Central bank gold flows

Central-bank gold purchases hit multi-decade highs in 2022-2023. The buyers, the stated reasons, and the structural drivers — descriptive analysis only.

What 'central bank gold' actually means

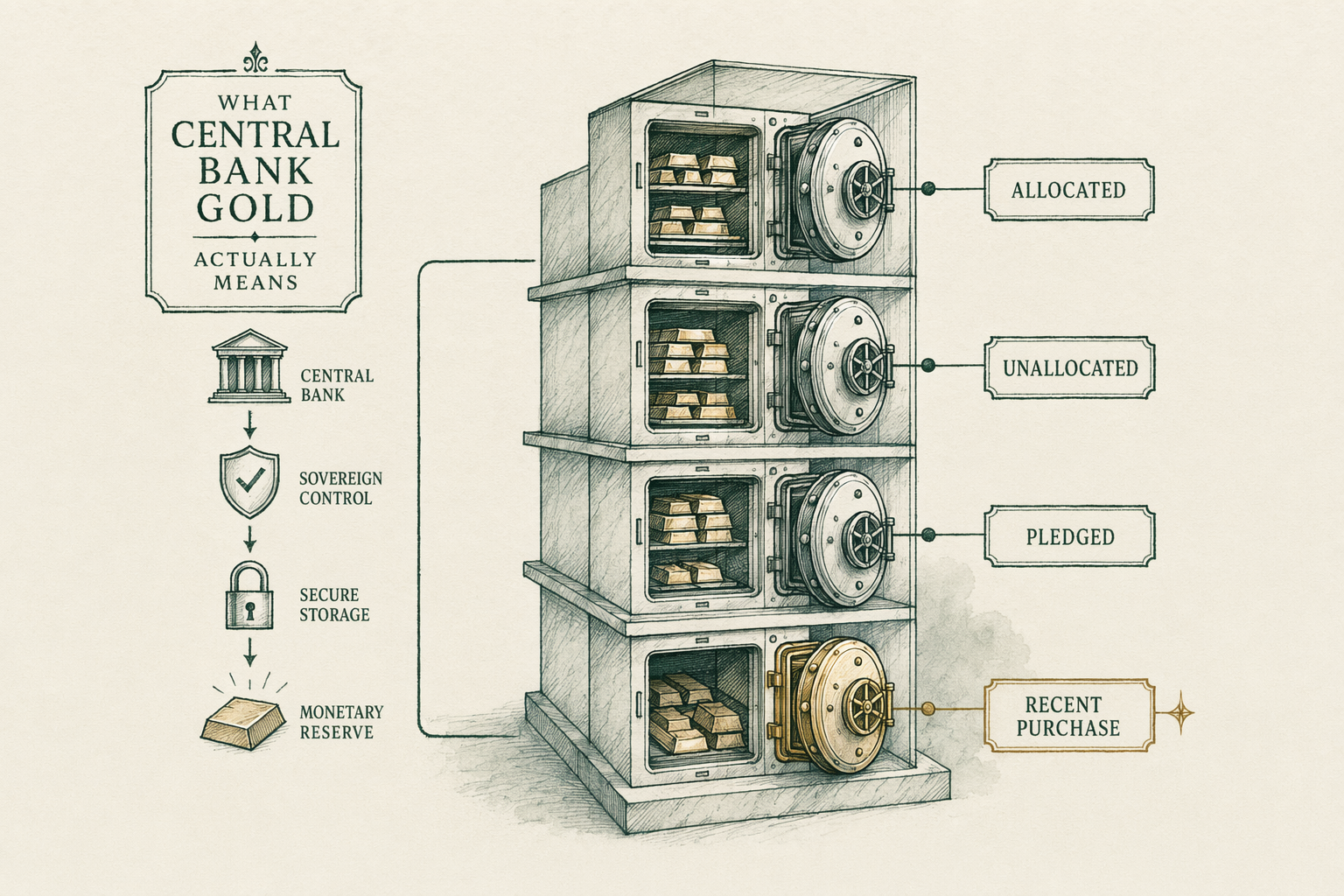

Central-bank gold is gold held by national central banks (or by sovereign-wealth funds and other government-controlled monetary institutions) on the institution's own balance sheet, as part of the institution's foreign-exchange and monetary-reserve holdings. As of recent IMF-published estimates the global total of central-bank-held gold is roughly `35,000` to `36,000` tonnes — equivalent to roughly `20%` of the total above-ground gold stock in the world.

The largest central-bank gold holders by tonnage are the United States Treasury (`8,133` tonnes, held by the Federal Reserve Bank of New York and the US Bullion Depository at Fort Knox), Germany (`3,355` tonnes), Italy (`2,452` tonnes), France (`2,437` tonnes), and the Russian Federation (`2,332` tonnes before 2022; post-2022 the position is harder to verify externally). These five hold approximately half of all central-bank gold globally.

Beyond the top five, the next tier of major holders includes China (officially `2,235` tonnes as of late 2024, with unofficial estimates from researchers including ones by SocGen and HSBC suggesting the actual holding may be materially larger), Switzerland, Japan, India, the Netherlands, and Turkey. These constitute roughly another quarter of global central-bank gold.

The IMF and the World Gold Council publish quarterly central-bank holdings data drawn from member countries' published reserve statistics. The data is the canonical institutional reference and is what professional gold-market analysts cite. Retail-press summaries of 'central bank buying' typically draw from World Gold Council quarterly demand-trends reports, which are themselves drawn from IMF International Financial Statistics and supplementary surveys.

The World Gold Council annual survey

The World Gold Council publishes an annual Central Bank Gold Reserves Survey, polling reserve managers at central banks globally about their gold-management views, intentions, and rationale. The survey has been published annually since 2018 and is the canonical institutional reference for understanding central-bank reserve-manager thinking on gold.

Survey methodology: WGC sends a structured questionnaire to reserve managers at central banks worldwide, with response rates in the `40%` to `60%` range depending on the year and the specific question. Responses are anonymized at the country level when reported. The questionnaire covers topics including current holdings, expected changes, the rationale behind holding gold, and views on gold's role in the broader reserve portfolio.

The 2024 survey found that approximately `81%` of responding central banks expected global central-bank gold holdings to increase over the next `12` months, the highest reading in the survey's history. Approximately `29%` of respondents indicated their own institution planned to increase its gold holdings over the next `12` months — also the highest reading in the survey's history.

The top-stated reasons for holding gold in the 2024 survey: 'performance during times of crisis' (cited by `76%` of respondents), 'long-term store of value' (`73%`), 'effective portfolio diversifier' (`72%`), 'no default risk' (`64%`), 'no counterparty risk' (`62%`), and (notably elevated post-2022) 'concerns about geopolitical risk' and 'concerns about sanctions resilience' as cross-cutting themes. The geopolitical and sanctions-resilience themes were not separately tracked in pre-2018 surveys but have risen sharply in survey-tracked responses since 2022.

Key caveat: the survey reflects stated rationale from responding institutions. Actual purchase behavior may diverge from stated rationale. The published survey data and the actual flow data (IMF holdings statistics) together provide the institutional picture; neither alone is sufficient.

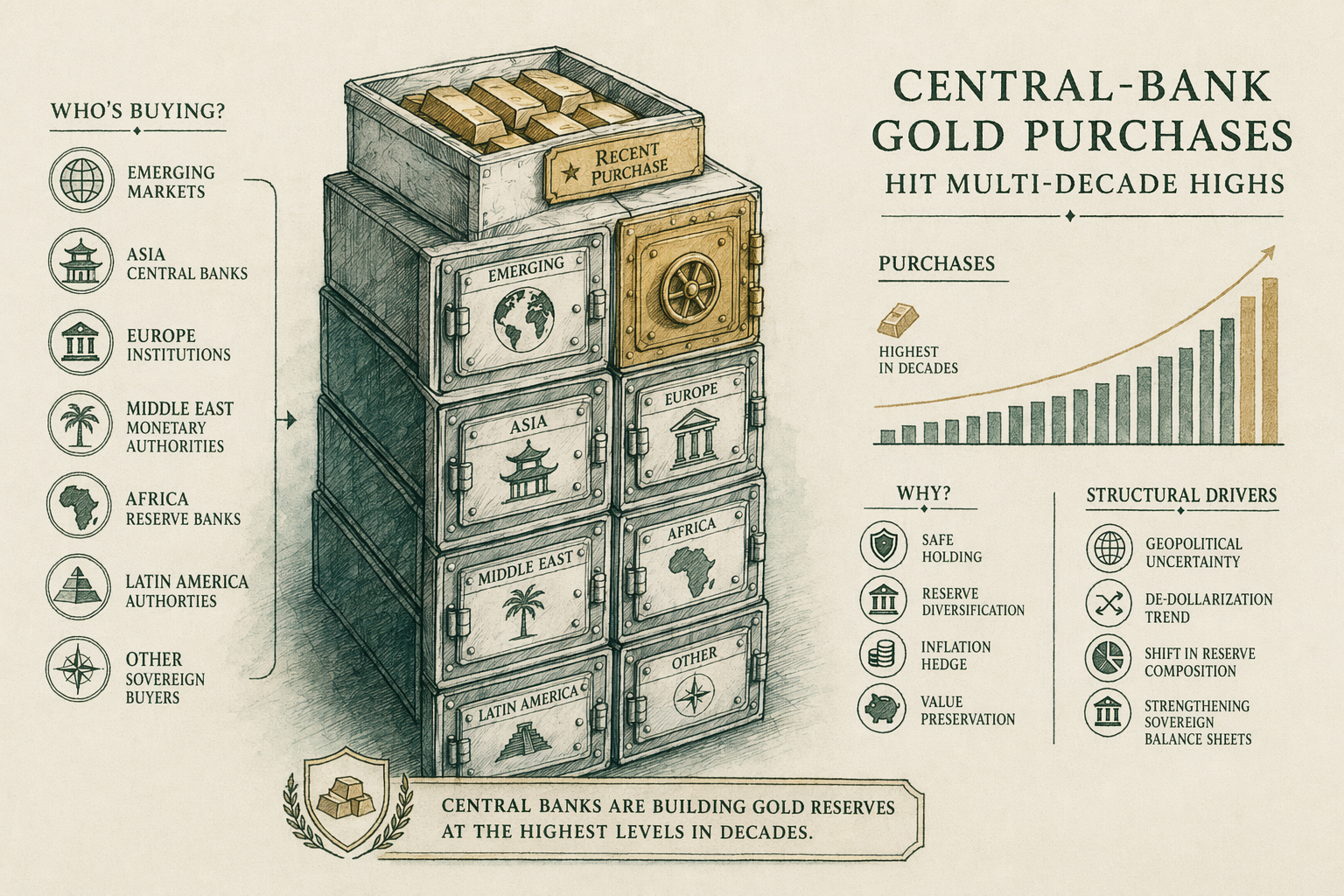

Major net buyers — China, Poland, Singapore, Turkey

The largest reported central-bank net gold buyers in the 2022-2024 window, per IMF and WGC published data, were the People's Bank of China, the National Bank of Poland, the Reserve Bank of India, the Central Bank of Turkey, and the Monetary Authority of Singapore.

The People's Bank of China resumed reporting gold purchases in late 2022 after a multi-year pause in reported buying, adding approximately `316` tonnes through end-2024 by official reporting. Unofficial estimates from market researchers (including widely-cited analysis from Société Générale and from HSBC Bank's commodity research desk) suggest China's actual gold accumulation across this window may be materially larger than the official reporting reflects.

The National Bank of Poland added approximately `130` tonnes through 2023 and continued additions in 2024. NBP's stated rationale (per its public statements from Governor Adam Glapinski and from NBP communication materials) cites diversification away from US dollar reserves, gold's behavior during crises, and geopolitical risk hedging following the 2022 Russia-Ukraine conflict and the resulting sanctions framework.

The Central Bank of Turkey accumulated gold materially in 2023 (over `100` tonnes net add). Turkey's broader monetary context — high domestic inflation, currency-management challenges, and significant retail-citizen gold holdings — sits behind the official-reserve buying. Turkey's net-buying pace fluctuated significantly across 2022-2024 with the country's overall reserve-management dynamics.

The Reserve Bank of India added approximately `73` tonnes through 2024, continuing a multi-year pattern of measured gold accumulation. India's stated rationale focuses on portfolio diversification and gold's long-term store-of-value role.

The Monetary Authority of Singapore added approximately `26` tonnes through early 2023. MAS's gold-management approach has historically been more conservative; the 2023 add represented an inflection point.

Beyond the named top buyers: Czech National Bank, the Reserve Bank of Australia (limited, but notable directional shift), the Hungarian National Bank, the Iraqi central bank, and a number of others have shown smaller-but-directionally-consistent net buying in the 2022-2024 window. The aggregate-emerging-market pattern is more important than any individual country's behavior — the emerging-market central-bank cohort is collectively the dominant source of net global central-bank gold buying.

Stated rationale: diversification, geopolitical risk, sanctions resilience

The 2022 freezing of Russian central bank foreign-currency reserves by Western governments (a coordinated G7-plus-EU action following the start of the Russia-Ukraine conflict) was a material event in the institutional context of central-bank gold thinking. The freezing affected approximately `$300` billion of Russian central-bank reserves held in Western financial institutions and central banks. The reserves remained frozen as of 2026-Q2; resolution of the assets has been a subject of ongoing diplomatic and legal discussion.

Post-2022, the World Gold Council's reserve-manager survey began capturing the 'sanctions resilience' theme more explicitly. The 2023 and 2024 surveys both showed materially elevated stated importance for the concept that gold is held outside any national jurisdiction's ability to freeze or seize (subject to where the gold is physically held — gold stored in the Bank of England's vaults in London is held under UK jurisdiction, while gold held by a central bank in its own country is held in its own jurisdiction).

The diversification rationale predates 2022 and has been the most consistently stated reason for central-bank gold holdings across the entire survey history. Gold's near-zero correlation to typical reserve currencies (US dollar, euro, yen, sterling), its non-default-risk profile (gold is no one's liability), and its low correlation to other reserve assets in stressed periods are the foundational diversification arguments.

The geopolitical-risk rationale captures the broader theme that gold provides a reserve asset that does not depend on the integrity of any specific issuer or any specific institutional framework. This theme rose materially in survey responses across 2022-2024.

Causal direction caveat: the rationales surveyed are stated reasons. Whether central banks actually bought because of the stated reasons, or whether they bought for other reasons and rationalized the buying with the survey-friendly language, is not resolvable from the survey data alone. Both can be partly true.

Practical implication for gold-market analysts: central-bank flows are now a structural variable rather than a residual. Annual net buying in the `1,000` tonne range represents roughly `25%` to `30%` of total annual mine supply, which is enough to meaningfully tilt market balance. The /case-studies/2024-spot-price-decoupling/ case study covers the 2024 price-action implications.

Repatriation flows

A separate strand of post-2010 central-bank gold activity is repatriation — the movement of gold that had historically been held in foreign vault locations (London at the Bank of England, New York at the Federal Reserve Bank of New York) back to vault locations within the holding country's own jurisdiction.

Germany's Bundesbank announced in 2013 a multi-year program to repatriate approximately `674` tonnes of its gold from New York and Paris back to Frankfurt, completing the program in 2017. The Netherlands' De Nederlandsche Bank repatriated approximately `123` tonnes from New York back to Amsterdam in late 2014. France, Belgium, Austria, and a number of other countries have undertaken smaller similar programs. Poland announced a 2018-2019 repatriation program moving approximately `100` tonnes from London to Warsaw.

The publicly stated rationales for repatriation programs cluster around three themes: domestic-jurisdiction control over reserves; the symbolism of holding the country's gold within its own borders; and (in some country-specific cases) responses to political-domestic-audience concerns about whether foreign-held gold is actually in the vaults as documented.

Repatriation is a flow of metal between vault locations, not a change in total holdings. It does not change the global central-bank gold total. It does change the geographic distribution of vault holdings — and meaningfully changes the LBMA London-vault inventory data, which is a tracked institutional metric.

Operational note: physical repatriation of significant gold tonnage is a multi-year process. The bars must be inspected, re-weighed, sometimes re-refined to the receiving country's preferred bar specification, transported under insurance, and re-vaulted at the receiving end. The Bundesbank's `674`-tonne program took five years to execute.

Historical context — 1999 Washington Agreement to today

Central-bank gold behavior has shifted regime twice in the past three decades. The first shift was the late-1990s recognition that coordinated European central-bank gold sales were depressing prices in a way that was harming the affected institutions. The 1999 Washington Agreement (formally the Central Bank Gold Agreement) — initially signed by `15` European central banks — capped collective annual gold sales at `400` tonnes through 2004. The agreement was renewed in 2004 (`500` tonne cap), 2009 (`400` tonne cap), and 2014. Coordinated European central-bank net selling effectively ended in the late 2010s as policy shifted toward net stable holdings or marginal buying.

The second shift was the 2018-onward emergence of net buying as the dominant central-bank pattern. By the early 2020s the European-coordinated-selling framework had become essentially irrelevant — there was no coordinated selling to coordinate. The Washington Agreement framework was not renewed after its 2014 iteration expired.

The 2022-2024 multi-decade-high buying pattern represents the maturation of the second-shift regime, with emerging-market central banks now structurally the dominant flow. Western developed-market central banks have remained broadly net stable; emerging-market central banks have driven the aggregate flow.

Whether the current high-buying regime continues, plateaus, or reverses is genuinely uncertain. Survey data from 2024 indicates strong continued intent to buy among the surveyed institutions; institutional inertia in reserve-management decisions suggests the pattern has multi-year persistence in either direction once set. We avoid forward-looking predictions per our editorial framework — see /editorial-standards/.

What is descriptively clear: the structural role of central-bank gold flows in the gold-market balance is materially different in 2026 than it was in 2018, and any analysis of gold-market structure that does not include the central-bank flow variable is incomplete.

How we sourced this

Citations draw from the International Monetary Fund's International Financial Statistics (the canonical data source for central-bank reserve holdings); the World Gold Council's annual Central Bank Gold Reserves Survey (2018 through 2024 editions); the World Gold Council's quarterly Gold Demand Trends reports; the Bank for International Settlements' gold-market data; individual central-bank annual reports and reserve-management communications (especially from the National Bank of Poland's Governor Glapinski and from the People's Bank of China's published reserve statistics); and the published academic literature on gold's role in central-bank reserve portfolios.

Repatriation-program documentation draws from the Bundesbank's published 2013-2017 repatriation-program reports, the De Nederlandsche Bank's 2014 repatriation communication, and contemporaneous coverage in Reuters, the Financial Times, and Bloomberg.

We deliberately rely on institutional and primary-source data rather than retail-press summaries. Where the data is contested (notably China's official-vs-actual holdings), we cite both the official reporting and the major commercial-research alternative estimates with the caveat that the actual figure is not externally verifiable.

In plain English

In plain English: central banks worldwide collectively hold about a fifth of all the gold ever mined. The US Treasury holds the most. Western developed-market central banks have been broadly net stable for two decades. Emerging-market central banks (China, Poland, Turkey, India, Singapore) have been net buying aggressively since 2018, with the pace hitting multi-decade highs in 2022-2024 after Western governments froze Russian central-bank reserves. The stated reasons are diversification, geopolitical risk, and sanctions resilience. The flows are now large enough to materially influence gold-market balance over multi-year windows. We do not predict where this goes next — the survey data suggests continued buying intent, but reserve-management decisions have a way of changing without notice.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

Who buys the most gold among central banks?

Per World Gold Council data, the People's Bank of China, the National Bank of Poland, the Reserve Bank of India, the Central Bank of Turkey, and the Monetary Authority of Singapore have been among the largest reported net buyers in recent years. Unreported buying may differ. -

Why do central banks publicly hold gold?

Per the World Gold Council's annual reserve survey, the top stated reasons include 'performance during times of crisis,' 'long-term store of value,' 'effective portfolio diversifier,' and 'no default risk.' Geopolitical risk and sanctions resilience have risen in recent surveys. -

What was the 1999 Washington Agreement?

An accord among European central banks limiting collective gold sales after a decade of large net selling depressed prices. Renewed in 2004, 2009, 2014. Coordinated selling effectively ended in the late 2010s as central-bank policy shifted toward net buying. -

Are central-bank flows a price signal?

Descriptively, central-bank net buying has correlated with elevated gold prices in 2022-2024. Causal direction is contested. Treat the data as structural context, not a trade signal.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.