Delaware Depository vs Brink's Global Services

Side-by-side editorial comparison of Delaware Depository and Brink's depository services on IRS approval, allocated vs commingled options, insurance, and fees.

Methodology and disclosure

**Editorial disclosure.** BullionLens earns a commission when a reader opens a Gold IRA account through links on this page; the depositories on this page are not direct affiliate partners. The Gold IRA companies that route accounts to these depositories typically are affiliate partners. This does not change the fees the depository quotes; the Gold IRA company sets the storage fee passed to the customer, often with a markup over the depository's wholesale rate. Editorial selection is independent — see [our editorial standards](/editorial-standards/). Reviewed `2026-Q2`.

Delaware Depository and Brink's Global Services are two of the most-cited IRS-approved depositories for Gold IRA holdings. The two operators run different facility footprints, different insurance arrangements, and different operational models — Delaware Depository runs purpose-built precious-metals vaults; Brink's runs precious-metals storage as one product line within a broader global secure-logistics operation. The differences worth surfacing for a Gold IRA holder are facility location, insurance backstop, and the segregated-vs-commingled storage menu.

We compare seven objective criteria: corporate backgrounds, IRS-approved depository status, primary vault locations, segregated vs commingled storage options, insurance arrangements, fee structure (depository-side wholesale, not the markup the Gold IRA marketing company adds), and Better Business Bureau record. Figures are paraphrased from each operator's public materials current as of `2026-Q2`. We do not name a winner — the depository choice is often set by the Gold IRA marketing company at account opening rather than by the customer directly.

Corporate backgrounds

**Delaware Depository Service Company** was founded in `1999` and is headquartered in Wilmington, Delaware. The company operates a purpose-built precious-metals depository in Wilmington with a secondary facility in Texas via the related International Depository Services Group. Delaware Depository's primary business is precious-metals storage for IRA-holders, institutional customers, and direct-retail clients; the operation is single-purpose in a way that broader logistics companies are not.

**Brink's Global Services** is the precious-metals-storage product line of Brink's Incorporated, a publicly traded global secure-logistics company (NYSE: BCO) founded in `1859`. Brink's runs precious-metals vaults in multiple US cities (most notably Los Angeles, New York, and Salt Lake City) and internationally (London, Zurich, Singapore, Hong Kong). The precious-metals operation is one of multiple product lines within Brink's broader business, which includes ATM servicing, cash logistics, and high-value freight.

The structural difference matters operationally. Delaware Depository is single-purpose; the entire operation is built around precious-metals custody. Brink's is multi-purpose; precious-metals storage is one of several product lines within a global logistics company with significantly more revenue, more public-company financial transparency (Brink's Inc. files quarterly reports with the SEC), and a longer total operating history. Neither approach is inherently better; they are different operational models.

IRS-approved status

Both Delaware Depository and Brink's Global Services are IRS-approved depositories for IRA-held precious metals under IRC § 408(m). The IRS approval is the floor requirement for any depository that wishes to hold IRA precious metals on behalf of an IRS-recognized custodian. Both operators have held this approval continuously since their respective entries into the precious-metals-storage business.

The IRS approval is not a quality signal beyond the floor — it confirms the depository can legally hold IRA metals; it does not endorse the depository's operational quality, security practices, or insurance arrangements. The actual quality assessment requires reviewing the storage agreement, the insurance certificate, and the audit history.

Both operators participate in periodic third-party audits of holdings. Delaware Depository's audits are conducted by independent CPA firms on a published schedule; Brink's audits are part of the parent company's public-company audit cycle and are integrated into Brink's Inc.'s quarterly financial reporting. The audit-trail strength is roughly equivalent.

Locations and vault facilities

**Delaware Depository** operates its primary facility in Wilmington, Delaware. The Wilmington vault is purpose-built for precious-metals storage with multiple security layers (perimeter security, vault construction, alarm systems, surveillance, and 24-hour staffing). The secondary facility operated by the affiliated International Depository Services Group is in Texas. Delaware's location is convenient for East Coast clients and is the most-cited depository for Gold IRA accounts marketed by Augusta, Birch, and most other major Gold IRA companies as the default storage choice.

**Brink's Global Services** operates precious-metals storage in multiple US cities — Los Angeles, New York, Salt Lake City — as well as international facilities in London, Zurich, Singapore, and Hong Kong. For Gold IRA holdings (which IRS rules require to be stored in IRS-approved US depositories), the relevant Brink's facilities are the US locations. The geographic distribution provides options for clients who prefer non-Eastern-Corridor storage.

Net read: Delaware Depository concentrates in Delaware (with Texas via the IDS affiliate). Brink's fans across multiple US cities. A client who specifically wants West Coast or Mountain West storage typically goes through Brink's Salt Lake City or Los Angeles facility. A client comfortable with East Coast storage finds Delaware Depository the more-commonly-routed choice.

Allocated, segregated, commingled options

Both depositories offer the three standard storage arrangements. **Allocated** storage means specific bars and coins, identified by serial number and weight, are registered in the customer's name in the depository's records. **Segregated** allocated storage means the customer's specific holdings are physically separated from other customers' holdings (often in dedicated drawers, shelves, or vault sections). **Commingled allocated** storage means the customer holds specific identified bars and coins, but the physical arrangement is mixed with other allocated customers' bars and coins of the same type (still registered to each customer individually).

**Delaware Depository** offers segregated and commingled allocated storage; the marketing materials present segregated as the premium option with a higher annual fee. The segregated arrangement is often called 'Private Storage' or 'Segregated Storage' in customer documents.

**Brink's Global Services** offers segregated and commingled allocated storage. Brink's commingled storage is sometimes called 'Pool Allocated' in customer documents but remains allocated in the legal sense — the customer's specific bars are identified, just physically intermixed with other allocated customers' bars.

Neither depository's commingled-allocated arrangement is 'unallocated' in the legal sense. Unallocated storage (pool claim against a fungible inventory) is a separate, cheaper, and legally weaker arrangement; neither Delaware Depository nor Brink's typically markets unallocated storage for Gold IRA holdings, because the unallocated structure can produce IRS issues with the 'allocated to the IRA owner' identification requirement.

Insurance arrangements

Both depositories carry institutional all-risk insurance covering theft, mysterious disappearance, and natural disaster. The specific insurance carriers, coverage limits, and exclusions differ.

**Delaware Depository** insurance is placed through Lloyd's of London on the standard schedule, with stated coverage limits per location and per-customer aggregate caps published in the storage agreement. Lloyd's is one of the most established insurance markets for high-value bullion-storage risk; the Delaware coverage structure has been in place for the depository's operating history.

**Brink's Global Services** insurance is part of the parent company's global insurance program. Brink's Inc.'s public-company financial reporting discloses the insurance arrangements in aggregate for the precious-metals storage product line. The coverage structure benefits from the scale of Brink's overall logistics insurance buying power.

Net read: both depositories carry insurance appropriate to the precious-metals storage business. A Gold IRA holder should read the specific insurance certificate language for the assigned facility before signing the storage agreement, because per-location aggregate caps can matter if a single facility holds a large concentration of total customer assets.

Fee structure

Depository fees are charged to the Gold IRA custodian at a wholesale rate; the Gold IRA marketing company typically passes through a retail rate to the customer, with a markup. The fees a customer sees on their annual statement are the marked-up retail rate, not the depository's wholesale rate.

**Delaware Depository** wholesale-rate fees as of `2026-Q2` are paraphrased in industry summaries at approximately `$75`-`$125/yr` for commingled allocated storage and `$100`-`$200/yr` for segregated, depending on holdings value and custodian negotiation. Customer-facing rates passed through the Gold IRA marketing companies typically run `$100`-`$150/yr` commingled and `$150`-`$250/yr` segregated.

**Brink's Global Services** wholesale-rate fees as of `2026-Q2` are paraphrased at approximately `$100`-`$175/yr` for commingled allocated and `$150`-`$300/yr` for segregated, depending on facility and holdings value. Customer-facing rates passed through the Gold IRA marketing companies typically run `$125`-`$200/yr` commingled and `$200`-`$350/yr` segregated.

Net read: Delaware Depository tends to be the lower-fee option of the two on commingled storage by approximately `$25`-`$50/yr`; Brink's is competitive on segregated storage at certain facilities but tends to run higher on average. Confirm the actual customer-facing fee with the Gold IRA marketing company directly before signing; the wholesale rates above are illustrative.

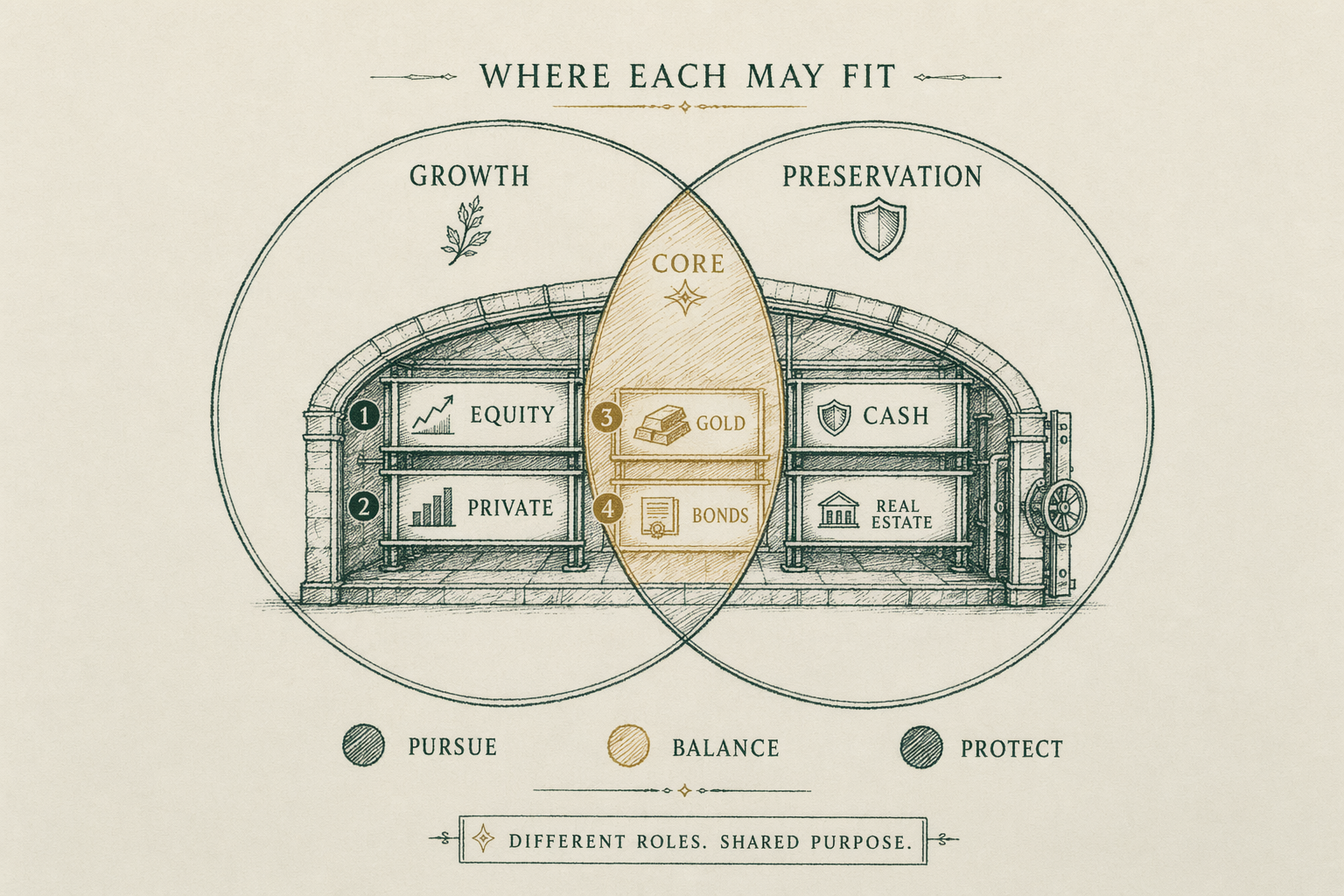

Where each may fit

The depository choice is most often set by the Gold IRA marketing company at account opening, not by the customer directly. A customer working with Augusta Precious Metals defaults to Delaware Depository because that is Augusta's default. A customer working with Goldco or American Hartford Gold can choose between Delaware Depository, Brink's Global Services, or International Depository Services of Texas at the new-account stage. The 'choice' between depositories is therefore typically a two-step decision: pick the Gold IRA marketing company first, then pick the depository from that company's available menu.

**Lean toward Delaware Depository if:** you are comfortable with East Coast storage, your Gold IRA marketing company's default is Delaware (Augusta, Birch, and most major companies use Delaware as default), or you value the single-purpose precious-metals operator model.

**Lean toward Brink's if:** you specifically want West Coast or Mountain West storage (Los Angeles, Salt Lake City), you value the public-company parent (Brink's Inc., NYSE: BCO) with quarterly SEC reporting transparency, or your Gold IRA marketing company has Brink's as a clearly offered alternative to Delaware.

Both are IRS-approved. Both offer allocated storage in segregated and commingled formats. Both carry institutional insurance. The decision is operationally about geography and about whether the marketing company offers a clear choice or defaults to one.

_Educational content, not personalized investment advice. BullionLens is not a registered investment adviser. Consult a licensed adviser before making decisions about retirement assets._

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Which depository is better?

Both are major IRS-approved depositories with strong industry reputations. The choice is usually set by your Gold IRA custodian and your geographic preference, not by you directly. -

Are insurance arrangements the same?

Both carry institutional all-risk insurance. Specific limits and exclusions differ; read the storage agreement carefully before signing. -

Is the comparison data current?

We snapshot fees and arrangements quarterly minimum and stamp each comparison with a 'Last reviewed' date. Companies change fees, custodians, and storage partners — verify with the company directly before opening an account. -

What if my situation doesn't match either company's profile?

The comparison is a starting point, not personalized advice. If neither company fits, see /reviews/gold-ira-companies/ for the full list of companies we cover and /editorial-standards/ for our selection criteria.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.