Why does China buy gold?

The People's Bank of China gold-reserve buying: stated reasons, the dollar-diversification thesis, and what the data shows.

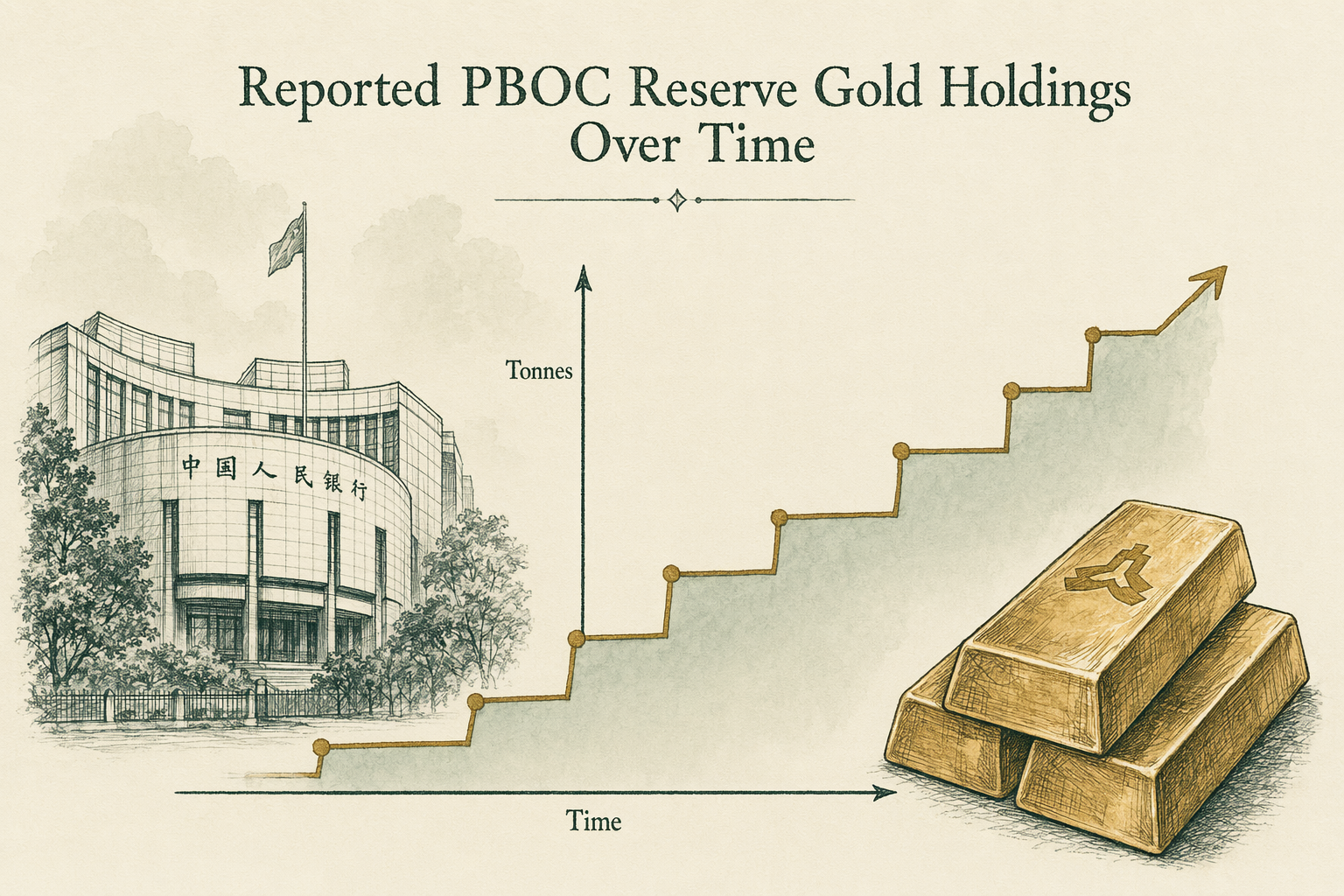

Reported PBOC reserve gold holdings over time

The PBOC reports its gold reserves periodically to the International Monetary Fund and via the SAFE (State Administration of Foreign Exchange) monthly disclosures. The reported figures have moved substantially over the past two decades.

Approximate reported holdings at key points (rounded to the nearest `100 tonnes`): `2002` at approximately `400 tonnes`; `2009` after a reported `454 tonne` purchase brought holdings to approximately `1,054 tonnes`; `2015` after a series of reported monthly increases reached approximately `1,700 tonnes`; `2020` at approximately `1,948 tonnes`; reported holdings continued increasing through `2022-2025` to a level reported above `2,200 tonnes` by mid-decade.

These are reported figures. The PBOC's reporting cadence is irregular — multi-year periods of unchanged reported holdings have been followed by sudden large announced increases (the `2009` and `2015` patterns), which most analysts interpret as the PBOC accumulating off-balance-sheet through state-owned commercial banks and then transferring to the central bank's reserve account when convenient to disclose. Snapshot as of `2026-Q2`.

Stated rationale

PBOC and Chinese government communications cite several stated reasons for gold accumulation: diversification of foreign-exchange reserves (which historically have been heavily weighted toward US Treasury securities); hedging against currency volatility in major reserve currencies; building a strategic asset that does not have direct counterparty exposure to a foreign government; and supporting the long-term goal of a more diversified global reserve currency system.

The World Gold Council's annual central-bank survey, which interviews reserve managers from approximately `60-70` central banks each year, has consistently shown gold's perceived strengths cited as: hedge against systemic risk, no default risk, performance during crisis, and historical store of value. Chinese reserve management is consistent with the broader emerging-market central-bank trend toward gold accumulation that the WGC survey has documented.

Read these stated rationales as official communications — they reveal what the PBOC chooses to disclose about its thinking. They are not the same as a comprehensive view of internal decision-making, which is not publicly accessible.

The dollar-diversification thesis

The most-cited interpretation in market commentary connects China's gold accumulation to the long-term goal of reducing dependence on US-dollar-denominated reserves. The thesis: as the United States and allied nations have increasingly used financial-system access as a geopolitical lever (sanctions, asset freezes, SWIFT exclusions), holding reserves in dollar-denominated assets carries political risk that gold (a bearer asset held domestically) does not.

The empirical support: China's US Treasury holdings peaked around `2013-2014` at approximately `$1.3 trillion` and have declined over the subsequent decade to approximately `$770 billion` by late `2024`. Over roughly the same period, China's reported gold holdings increased materially. The correlation is suggestive but not causal — the Treasury decline reflects multiple factors including currency-management operations and balance-of-payments shifts, not solely a reserve-diversification preference.

The thesis has substantial academic and policy-research backing — particularly in the post-2022 environment after the Russian central-bank reserve freeze made the political-risk dimension of reserve currency choice concrete. The thesis is contested, with some analysts arguing that the gold accumulation reflects a much narrower set of considerations and that the dollar-diversification framing is overstated.

Domestic gold market context

Beyond the PBOC's reserve accumulation, China is the world's largest consumer of physical gold by volume — driven by jewelry demand, bar-and-coin investment, and (recently) industrial use in semiconductor and electronics manufacturing. The Shanghai Gold Exchange (SGE) is the world's largest physical gold spot market by volume.

Chinese domestic gold demand is influenced by cultural factors (gold's traditional role in weddings, Lunar New Year gifting, and savings), tax policy (favorable treatment of physical gold versus other investment classes), and the limited menu of high-yielding investment alternatives available to Chinese retail investors.

The domestic-demand picture matters for the PBOC's accumulation strategy. A central bank that needs to source physical gold can draw on Chinese-mined production (China is the world's largest gold producer, currently around `370 tonnes/yr` from domestic mines) without needing to compete with international buyers in London or New York markets. This domestic-sourcing advantage gives the PBOC operational flexibility that smaller central banks do not have.

Caveats on reported vs actual holdings

PBOC-reported gold reserves are the PBOC's own disclosures to the IMF and to the public. They are not independently audited or verified by a third party. The pattern of irregular reporting — multi-year stretches of unchanged holdings followed by sudden announced increases — has led many analysts to estimate actual holdings above the reported figure, with the gap potentially material.

Independent estimates of actual PBOC holdings have ranged widely. The estimates rest on indirect evidence: China's role as the world's largest gold producer with extremely limited export, the volume of Chinese gold imports through Hong Kong and Shanghai customs records, and the SGE's net deliveries to the PBOC's commercial-bank counterparties. None of these are direct measures.

The honest summary: reported PBOC gold holdings have risen materially over the past two decades to a level among the world's largest sovereign holdings; actual holdings are widely believed to be higher than reported; precise figures on the unreported portion are not available. Treat the reported figures as a floor, not as the complete picture.

Want to talk this through? Book a 30-min research call →

Frequently asked questions

-

How much gold does China hold?

Per published PBOC reserve data, China's official gold reserves have risen materially over the past two decades to a level among the world's largest sovereign holdings. Reported figures are PBOC's own disclosures — unreported holdings are widely discussed but not verified. -

Is this dollar diversification?

Stated central-bank rationale per the World Gold Council survey includes reserve diversification and geopolitical risk hedging. Causation versus correlation with US Treasury holdings is contested in the academic literature. -

Where does BullionLens get its data on this topic?

Primary sources cited in the article. For market data we lean on the LBMA daily fixings, COMEX volume reports, IRS publications, SEC filings, and the World Gold Council's annual reports. We do not cite secondary aggregators as authority. -

When was this page last reviewed?

See the 'Last reviewed' date at the bottom of the page. We commit to a quarterly minimum review cycle; fee schedules, IRS rules, and company arrangements can change between reviews — confirm with primary sources before transacting.

In plain English We're an editorial desk. Educational only — talk to a licensed adviser before doing anything with retirement assets.