically included Brink's, Loomis, JPMorgan Chase, HSBC, Manfra Tordella & Brookes (MTB), and several others. Each approved warehouse holds gold inventory categorized as either "Eligible" (meets contract delivery specifications but not committed to a specific delivery) or "Registered" (issued against a specific delivery notice).

The Eligible-vs-Registered split is closely watched by market participants. Eligible inventory represents the pool of bullion that could be tendered for delivery; Registered inventory has actually been committed against open contracts. Spikes in the Registered category — observed during certain `2020-2023` periods — signal increased physical-delivery demand against the futures market and have been cited as evidence of physical-vs-paper tightening.

Approved assayers — the labs whose stamps and certifications the exchange accepts as authoritative on bar fineness — are also part of the system. Bars without an approved assayer's mark cannot be tendered for delivery, which is why bar provenance matters beyond aesthetic considerations.

Notice day and delivery process

Each COMEX gold contract month has a First Notice Day — the first business day on which the holder of a short position can issue a delivery notice to the long position. The notice initiates the physical-delivery process: the long position is assigned a specific bar (or bars) from an approved warehouse, and the long pays the contract price for the bullion.

The mechanical sequence: First Notice Day → short issues notice → exchange assigns long counterparty → long pays for and receives a warehouse receipt → long can either hold the warehouse receipt (continued storage at the approved warehouse) or arrange physical removal (with appropriate insured transport).

Most contract holders close their positions before First Notice Day to avoid the delivery process. The traders who do take delivery are typically institutional — bullion banks, refiners, large hedge funds with the operational capacity to handle the warehouse-receipt-and-bullion logistics.

Why most contracts settle in cash

The substantial majority of COMEX gold contracts are closed (offset) before First Notice Day, with neither side taking or making physical delivery. Several reasons:

**Operational complexity**: Taking delivery requires brokerage and clearinghouse arrangements many retail and even small-institutional accounts do not have. Most futures-trading accounts are configured for cash settlement, not physical delivery.

**Storage and logistics**: A warehouse receipt is straightforward, but physical removal involves insured transport (Brink's or Loomis armored ground transport, or Brink's secure air), customs and regulatory paperwork if shipping internationally, and the buyer's own insured storage at destination. None of this is impossible; all of it is operationally cumbersome.

**Cost basis**: The cost basis on physical delivery is the contract settlement price plus transport. The same bullion bought through a major bullion dealer typically costs less per ounce (dealer premium often runs below the futures-market spread plus transport) for the smaller buyer who doesn't already operate at COMEX scale.

**Market participants**: Most COMEX participants are not seeking physical bullion. They are hedging mining production, hedging jewelry/refining demand, taking directional positions on the gold price, or providing market-making liquidity. Cash settlement serves all of these without involving the warehouse logistics.

Recent delivery volume context

Historical baseline: in normal market conditions, perhaps `1-3%` of contract notional results in physical delivery, with the rest closing out before First Notice Day. The CME publishes monthly delivery statistics that any researcher can consult for current data.

**Notable elevated periods**: From early `2020` through `2023`, COMEX physical-delivery volumes ran materially above historical averages during multiple months. The cited reasons in market commentary included pandemic-era logistics disruptions, large-bar refining capacity constraints, and increased physical demand from central banks and institutional buyers. Without taking a position on causation, the observable data is that physical-delivery volumes in those periods exceeded what historical pattern would have predicted.

The implication for a retail bullion buyer is mostly nil. COMEX physical delivery volumes affect institutional bullion supply chains and futures-market basis; they don't directly affect what a retail buyer pays at APMEX or JM Bullion. For research purposes, watching the CME's monthly delivery reports is one of several signals about physical-market tightness.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

What is the COMEX gold contract size?

The standard CME Group COMEX gold futures contract (GC) represents 100 troy ounces of gold of minimum 99.5% fineness, deliverable in 100-oz bars or three 1-kilo bars from approved refiners. -

Do most COMEX contracts settle physically?

Historically a small percentage — most contracts are offset before expiry. However, physical-delivery volumes increased materially during certain 2020-2023 periods, drawing attention to inventory levels. -

Can a retail investor take delivery?

In principle yes, with the appropriate brokerage and clearinghouse arrangements, but the operational and storage requirements make it impractical for nearly all retail buyers. Physical bullion via a dealer is the retail path. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.