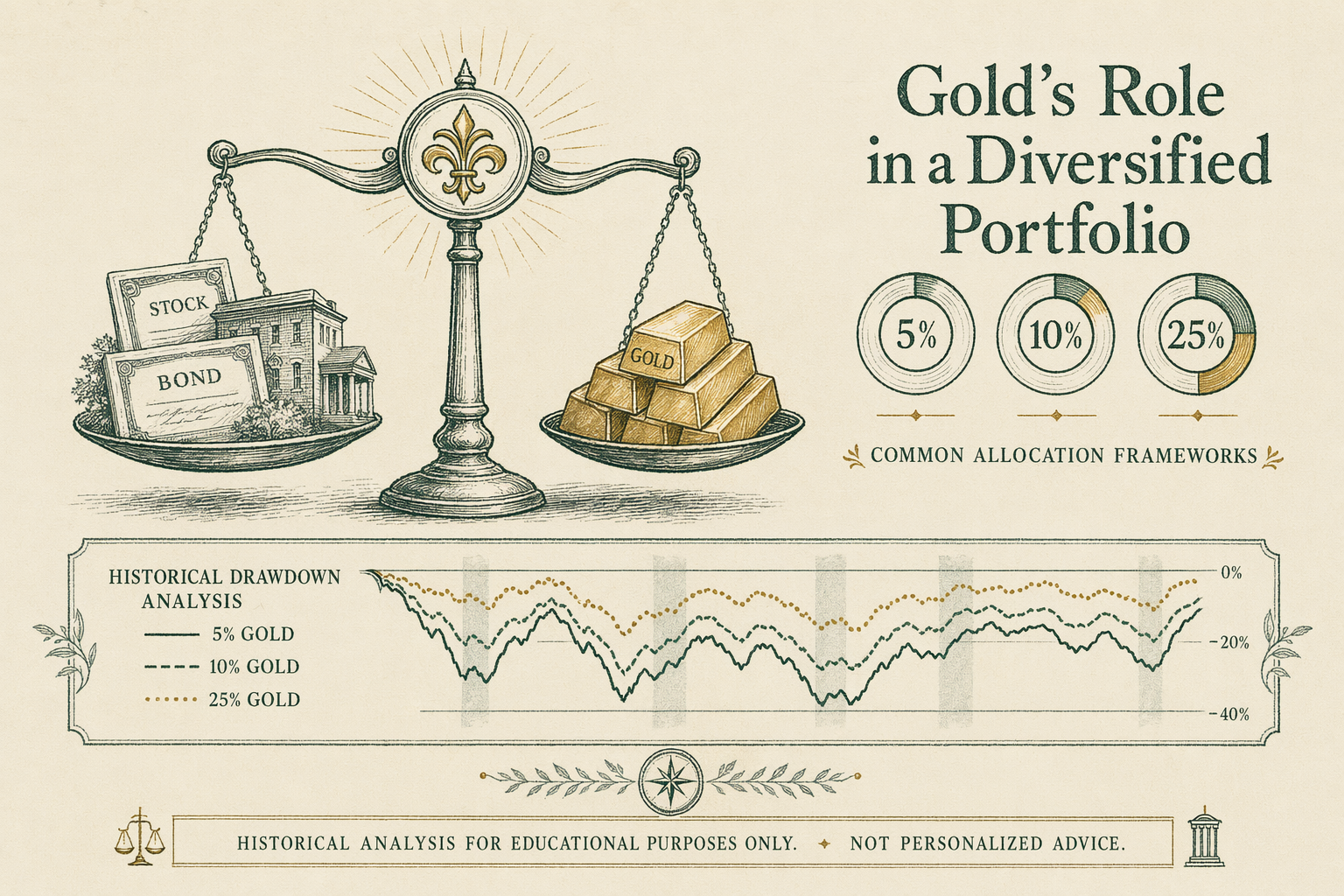

How much gold should a portfolio hold?

Common allocation frameworks for gold in a diversified portfolio: 5%, 10%, 25%. Historical drawdown analysis, not personalized advice.

What we are NOT doing — personalized advice

There is no academic or regulatory consensus on a single 'right' gold allocation. Practitioner frameworks span a range from `0%` (the standard pre-2000 US pension-fund posture) to `25%` (Harry Browne's Permanent Portfolio) to higher allocations published by individual newsletter authors. None of those frameworks is universally endorsed by a fiduciary body. The Department of Labor does not specify a gold allocation. The SEC does not specify one. The CFP Board does not specify one. Each framework is built on a different set of assumptions about correlations, drawdowns, and what you are trying to protect against.

BullionLens is an editorial research desk, not a registered investment adviser. This article surveys the most commonly cited frameworks and the historical drawdown data behind them. It does not tell you what your gold allocation should be. That answer depends on your age, your retirement horizon, your existing portfolio composition, your tax situation, your liquidity needs, and your tolerance for the year-to-year drawdown gold can produce. Those variables require a conversation with a licensed adviser who knows your full financial picture. The frameworks below are educational anchor points — useful for asking the right questions, not for substituting your judgment with ours.

The 5% conventional allocation

The most commonly cited gold allocation in mainstream financial-planning literature is `5%`. The World Gold Council's institutional research repeatedly returns to a `2%-10%` band, with `5%` as the rough midpoint. Mercer's 2019 report on the role of gold in institutional portfolios cited diversification benefit peaking around the `5%-10%` range in modeled US balanced portfolios. Adding meaningfully more than that began to shift the portfolio's risk profile from 'diversified with a gold sleeve' to 'directional bet on gold,' which is a different posture.

The `5%` framing has a practical appeal. At that size, the gold sleeve can absorb a `-30%` drawdown without imperiling the rest of the portfolio: a `-30%` move on `5%` is a `-1.5%` total-portfolio drag. The investor gets some of the low-correlation diversification benefit without making gold's own volatility the dominant feature. The `5%` allocation also fits cleanly into a standard `60/40` stocks/bonds structure as a small carve-out from either side — usually pulled from the bond sleeve, since gold is most often framed as an alternative to long-duration bonds in inflation scenarios.

The 10% diversifier allocation

A `10%` allocation appears across multiple practitioner frameworks: Ray Dalio's All Weather strategy (`7.5%` gold + `7.5%` commodities in the published version, often rounded to a `15%` real-asset sleeve with gold the larger piece), several published target-date-fund inflation-protection sleeves, and a number of independent fee-only advisers in the US Southeast and Mountain West who specialize in conservative retirement portfolios. At `10%`, the gold sleeve carries enough weight to materially move portfolio returns in either direction during gold-favorable or gold-unfavorable regimes.

The empirical evidence on diversification benefit past `10%` is mixed. The World Gold Council's 2020 paper on gold in pension portfolios modeled marginal Sharpe-ratio improvement that flattened near `10%` and turned negative beyond `15%` in their US-balanced base case. The flattening reflects a structural point: gold's diversification benefit comes from low correlation with equities and high-grade bonds, but its standalone return-and-volatility profile is mediocre — comparable annualized return to equities since `1971`, with deeper drawdowns. Past `10%`, you are buying gold's volatility without proportionally more correlation benefit.

Permanent Portfolio 25% allocation

Harry Browne's Permanent Portfolio — published in his 1981 book *Inflation-Proofing Your Investments* and elaborated through the 1980s and 1990s — splits assets `25%` equities, `25%` long-term Treasury bonds, `25%` cash, `25%` gold. Browne's argument was that each `25%` sleeve dominates in one of four economic regimes (prosperity, deflation, recession, inflation), so the portfolio is structurally insulated against any one regime breaking the whole. The `25%` gold allocation is the headline feature; the cash and bond sleeves are equally load-bearing.

The Permanent Portfolio's historical performance is well-documented and worth reading in primary form before subscribing to the framework. From `1972` through the present, the strategy's annualized real return has run roughly `3%-5%` lower than a `60/40` stocks/bonds benchmark, with materially lower drawdowns in 1973-74, 2000-02, and 2008-09. The tradeoff is structural: you give up bull-market upside in exchange for narrower drawdowns. Whether that tradeoff fits your situation depends on your liability profile. Browne's framework was written for retirees and pre-retirees who valued capital preservation over return maximization. It is not a one-size-fits-all recommendation.

Historical drawdown comparison

Drawdown is the right framing for an allocation conversation, because the question is rarely 'how much extra return does gold add over 30 years.' The more common question is 'how much does the portfolio fall in the worst year, and can I tolerate that?' Gold's own worst-year drawdowns since `1971` are substantial — `-32.6%` in `1981`, `-21.4%` in `2013`, `-25.9%` in `2008` peak-to-trough during the Lehman liquidity squeeze before recovering. Adding gold to a portfolio does not eliminate drawdown; it changes which scenarios produce the worst result.

Modeled against the `60/40` benchmark from `1972` to `2024`, a `5%` gold carve-out reduced the portfolio's worst calendar year by roughly `1-2` percentage points and added marginal smoothing in inflation-shock years (`1974`, `1979`, `2022`). A `10%` allocation produced larger smoothing during inflation shocks but slightly increased the portfolio's worst-year drawdown during deflationary or strong-dollar episodes (`1981-82`, `1996-99`, `2013-15`). A `25%` allocation in the Permanent Portfolio configuration produced the narrowest range of calendar-year outcomes overall, at the cost of materially lower long-run real returns. None of these scenarios is 'risk-free.' Each represents a different bet on which future regimes you are protecting against.

Real-world example — the 2008-2011 sequence at three sleeve sizes

Consider three identical `60/40` portfolios at the end of `2007`, each with `$1,000,000` in invested assets. Portfolio A holds `0%` gold. Portfolio B carves out `5%` for gold (`$50,000`, funded by reducing the bond sleeve to `35%`). Portfolio C carves out `10%` (`$100,000`, bonds at `30%`). LBMA spot gold closed `2007` at roughly `$833/oz` and ended `2011` at roughly `$1,531/oz` — a `+83.8%` four-year nominal move. The S&P `500` returned `-0.0%` price-only over the same window (recovering from a `-37%` `2008` drawdown). Aggregate bonds returned roughly `+25%` total.

Portfolio A's `2007-2011` trajectory: down `-22%` in 2008, recovers to roughly `$1,015,000` by year-end `2011`. Portfolio B: down `-19%` in 2008 (smaller equity drag, plus a small gold lift), ends `2011` near `$1,065,000`. Portfolio C: down `-17%` in 2008 (despite gold's mid-2008 sell-off, the bond and gold sleeves cushioned the equity loss more), ends `2011` near `$1,098,000`. The differences are real but modest at the conservative allocations. A reader who only saw the headline 'gold went from `$833` to `$1,531`' might expect Portfolio C to materially outpace Portfolio A; in practice, the sleeve was 10% of the portfolio, so its move contributed roughly `$84,000` of the `$83,000` gap. Gold's contribution scaled with sleeve size; it did not transform the portfolio's trajectory.

Common misconceptions readers bring to allocation

**'5% is the right answer for everyone.'** No. `5%` is the most commonly cited mainstream-research midpoint. Your appropriate allocation depends on your liability structure, your existing diversification, and your tolerance for gold's own drawdowns. A retiree with a `30%` bond ladder, an annuity, and Social Security has different room for a gold sleeve than a `35`-year-old with a `100%` equity `401(k)` and significant human capital.

**'Higher allocations always lower drawdown.'** No. Above `10%-15%`, you increasingly take on gold's standalone volatility without proportional diversification benefit. The Permanent Portfolio's `25%` works only because the other three sleeves are equally rigid; transplanting `25%` gold into an otherwise standard `60/40` does not produce a Permanent Portfolio result.

**'Gold is uncorrelated with stocks.'** Imperfectly true. Gold's long-run correlation to US equities runs roughly `0.0` to `+0.1`, but short-window correlations vary widely. In Q4 `2008` and again in Q1 `2020`, gold sold off alongside equities for several weeks during liquidity stress. Correlation regimes shift; the headline 'low correlation' is a long-window average.

What this means for you

Start with what you are trying to protect against. Inflation surprise? Currency debasement? Equity-market drawdown? Liquidity crisis? Each scenario has a different ideal hedge, and gold is the best fit for some and a mediocre fit for others. Then bring your full portfolio context — existing real-asset exposure (REITs, commodities, TIPS), human capital trajectory, retirement horizon — to a fee-only fiduciary adviser who can size a sleeve within the broader allocation. The `5%`, `10%`, and `25%` frameworks above are useful conversational anchors. They are not substitutes for a personalized plan, and BullionLens does not provide one.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Is there a 'right' gold allocation?

No. There is no academic or regulatory consensus on a 'right' gold allocation. Common practitioner frameworks cite 5-15% for diversification; Harry Browne's Permanent Portfolio used 25%. Personal allocation requires personalized advice from a licensed adviser. -

Do diversification benefits change with allocation size?

Yes. Empirical research generally finds incremental diversification benefit declines past 10-15% allocation. Above that, you are increasingly making a directional gold bet rather than a portfolio diversifier. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority. -

When was this page last reviewed?

See the 'Last reviewed' date at the bottom of the page. We commit to a quarterly minimum review cycle; fee schedules, IRS rules, and company arrangements can change between reviews — confirm with primary sources before transacting.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.